Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat next for Sainsbury’s after failed Asda merger blow?

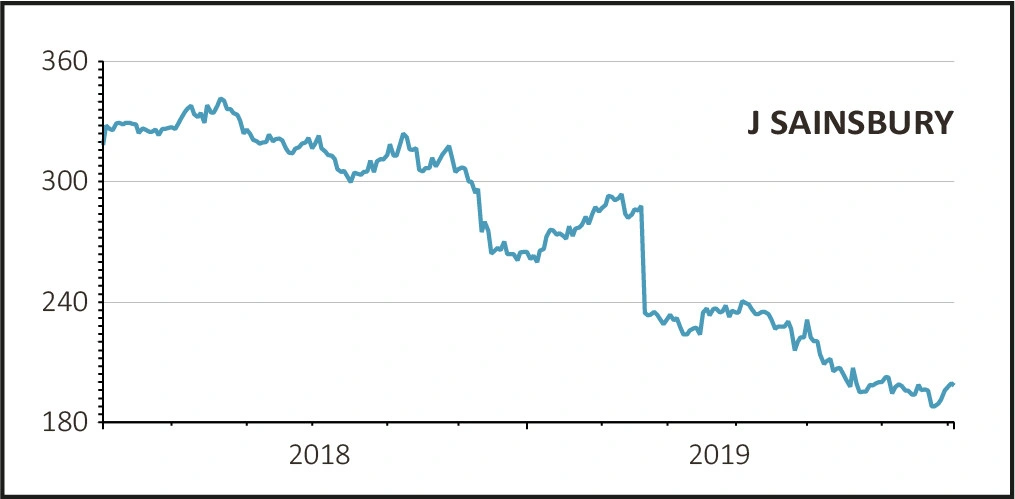

Shares in supermarkets operator Sainsbury’s (SBRY) rallied off a low base on better than expected full year results (1 May), but this could prove a false dawn for the embattled grocer.

Chief executive officer (CEO) Mike Coupe is under immense pressure to show his charge can succeed as a standalone business and having squandered an eye-watering £46m in fees on a failed merger attempt with Asda.

POSITIVE SURPRISE

Sentiment towards Sainsbury’s is poor, with the Competition & Markets Authority’s prohibition of its bold merger with Asda representing a huge body blow to Coupe and the entire Sainsbury’s investment case at a time when established rivals are reinvigorated and German disruptors Aldi and Lidl remain rampant.

Following on from Kantar grocery share data (30 Apr) showing a 1.2% sales decline for the 12 weeks to 21 April, the retailer’s results for the year to 9 March were not as a bad as feared, with underlying pre-tax profit and the dividend both up 7.8% to £635m and 11p respectively and net debt ahead of target.

However, profit was boosted by synergies from 2016’s Argos acquisition as well as a reduced interest bill. Furthermore, reported pre-tax profit fell from £409m to £239m after pension scheme costs and the aforementioned £46m of Asda-related costs.

A ROTTEN CORE?

Worryingly, Sainsbury’s core supermarkets underperformed the UK grocery market for much of the financial year and like-for-like grocery sales were down a disappointing 0.6% in the fourth quarter to 9 March.

Given that backcloth, Coupe needs to devise a ‘Plan B’ in light of the Asda debacle. It appears he is being given time for a strategy refresh. The market will have to wait until an investor day on 25 September for more details.

What we do know is Sainsbury’s will be increasing and accelerating investment in a core business that must surely have been neglected while Coupe & Co were distracted by Asda. Coupe is also making a new commitment to pare net debt ‘by at least £600m over the next three years’.

UNCERTAIN OUTLOOK

In terms of the outlook, Sainsbury’s laments retail markets which are ‘highly competitive and very promotional’, with the discounters and Co-op gaining share from the rest of the market, while describing the consumer outlook as ‘uncertain’.

Shore Capital seems unconvinced, seeing ‘no cost-free or quick turnaround’ for the supermarkets or Sainsbury’s Bank and believing the outlook is ‘challenged’. The broker also worries about the trajectory of earnings per share and the supermarket’s dividend paying capabilities.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.