Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan the FTSE 100 break free?

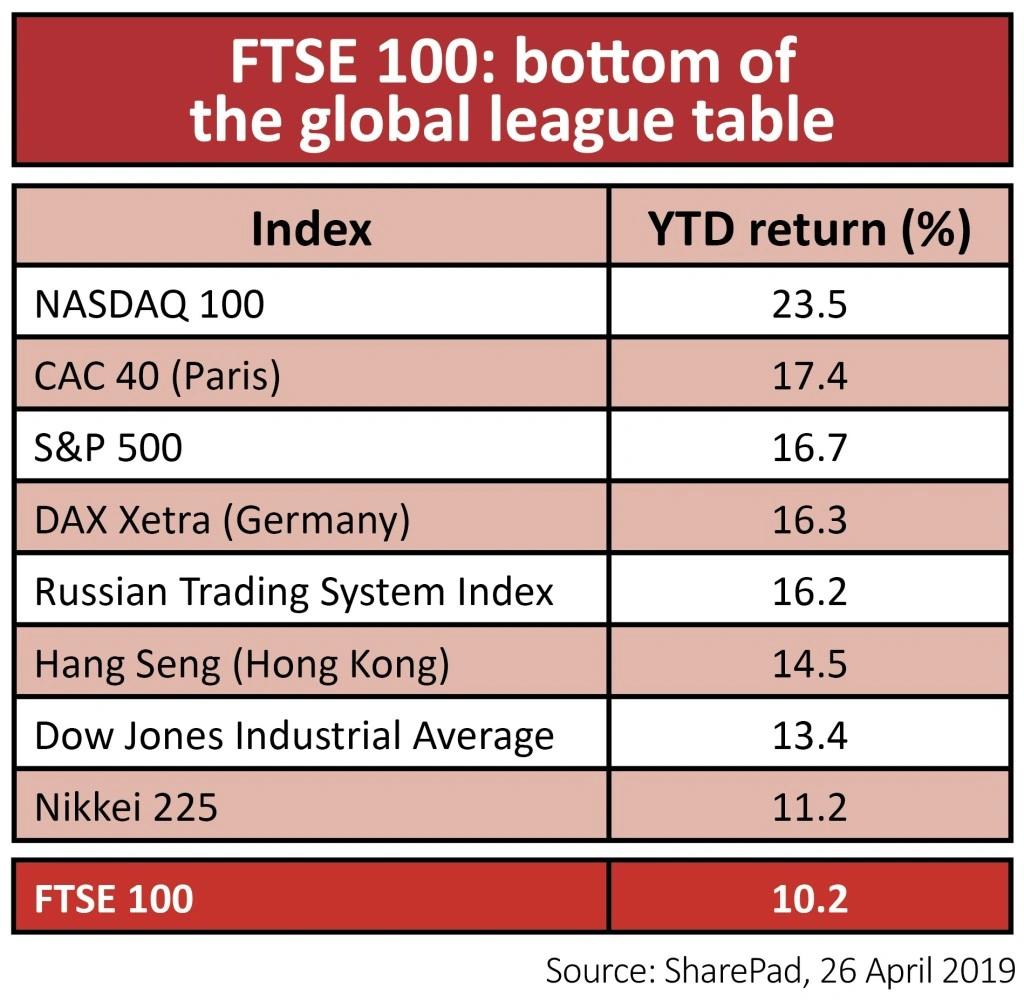

The 10.2% year-to-date rise in the FTSE 100 is a great result but the UK stock market’s flagship index is still being comfortably outpaced by its international counterparts.

And seen on a longer-term view the FTSE has definitely underperformed relative to other global benchmarks.

In this article we explain why this has happened, which super sectors have contributed to the relative underperformance of the FTSE and what needs to happen in these sectors for this trend to reverse.

We will also look at some of the best performing sectors and consider the strong influence on the index’s performance from Royal Dutch Shell (RDSB), which when its ‘A’ and ‘B’ share classes are both factored in accounts for more than 10% of the index on its own.

WHAT’S ACTING AS A DRAG ON THE FTSE?

It would be easy to conclude that Brexit is behind the FTSE’s woes. This is not the case.

While markets hate uncertainty, the bulk of the FTSE’s earnings come from overseas. This means weakness in sterling, the main barometer of fears over a chaotic Brexit, has actually been a strong catalyst as it boosts the relative value of these foreign earnings.

More relevant are concerns over global growth, a slowdown in China and growing tensions between the US and seemingly all of its major trading partners – to which the FTSE is disproportionately exposed through many different industries.

You need to consider the weighting of the different stocks and sectors in the index. For those who are unfamiliar with this term, it refers to how much of the total market value of the FTSE said industry or share represents.

We have already indicated that Shell makes up in excess of 10% of the FTSE. And, for example, the Oil & Gas super sector in total

has a weighting of nearly 17%. We have calculated a weighting for relevant sectors in the FTSE 100 encompassing those stocks from the sector which have underperformed the wider index to give a clearer picture of what has been dragging on its performance.

BANKS

Weighting in the FTSE 100*: 9.5%

Year-to-date performance**: 6.1%

*Encompassing those stocks from the super sector which have underperformed the FTSE 100 **Based on the average return from constituents of the sector which have underperformed the FTSE 100 year-to-date

Source: Thomson Reuters, Sharepad, 26 April 2019

The banking sector makes up a good chunk of the FTSE 100 with HSBC (HSBA), the second largest stock in the index, accounting more than half of the weighting.

HSBC has gained just 3.2% and because of its large weighting it has distorted the sector return.

We discussed in January three reasons why we believe investors shouldn’t own HSBC. Despite its seemingly attractive dividend yield, we think the stock is higher-risk than it appears because:

– Revenues and earnings are still dominated by the bank’s exposure to China;

– The UK mortgage market is soaking up capital with miniscule returns;

– The investment banking unit is doing the same but with the added downside risk that trading global markets entails.

Barclays (BARC), Lloyds (LLOY) and Royal Bank of Scotland (RBS) are much more focused on the UK retail and commercial banking market and in spite of fears over a Brexit-related slump the domestic economy seems to be holding up.

However, like HSBC, Barclays has an investment banking unit which absorbs a great deal of capital and over the long term has added very little value.

HEALTH CARE

Weighting in the FTSE 100*: 9.1%

Year-to-date performance**: 1.4%

*Encompassing those stocks from the

super sector which have underperformed the FTSE 100 **Based on the average return from constituents of the sector which have underperformed the FTSE 100 year-to-date

Source: Thomson Reuters, Sharepad, 26 April 2019

Holding back the gains from the Health Care Super sector have been volatile share price rides from FTSE 100 listed private hospital operator NMC Health (NMC) and drug manufacturer Hikma Pharmaceuticals (HIK).

Drugs goliaths GlaxoSmithKline (GSK) and AstraZeneca (AZN) have also failed to keep pace with the wider FTSE 100 rally. 2018 was a better than expected year for GlaxoSmithKline, thanks to a strong performance in vaccines and no generic competition for its leading respiratory treatment Advair entering the US market.

Alas, after several delays, a generic entrant was accepted by the FDA at the end of 2018 and the market is pricing in significant earnings declines due to pricing and volume pressure in 2019. Fellow pharma giant AstraZeneca is also fighting off generic competition for some big products, although continued healthy sales of newer drugs - supported by a step-up in R&D spending, could help alleviate market fears.

More recently, AstraZeneca’s shares were knocked by news of a $6.9bn deal with Japan’s Daiichi Sankyo to develop and sell the latter’s breast and gastric cancer drug. This didn’t go down too well with a market seemingly more focused on the deal mechanics than the deal rationale.

PERSONAL & HEALTHCARE GOODS

Weighting in the FTSE 100*: 3.5%

Year-to-date performance**: 4.4%

*Encompassing those stocks from the super sector which have underperformed the FTSE 100 **Based on the average return from constituents of the sector which have underperformed the FTSE 100 year-to-date

Source: Thomson Reuters, Sharepad, 26 April 2019

The Personal & Household Goods super sector includes FTSE 100 housebuilders Berkeley (BKG), Persimmon (PSN), Barratt Developments (BDEV) and Taylor Wimpey (TW.), not to mention packaged consumer goods colossus Unilever (ULVR).

Performance in parts of the sector relative to the FTSE 100 has disappointed year-to-date with gains constrained by uncertainty surrounding tobacco stocks and company-specific concerns at Reckitt Benckiser (RB.). Shares in the consumer health products maker behind Nurofen, Gaviscon and Strepsils have been volatile with the market concerned over recent soft sales growth trends.

CEO Rakesh Kapoor, architect of the transformational acquisition of US baby formula maker Mead Johnson, is retiring and more recently, Reckitt reversed on concerns it could be caught up in a US probe involving Indivior (INDV), which it demerged in 2014, which has been accused of opioid treatment-related fraud. Resolution of this uncertainty is a potential upside catalyst but

Reckitt has already set aside $400m to cover liabilities and the ultimate fine may end up being substantially higher.

Reckitt’s infant formula business derives a portion of its sales from US government contracts and thus could also be at risk. Also weighing on the Super-Sector’s relative showing is Imperial Brands (IMB). Investors remain worried about the ability of next generation products to help offset falling demand for traditional tobacco and there’s also major US regulation uncertainty to fret about.

Sentiment towards Imperial was negatively impacted by the recent announcement of a bill in the US to raise the national minimum age to purchase tobacco products (including e-cigarettes) from 18 to 21.

UTILITIES

Weighting in the FTSE 100*: 2.4%

Year-to-date performance**: - 2.1%

*Encompassing those stocks from the super sector which have underperformed the FTSE 100 **Based on the average return from constituents of the sector which have underperformed the FTSE 100 year-to-date

Source: Thomson Reuters, Sharepad, 26 April 2019

Stock market classification has typically split the wider utility space into component electricity and gas, water and telecoms sectors. But while running a power station, supplying sewage services, keeping the lights on or providing 24/7 internet access on the go may look entirely different these industries are all faced with very similar core problems; an increasingly hawkish regulatory environment, intense competition and the need to invest millions of pounds into their respective infrastructure and networks.

And that cuts to the chase of what links British Gas-owner Centrica (CNA) with mobile phones giant Vodafone (VOD), United Utilities (UU.), the UK’s largest water services supplier, and BT (BT.A) – dividends, and their sustainability at current levels.

Utility companies of most stripes have long held a prominent place in investor portfolios thanks to their implied defensive characteristics, reliable revenues and inflation-proofed income. But this is no longer the case.

Take Vodafone, for example. Its shares have declined nearly 10% so far in 2019 as questions linger over its payout. This year’s forecast €0.15 per share dividend implies an income yield of about 9%, but you know what they say about things looking too good to be true.

Worries persist about sky-high levels of debt, where net borrowings run to about €32bn, or roughly 75% of the company’s £37bn market value. The pinch is exacerbated by significant competitive threats (it was recently voted the worst of the big four UK mobile networks by consumers) and the substantial spending needed to deliver next generation 5G services.

Arguably, Centrica dividend is most at risk among UK utilities. The energy firm has signalled that energy price caps will constrain cash flow this year and has explicitly linked dividends to meeting cash generation and debt targets.

The consensus forecast which underpins Centrica’s forward yield of 9.2% in 2019 is 9.7p which implies a 19% cut from 2018’s 12p figure, but there are some analysts who think a cut considerably larger is possible. RBC is anticipating a 2019 dividend of 8p. Centrica’s credit rating was recently downgraded (pushing up its cost of borrowings) while its British Gas consumer energy arm continues to haemorrhage customers, neither of which is helpful.

Similar questions over dividend sustainability are still to be answered at energy supplier SSE (SSE) and BT, while the water sector has not been immune from hard line demands by its own watchdog, Ofwat.

TELECOMMUNICATIONS

Weighting in the FTSE 100*: 3%

Year-to-date performance**: -5.3%

*Encompassing those stocks from the super sector which have underperformed the FTSE 100

**Based on the average return from constituents of the sector which have underperformed the FTSE 100 year-to-date

Source: Thomson Reuters, Sharepad, 26 April 2019

TRAVEL & LEISURE

Weighting in the FTSE 100*: 3.7%

Year-to-date performance**: -1.7%

*Encompassing those stocks from the super sector which have underperformed the FTSE 100 **Based on the average return from constituents of the sector which have underperformed the FTSE 100 year-to-date

Source: Thomson Reuters, Sharepad, 26 April 2019

The FTSE 100 Travel & Leisure sector is extremely diverse, covering airlines to fast food delivery and hotels, and while the sector is up 4.9% year to date the performance of individual stocks is equally diverse, from -26% to +26%.

Just Eat (JE.) has had a strong run since January helped by a return to profits last year and pressure from an activist investor to up its game.

The two biggest laggards, International Consolidated Airlines (IAG) and TUI (TUI), have been negatively affected by the continuing price war in European air travel with TUI also incurring heavy losses through grounding its fleet of Boeing 737 Max airliners.

For income investors it’s worth noting that the sector is rich in terms of shareholder returns with most companies either paying special dividends or buying back their own shares this year which might help the sector return to favour.

Whitbread (WTB) is returning at least £2.5bn of the £3.9bn cash it received from the sale of Costa coffee to Coca-Cola, beginning with a £500m share buyback ahead of its full year results.

IAG announced is paying a special dividend of €700m or €0.35 per share on top of the ordinary dividend of €0.31 per share, while Carnival (CCL) operates a continual buy-back programme and bought in $250m of shares last quarter.

WHY SHELL IS SO IMPORTANT TO THE FTSE 100

Weighting in the FTSE 100: 10.9%

Year-to-date performance: 5.3%

Source: Thomson Reuters, Sharepad, 26 April 2019

Anglo-Dutch oil major Royal Dutch Shell can have a big influence on the FTSE because it represents more than a tenth of the total value of the index.

The company developed as a combination between Shell in the UK and Netherlands firm N.V. Koninklijke Nederlandsche Petroleum Maatschappij.

This explains why it has an A and B share structure. The A shares face a 15% Dutch withholding tax on dividends but the B shares are exempt from this levy. The performance of the shares, while firmly in positive territory year-to-date, has lagged the FTSE 100.

This might come as a bit of a surprise given the strong recovery in oil prices and given that its closest peer on the UK market BP (BP.) is up around 13%.

The shares may have been held back by reports of potential criminal charges in the Netherlands relating to corrupt practices in Nigeria.

However, the longer oil prices remain above $70 per barrel, the greater faith investors might have in the company’s dividend which

at a share price of £24.70 implies a dividend yield of nearly 6%.

A strong second half showing for Shell could have positive implications for the FTSE 100’s performance in the remainder of the year.

Which parts of the FTSE 100 have been doing well and can they keep it up?

The retailers have had a strong start to 2019, with several of the sector’s constituents among the top performers including Tesco (TSCO) whose turnaround under chief executive Dave Lewis has continued to gather momentum.

Whether this can continue is likely to depend on the jobs market, if the recent uptrend in ‘real’ – that is adjusted for inflation – wages can continue and if a chaotic Brexit ends up hurting consumer sentiment.

Mining behemoth Rio Tinto (RIO) and oil heavyweight BP have both contributed to the FTSE’s gains. While Rio’s strong performance also reflects a very resilient first quarter showing in the face of several operational challenges, their fortunes are likely to remain closely tied to volatile commodity prices.

Individual heavyweight stocks which have contributed to the FTSE’s rise include global insurance business Prudential (PRU) and

British American Tobacco (BATS). Prudential has enjoyed a recovery rally after a disappointing share price showing in 2018. Full year results which came in slightly ahead of expectations acted as a catalyst.

British American Tobacco has also enjoyed a rebound, having hit multi-year lows in early January on regulatory and competition concerns.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.