Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy the recovery at Luceco looks attractive

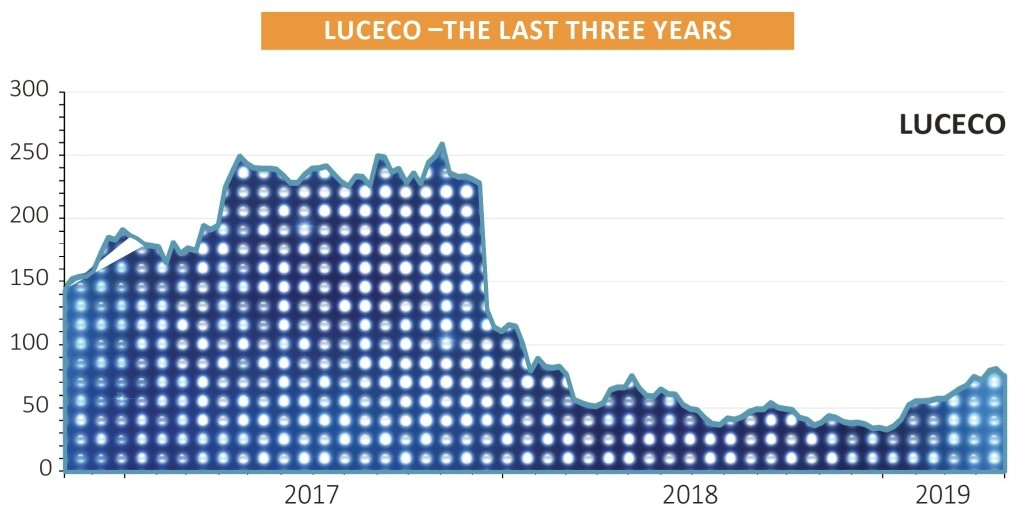

LED lighting and electricals manufacturer Luceco (LUCE) is on track to roughly double pre-tax profit in 2019 as it bounces back from a series of problems. These challenges have included retail-facing customers running down existing LED stocks and price increases on key raw materials, particularly copper.

But it was the disastrous stock and currency mis-management that really hurt, smashing profit margins to pieces and causing the company to issue two profit warnings, first in December 2017 and then again in March 2018.

This has left the company’s 2018 trading performance deeply scarred and the share price significantly discounted. But the stock market is forward-looking and we believe more recent positive noises from the company make this an opportune time to revisit the longer-term investment story.

WHAT DOES LUCECO DO?

The Telford-based business operates supplies a large collection of electrical products to both retail and wholesale suppliers, covering industries such as commercial construction, residential housebuilding and housing maintenance operators, what is often called the RMI market, or repair, maintenance and improvement.

Customers investors may have heard of include FTSE 100 plumbing supplies group Ferguson (FERG) – previously known as Wolseley – Travis Perkins (TPK) and Grafton (GFTU), plus major DIY chains such as Homebase and the Screwfix and B&Q chains owned by Kingfisher (KGF).

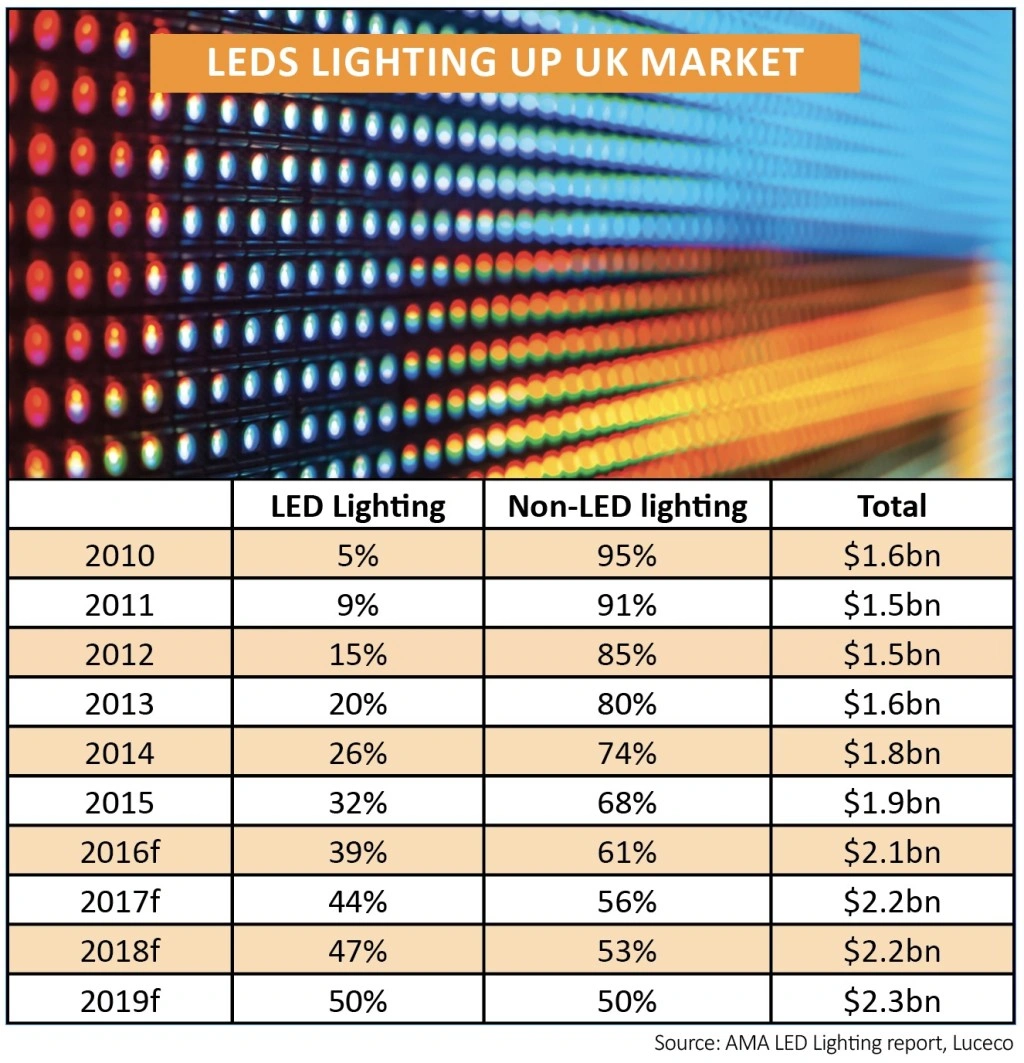

Luceco operates through four brands – BG (wiring accessories), Masterplug (extension leads, cables and portable power) and Ross (TV wall mounts). The final leg is the Luceco branded LED lighting business.

The LED business is the one that retail investors are likely to know best. Since the company joined the stock market in October 2016 is frequently referred to as LED lighting company Luceco.

This is a little misrepresentative since the LED lighting business was built from scratch just five years ago. While is does offer promising growth potential in the future its profit track record is patchy.

In contrast, the wiring and cables businesses have been around for decades and have had time to establish themselves as go-to suppliers of market leading products where quality and safety is more important than price. Who wants to buy cheap where 240 volts is concerned?

BG and Masterplug accounted for two-thirds of revenue in 2018 and nearly all of the £8.5m pre-tax profit, after adjustments.

WHAT WENT WRONG?

While managing end customer demand and commodity pricing are largely part of the normal cycle of doing business Luceco holds up its hands on the inventory miscalculation mistakes made. That led to the resignation of the company’s financial controller at the time and prompted a detailed rethink of internal controls and processes.

This resulted in significant investment in things like sales and marketing, product development while also streamlining parts of the business, including closing down its small US operation.

What this means is that costs needed to get the business back on track are now largely sunk with the rewards still to come.

So while 2018 results to 31 December, announced on 9 April, looked ugly the company’s rhetoric is becoming increasingly optimistic.

‘We currently have a strong order book and revenue growth is running in line with expectations,’ chief executive John Hornby said then, before adding his confidence that operating profit for 2019 will be ‘comfortably ahead of current market expectations.’

Operating profit forecasts had been pitched at £13m for 2019 but unsurprisingly analysts at broker Numis still lifted their estimates by another £1m to £14m even after having previously upgraded 2019 estimates as recently as January.

Importantly for the medium-term, operating profits are now expected to continue their rapid recovery into 2020, with Numis now anticipating £16.5m, implying 18% growth.

This is possible through the combined dynamics of solid single-digit revenue growth, a lower-cost manufacturing base in China, plus rebuilding operating profit margins from high single-digits forecast for 2020 back to the mid-teens of a few years ago.

There are still challenges to overcome, not least ongoing questions about the sustainability of global growth, as well as Brexit uncertainty and what that might do for exchange rates and commodity pricing.

SHARES SAYS: Luceco’s destiny feels back in its own hands and looks like a relatively lower risk recovery-to-growth story on a 2019 price to earnings multiple of 13.4-times, based on a 78p share price.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.