Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDo commodity prices suggest stock markets are right to be bullish?

A surge in the oil price to six-month highs above $70 a barrel, using Brent crude as a benchmark, is grabbing a lot of headlines.

Uncertainty over Libyan and Venezuelan output is contributing to crude’s gains but a greater near-term influence appears to be US president Donald Trump’s determination to exclude Iranian supply from global markets.

The White House is withdrawing a sanctions waiver from eight nations who buy oil from Tehran with the likely result that around 1.2m barrels of oil per day (bopd) will be unavailable – no small matter in a market where supply and demand are already finely balanced around the 99m bopd mark.

That said, Trump is already calling on OPEC, and Saudi Arabia in particular, to increase output to ensure that oil prices do not rise sharply. A big jump in prices at gas stations is the last thing Mr Trump will want to see, as it may jeopardise his target of 4% GDP growth and also dent consumer confidence as he prepares for the November 2020 Presidential election.

And this shows the inherent difficulty of investing in commodities, as so many factors can affect supply or demand in the near term. They can be related to technical issues, the weather, geopolitics, human error, changes in taste or fashion, disease and currency movements, as well as economic growth.

Wide range of results

Wide range of results

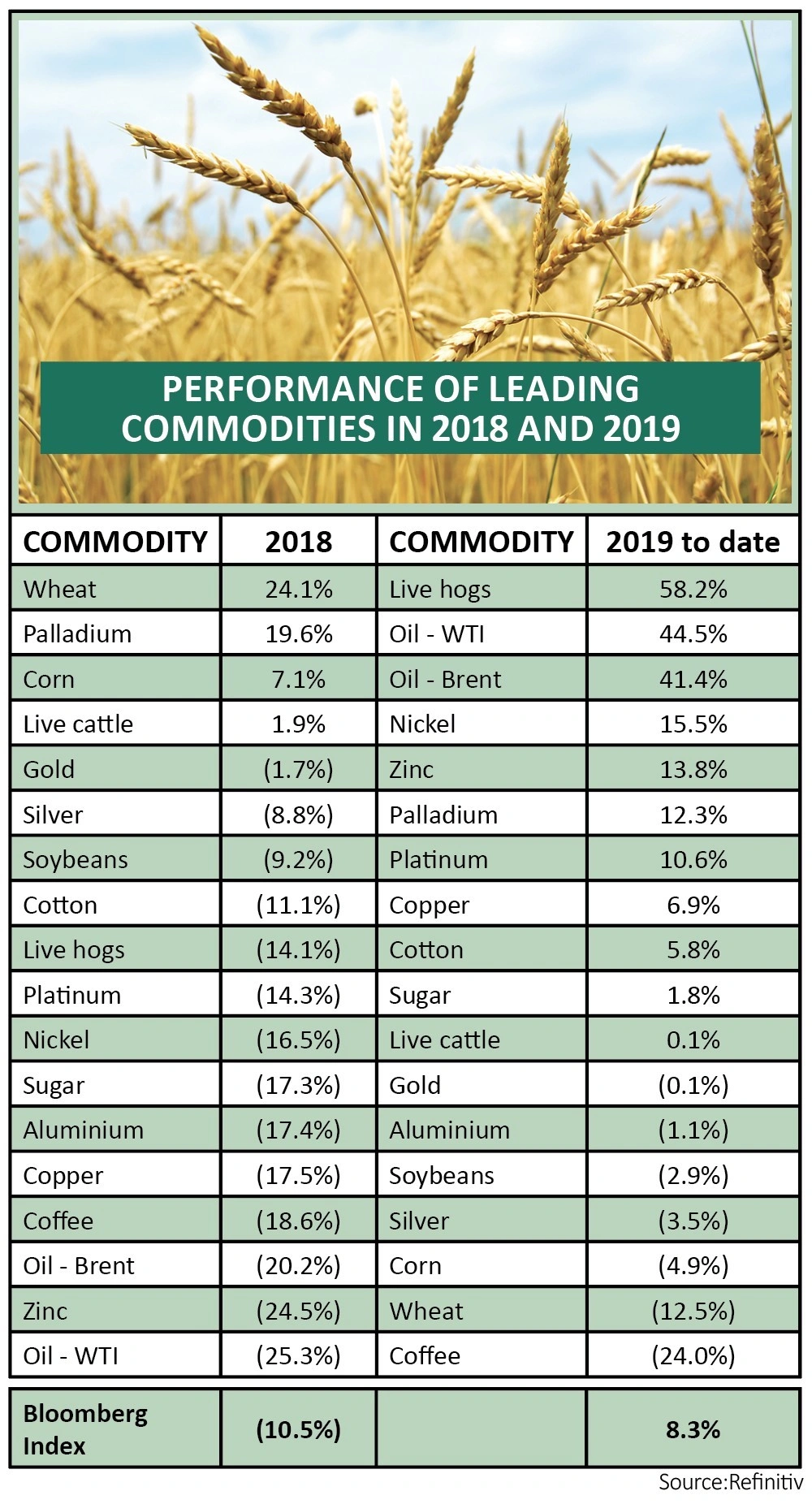

These challenges are reflected in the performance of individual commodities in 2018 and 2019. Very few clear trends emerge over the last 16 months.

The exceptions being perhaps the strong gains made by palladium, helped by a switch by car-buyers from diesel to petrol cars following a string of emissions scandals; a fall in coffee, due to last year’s bumper Brazilian crop and a drop in Brasilia’s currency, the real, which is fuelling low-priced exports; and the failure of gold and silver to do much at all.

You would have needed a crystal ball to spot (and buy) the best-performing individual commodities of 2018 and 2019 to date.

Last year, wheat sat on top of the pile, thanks to hot and dry conditions hitting supply of American hard red winter wheat and crops grown in Southern Russia.

This year’s biggest gainer so far are live hogs. An outbreak of African swine fever in China, home to the world’s largest pig population, is driving prices higher amid fear that up to 130m animals, or a third of the total Chinese drove, could be lost.

Global trends

The lack of a yield and their price volatility may still deter many investors from seeking exposure to commodities and they may not be suitable or appropriate for everyone. Those who do feel raw materials may offer some useful diversification in a balanced portfolio still have to address the question of how best to address the asset class.

The wide range of performance between individual commodities means that time-pressed investors are unlikely to want to take the risk of trying to choose between the ‘right’ and ‘wrong’ commodities at any given time.

They may instead prefer to seek broad-brush exposure, via a tracker which follows a basket of materials of a fund that invests in quoted companies that are involved in agriculture, energy or mining.

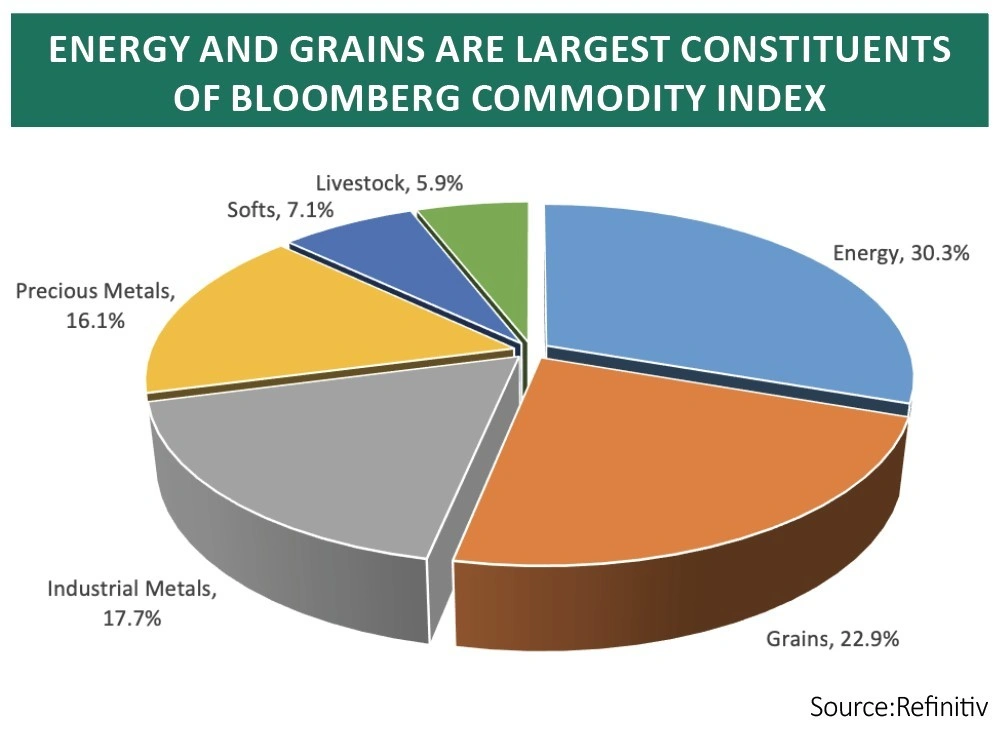

This strategy is at least gaining some succour from a solid performance in 2019 to date of the Bloomberg Commodities index, a basket of 23 raw materials following this year’s first-time inclusion of low-sulphur gas oil.

The 10% fall in the benchmark in 2018 is easy to understand in the context of the global growth scare and equity market sell-off which gripped financial markets in the fourth quarter. And this year’s 8% advance looks to make sense in the context of a recovery in the US equities in particular, but also the broad FTSE All-World index, which is up by a handy 15% in 2019 to date.

This gain may also give buyers of bonds some pause for thought, if it does mean that a truly inflationary recovery is finally upon us.

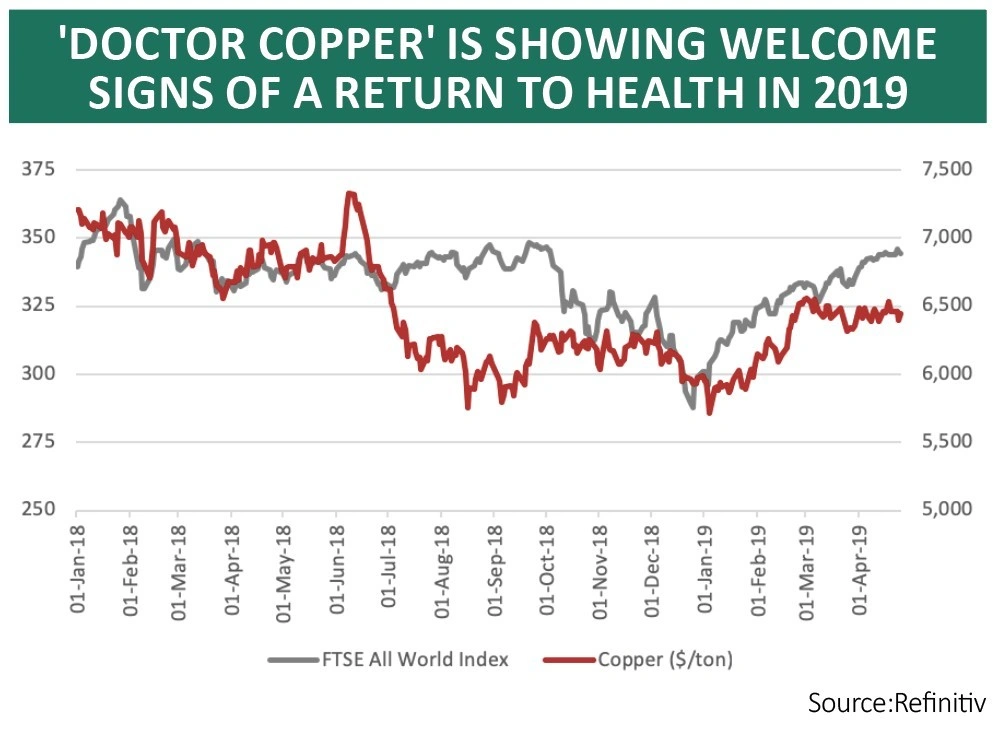

The situation is still far from clear cut, since energy represents 30% of the Bloomberg Commodity Index, oil’s 40%-plus gains this year will be exerting great influence over the benchmark. But those investors who are bullish on equities (or commodities for that matter) may be able to draw some comfort from a 6% gain in ‘Doctor Copper’, the ductile, malleable widely-used metal which is traditionally seen as a good guide to the health of the global economy.

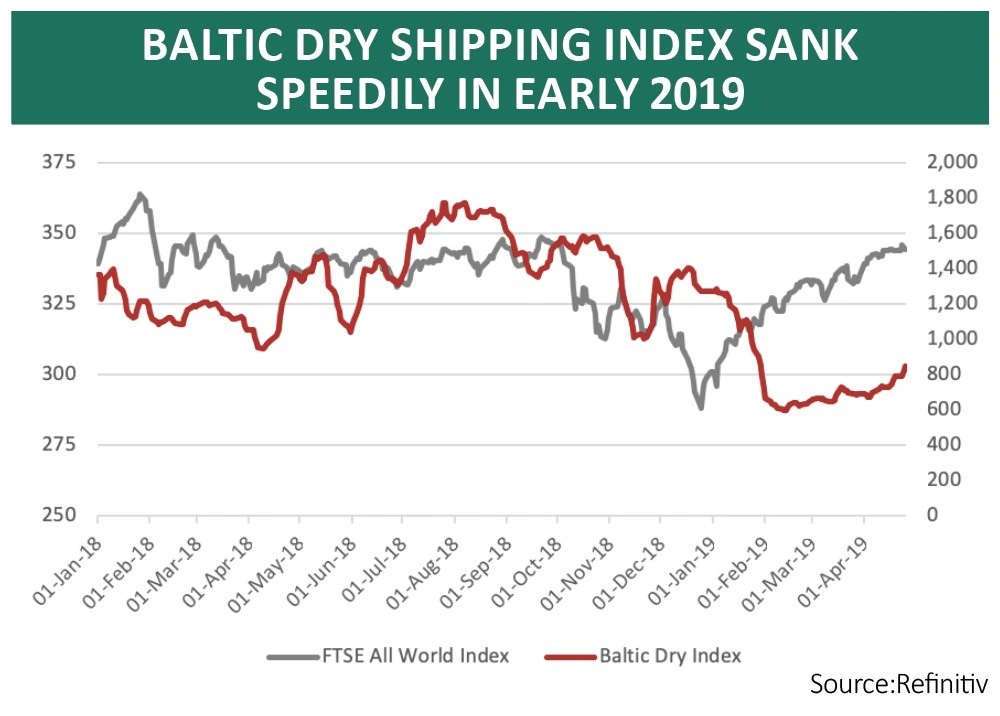

One potential warning sign, however, remains the Baltic Dry shipping index, a measure of activity in dry bulk cargoes such as grains, ores, coal and building materials. It is still down by around a third this year, to perhaps reflect weak global trade flows, and a recovery here would provide some comfort that equity and commodity markets are right to have faith in the globe’s economic growth prospects for 2019 and beyond.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.