Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

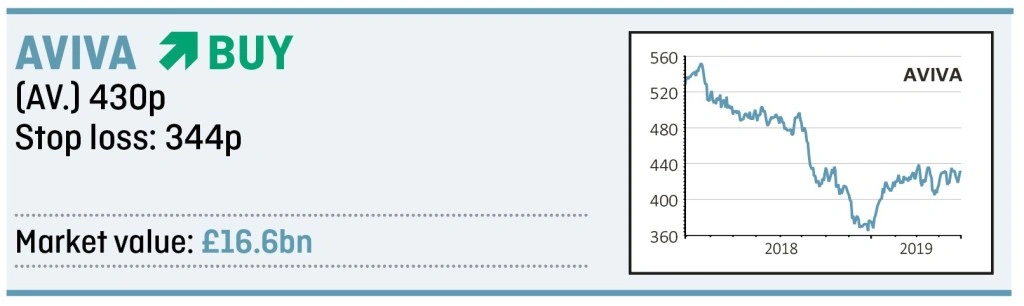

magazineAviva’s shares are too cheap to ignore at a 7.3% yield

We believe Aviva (AV.) looks very interesting at the current price as its shares are cheap and a new CEO could reshape the business.

Anyone investing in the shares must understand that change could take time, however the potential rewards look very good.

‘Aviva is undergoing a revolution in its balance sheet strength that will leave the group with more equity, less debt and more prudent asset and liability valuations than consensus expects, thus ensuring long-term dividend sustainability,’ says Jefferies analyst Philip Kett.

Aviva is the UK’s largest composite insurance company with around half of sales coming from its home market and half from Canada, France, Holland, Ireland and Poland.

Most of its sales come from life insurance where customers and premiums tend to be ‘stickier’ than in household or car insurance although it has a top three UK share in non-life markets.

Aviva looks undervalued at 8.2 times this year’s earnings and less than 8 times next year’s. In comparison, Prudential (PRU) is valued at 11-times and 10-times respectively while Swiss Life is valued at 14-times and 13-times.

In October chief executive officer Mark Wilson stepped down, supposedly over a disagreement with the board over strategy. He has since been replaced by Maurice Tulloch who says he will simplify the business.

MARKET CONCERNS

The current concerns hanging over the shares are Aviva’s high debt levels compared with its peers and its perceived lack of earnings growth. The company said in April that sustaining momentum for operating earnings this year would be difficult.

Operating profit grew just 2% in 2018 and the average growth rate for the next three years is estimated to be just 3% to 4%, but improvements to its balance sheet combined with the lowly valuation make Aviva stand out.

‘Aviva continues to invest in improving customer service by reducing the complexity at both the point of sale and claim,’ comments Kett. ‘The aim is to increase customer retention and shift from the industry norm of strained / adversarial customer relations. Like the market, we struggle to value this but acknowledge that if it be achieved, this would be a paradigm shift in the insurance business model.’

Its dividend policy was recently reset so that payments progress in line with growth in earnings, which disappointed the market but gives Aviva the flexibility to reduce its debt or invest more in the business.

Despite these change the shares are still very attractive from an income perspective. It is forecast to pay 31.5p in dividends for 2019, implying a 7.3% yield.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.