Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBrexit deal and vaccines: Why UK stocks can break free from lockdown shackles

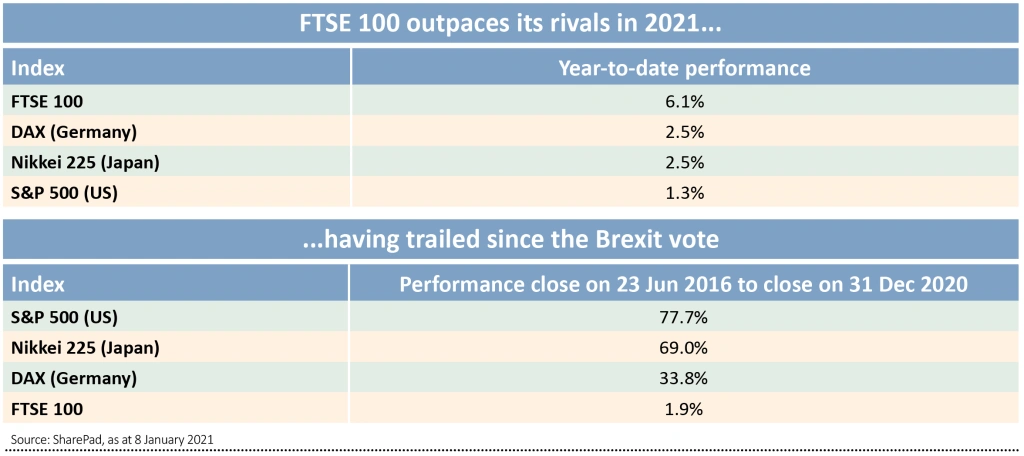

We are championing UK stocks despite the introduction of the latest lockdown measures. For more than four years London-listed shares have trailed in the wake of nearly all other major global markets, but the early Christmas present of a Brexit deal should end much of the uncertainty which led to this underperformance.

We are already seeing a dramatic reversal in fortunes with the FTSE 100 going from one of the worst performers in recent years up until the end of 2020 to one of the best in 2021 to date.

While Covid-restrictions will extend and deepen the economic impact in the first quarter of the year and have a big impact on certain sectors, the UK is also well placed for a vaccine roll-out.

The AstraZeneca (AZN) and Oxford University jab is being manufactured in the UK and unlike in some countries most Britons seem happy to receive it.

UK stocks may have enjoyed some gains since late December 2020 but there could be a lot further to go as we move from Covid restrictions to a reopening of society. In this article we flag five ways to play a bounceback for Britain.

What a Brexit deal means for UK stocks

Catalysts linked to a Brexit deal should help UK shares play catch up in 2021. An agreement could act as a driver for money from both inside and outside the country, which has been sitting on the side-lines pending clarity on the future relationship with Europe, to flow.

In a briefing note after the deal consultancy the Centre for Economics and Business Research said: ‘We would expect business investment in the UK, which has been very subdued since the 2016 referendum, to recover in 2021.’

As we discuss below, it also creates more favourable conditions for incoming M&A as overseas predators look for undervalued opportunities on these shores.

In terms of the immediate market response, after fears we were heading for an end to the Brexit transition period without an agreement proved unfounded, domestic-facing stocks rallied.

Some of the most popular investments being bought by customers of the AJ Bell Youinvest investment platform in the weeks since the Brexit deal was announced include Lloyds Banking (LLOY), and ETFs with a UK focus like iShares Core FTSE 100 (ISF) and Vanguard FTSE 250 (VMID).

Stocks and funds with global horizons like pharmaceutical giants AstraZeneca (AZN) and GlaxoSmithKline (GSK) and popular global growth investment trust Scottish Mortgage Trust (SMT) were in favour too.

The advances for UK-focused assets were concentrated on 23 December and the morning of 24 December amid anticipation a deal would be reached built. The retail, housebuilding, financial and real estate sectors were among those most in demand as the table of best-performing stocks shows.

After the deal was announced a portion of these gains was eroded and sterling’s gains against other major currencies were more muted than some had forecast.

This may have reflected the market adage that it is better to travel than arrive when investing but could also imply some disappointment over the details of the deal.

After all, not everything has been resolved by the trade agreement. Nigel Green, CEO of deVere Group comments: ‘Let’s be very clear. Whilst better than nothing, this UK/EU deal is a thin and narrow one. It only covers goods, not services, which account for 80% of the UK economy – and even with an agreement for goods there will be additional rules and further costs.’

Edward Park, chief investment officer at Brooks Macdonald says: ‘Services are a problem for 2021 but this is where the EU imports more from the UK than the other way round, so this could be a particularly difficult area. It is the importance of services to the UK economy and poor 2021 growth forecasts which explain the fairly muted response by the markets to (the) trade deal.’

A lot of focus has been on the negotiations around financial services given how central the City of London is to the UK economy. Most observers expect limited access for UK institutions into Europe. The long-term impact of this on the City is hard to determine but it is worth noting it has been a major centre for global finance for an extremely long period of time, pre-dating UK membership of a European trading bloc.

Could Brexit deal prompt UK M&A boom?

According to data from Refinitv companies have agreed more than $2.3 trillion worth of deals since July 2020, an 88% increase from the first half of last year which was interrupted by the pandemic.

Cheap money and coordinated central bank and government stimulus has emboldened corporates to look through the pandemic towards economic expansion once economies reopen.

Now that Brexit risk has been removed there could be a flurry of mergers and acquisition (M&A) activity looking to take advantage of the UK stock market’s laggard performance as well as sterling weakness.

Almost on cue, on the first business day of the new year gambling giant Entain (ENT), formerly GVC and owner of Ladbrokes received a takeover offer from its US partner MGM Resorts International.

The all-share offer valued the company at £13.83, representing a 22% premium to the prior closing price.

Management have rejected the offer on the grounds that it undervalues its prospects to exploit the $20 billion US opportunity over the next few years.

LOCKDOWN 3.0 IMPACT

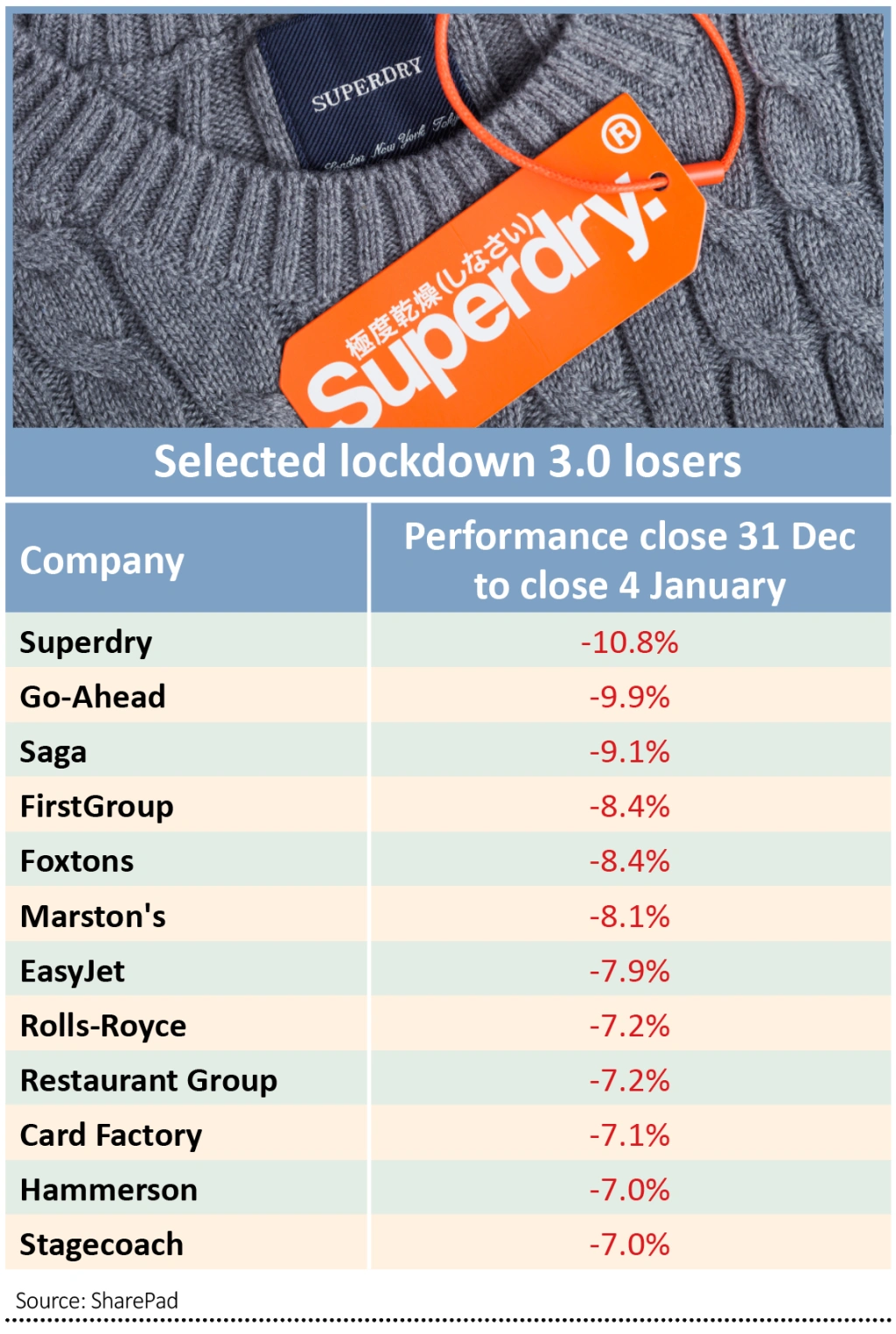

In anticipation of prime minister Boris Johnson’s latest lockdown, now in place and set to last until at least mid-February, shares in a number of lockdown losers weakened (as the SharePad data from the close of trading on 31 December to the close of play on 4 January illustrates).

These included the likes of London-focused estate agent Foxtons (FOXT), shopping mall operator Hammerson (HMSO) as well as travel and leisure names such as budget airline EasyJet (EZJ) and cruise operator Carnival (CCL).

News of a third lockdown provided another hammer blow to non-essential retailers including greetings cards-to-gift bags seller Card Factory (CARD) and Primark, the discount retail arm of Associated British Foods (ABF) now expected to suffer as it did back in Spring 2020.

Other companies that could find life exceptionally difficult include leisure group Hollywood Bowl (BOWL) and the commuter footfall dependent sandwiches-to-salads maker Greencore (GNC), among the main casualties of the structural work from home shift triggered by the pandemic.

However, tighter restrictions should provide another boost to the major supermarkets including Tesco (TSCO), Sainsbury’s (SBRY) and Morrisons (MRW), as well as other designated ‘essential retailers’ upon which the nation will once again rely.

Sainsbury’s (SBRY) reported (7 Jan) a record increase in sales over the Christmas period, enabling the UK’s second largest supermarket to raise full year earnings guidance. Lockdown 3.0 should provide a further boost to both its brick and mortar and online grocery sales, while also sustaining the positive momentum behind its toys-to-home products business Argos.

Others strongly positioned for restrictions include essential retailers such as B&Q-to-Screwfix owner Kingfisher (KGF), which has seen its sales soar as people stuck at home splash out on home improvements. Another noteworthy name is B&M European Value Retail (BME), the general merchandise discounter that has traded unencumbered during the pandemic. B&M reported (7 Jan) strong sales for the third quarter including Christmas and thanks to its copious cash generation and strong balance sheet, treated investors to a third special dividend since March 2020.

Pets at Home (PETS) could continue to take market share across all channels during lockdown as UK consumers prioritise spending on the health and wellbeing of their canine and feline friends.

Other potential beneficiaries of a brick and mortar shutdown are the online retailers including web-based electricals seller AO World (AO.), online musical instruments seller Gear4music (G4M:AIM) and fast-fashion retailers Boohoo (BOO:AIM) and ASOS (ASC:AIM). Restrictions on social life will also create helpful conditions for online wine retailer Naked Wines (WINE:AIM), which should do well as pandemic-induced stress encourages online wine ordering.

Elsewhere, chocolatier Hotel Chocolat (HOTC:AIM) has proved effective at switching channels from its stores to online and third-party partners in response to the pandemic and could profit from gifting spend around Valentine’s Day and then Easter.

THE BIG REOPENING

Should coronavirus vaccinations be rolled out in record time and a majority of the population gets immunity by spring, the sectors of the economy hardest hit by lockdown measures could very well be the ones that bounce back strongest.

This includes the travel sector, as well as leisure and hospitality, with businesses in these areas forced to close outlets or stop the majority of operations to curb the spread of the virus.

Statistics from the Bank of England show high levels of consumer cash savings during lockdown, with over £150 billion put into cash accounts last year.

That combined with pent-up demand for everything from a holiday to a trip to the cinema or a good meal out, could well translate to a big recovery in revenue and earnings for firms in the travel and leisure sectors in the second half of this year.

In travel in particular, the market is pricing in a large degree of recovery by summer with a number of airlines and tour operators – particularly Ryanair (RYA), Wizz Air (WIZZ) and On The Beach (OTB) – either above or nearing their share price a year ago.

According to forecasts compiled by Refinitiv, most of the airlines and tour operators should see a large degree of recovery in earnings during 2021 with a full recovery by 2022, or early 2023 at the latest.

There is a consensus among analysts and fund managers that there is a lot of pent-up demand for holidays, and tour operators TUI (TUI) and Jet2 (JET2) previously reported that summer bookings for 2021 have been ‘encouraging’.

However some stocks, notably EasyJet (EZJ) and TUI, remain 50% down on their share price pre-pandemic, with concerns centering around their balance sheet compared to their peers.

For example TUI is saddled with over €5 billion in net debt, and while EasyJet has a more manageable £1.1 billion debt load, its cash burn remains notably above the level of its peers.

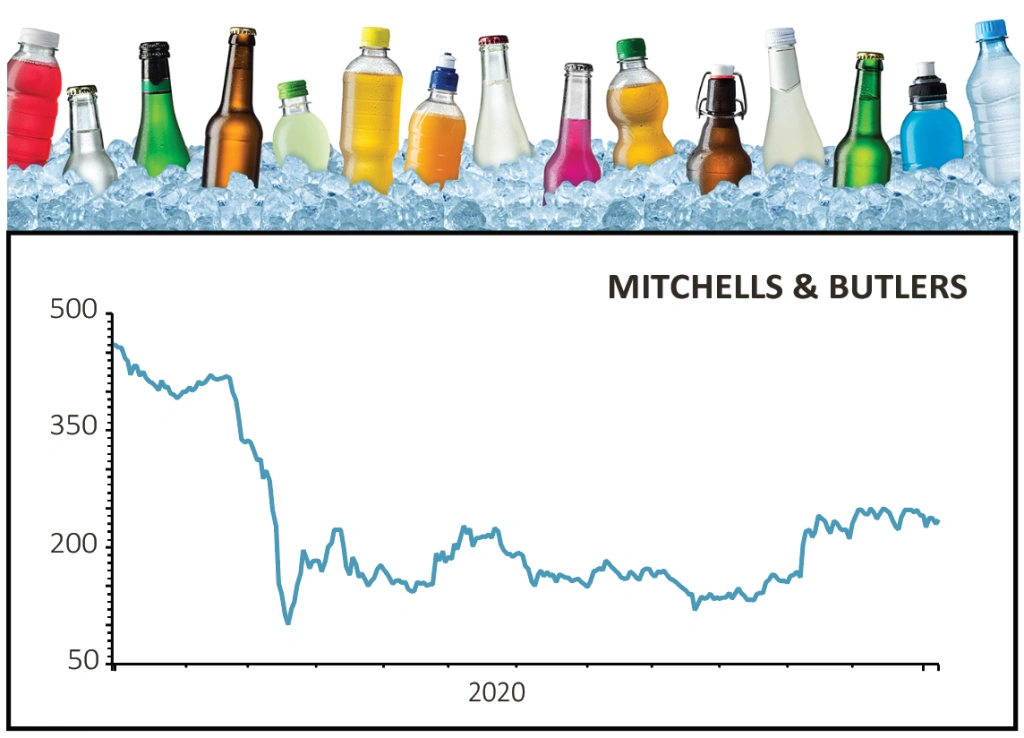

Meanwhile hospitality could be the area to benefit most if the vaccine rollout is successful and most restrictions are lifted in the second quarter of the year, especially as valuations are still depressed for virtually all stocks in the sector.

The share prices of pub groups like JD Wetherspoon (JDW) and Mitchells and Butlers (MAB) are still around 30% and 50% below their pre-pandemic levels, yet according to consensus forecasts compiled by Refinitiv, both are expected to swing back into profit this year and bounce back completely by 2022.

It is worth considering however comments by Mitchells and Butlers in its first quarter trading update, in which it welcomes ‘recent positive news on vaccine approval and roll-out’ but warns the future facing the sector ‘remains extremely uncertain’. The firm adds, ‘It is not possible to estimate with any confidence what restrictions on our ability to trade lie ahead of us and for how long.’

For all these businesses, one important factor to consider is that those first booming months after a recession has peaked can sometimes be the most dangerous, as overtrading sets in and supply doesn’t keep up with demand. This presents a real danger of a business potentially going bust very quickly.

Why? Relief over the reemergence of growth post-recession can be met with firms going back into panic mode, hiring more staff and buying higher amounts of supplies to keep up with increased demand.

But this can cause a problem with cash flow because there’s a time lag between investing to keep up with demand and actually being paid. By the time supplies have been bought, manufactured and the customer has paid, that can be a long period of time and an acute shortage of cash can develop rapidly.

This mainly affects firms in the manufacturing sector but can be applied to other sectors and has been seen in the past with airlines and tour operators, as well as pub and restaurant firms.

Can property market gains be sustained?

The housing market roared back from the March 2020 lockdown and the newly introduced restrictions leave this space largely untouched. After emerging from deep freeze in May, the introduction of a stamp duty holiday on property transactions in July supercharged house prices. Nationwide reported that UK house prices rose another 0.8% in December, taking the total increase for 2020 to 7.3%.

There is concern about what happens when the stamp duty relief ends in March, particularly given rising unemployment and the new lockdown measures. Shares’ conversations with suppliers and service providers to the property market in recent months have suggested some confidence there will be a further Government intervention to support the market, possibly by extending the stamp duty relief period.

There is logic to this when you consider the Conservatives like to style themselves as the party of home ownership and such a move would be a clear positive for the housebuilding sector. Liberum Capital analyst Charlie Campbell says that balance sheet risk has been largely eliminated with most sector constituents enjoying net cash positions.

‘Anyone worried about the impact of widespread job losses on the property market should consider that those most at risk of unemployment are more likely to rent than to own homes’, he adds.

FIVE WAYS TO PLAY A BOUNCEBACK FOR BRITAIN

Bellway (BWY) £29.39

That Bellway (BWY) was one of the first housebuilders to announce a return for dividends should not come as a surprise given it sustained dividend payments throughout the 2007/8 financial crisis. It also has a long track record of growing volumes which can help offset margin pressure if there is a dip in house prices.

Catalysts include potentially positive trading updates scheduled from its peers in January and any further support doled out for the housing market by chancellor Rishi Sunak. In a December 2020 trading update Bellway reported net cash of £242.9 million and a forward order book up 18.7% to £1.77 billion. This should underpin plans to grow the payout and invest in land at an opportune moment in the cycle when valuations are depressed.

Based on Liberum forecasts for the July 2022 financial year the shares offer an attractive yield of 3.5% and trade in line with net asset value (NAV) compared with an average premium to NAV of 59% for the wider peer group (though this number is inflated somewhat by the premium ratings enjoyed by Persimmon (PSN) and Berkeley (BKG)).

Hays (HAS) 148p

Recruitment companies such as Hays (HAS) are typically the first to see an improvement in the economy. That’s because when firms plan to grow they usually need to hire more people.

Deutsche Bank recently turned positive on the sector saying staffing agencies could fully benefit from the recovery at the start of the economic cycle.

Hays has been expanding its global footprint over the last few years to over 33 countries across 20 different sectors and today the UK generates 23% of the firm’s net fees.

In the difficult 2020 financial year Hays achieved all its profits in the first nine months to March with the final quarter breaking even. Overall profits dropped by 45% to £135 million.

Hays is strategically well positioned to profit from economic recovery with 44% of its business exposed to cyclical markets and 56% exposed towards structural growth.

WHSmith (SMWH) £15.36

A vaccine-driven recovery in global travel numbers should reignite the growth story at WH Smith (SMWH), the books, magazines and snacks retailer with a balance sheet robust enough to weather the remainder of the crisis.

WHSmith’s long-run bull case has centred around the opening of international airport and train station stores, so it has been hit hard by the suspension of flights and the fact flocks of commuters are now working from home. Bold investors should look past the figures for the current year to August 2021 and focus on 2022, when the recovery of the travel business should (hopefully) be underway.

Broker Peel Hunt expects the US to emerge quickest from the crisis as 85% of the country’s air travel is domestic. Closer to home, the end of lockdowns will ride to the rescue of the embattled UK high street business.

During the pandemic, Carl Cowling-led WHSmith has cancelled the dividend and boosted liquidity whilst bearing down on costs, so the retailer will benefit from a positive operational gearing effect as the global travel market returns to growth.

Mercantile Investment Trust (MRC) 250.5p

If you want a broad spread of assets to tap into Britain’s bounce back potential the JP Morgan-run Mercantile Investment Trust (MRC) is an excellent option. Exclusively focused on the UK, but geared particularly to the FTSE 250, investors get exposure to many of the sector themes we have discussed.

Housebuilder Countryside Properties (CWY) join robust retailers like Dunelm (DNLM) and Games Workshop (GAW). Bus and coach operator National Express (NEX) is also in the portfolio alongside other industrial, financial and consumer stocks that could benefit from improving economic stability.

Past performance is impressive, the stock outstripping its investment trust all companies benchmark over one, three and five years as its typical 8% to 9% discount to net assets narrowed to just 0.2% now. Net asset premiums of the past are not out of the question given total returns of more than 12% a year over the past decade, based on Morningstar data, twice that of its benchmark.

Annual charges of 0.44% are relatively inexpensive for an active fund, while it pays quarterly dividends designed to match or better inflation that promise a 2.6% income yield.

Vanguard FTSE 250 (VMID) £33.19

The FTSE 250 is well-known for being easiest way to play UK stocks, and so for investors looking to get exposure to the great British economy it should naturally be the index of choice.

However, it is perhaps less exposed to UK than investors may think with around 50% of companies in the index focused on the domestic economy. That means investors would therefore get overseas diversification as well, which could act as a nice support as economies across the world also stage a recovery.

The best way to play the FTSE 250 is through the Vanguard FTSE 250 (VMID) exchange-traded fund (ETF). This ETF is the cheapest of all the options available, with a total expense ratio of 0.1% a year. It’s also the most popular, meaning the extra cost of buying and selling (the bid-ask spread) is lower than for other FTSE 250 ETFs. For the dividend-paying option, choose the aforementioned ETF, but if you want dividends reinvested go for the accumulation version, Vanguard FTSE 250 ETF GBP Acc (VMIG).

AJ Bell is the owner and publisher of Shares magazine. The editor (Daniel Coatsworth) and all of the authors own shares in AJ Bell referenced in this article. The editor (Daniel Coatsworth) owns shares in Vanguard FTSE 250 UCITS ETF and one of the authors (Steven Frazer) owns shares in Scottish Mortgage Investment Trust also referenced in this article.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

First-time Investor

Great Ideas

- Alibaba faces baptism of fire at start of 2021

- IP Group still offers upside as it eyes further realisations

- Play a regional recovery with BlackRock Latin American

- Buy Sainsbury's now before the shares surge

- Gamma run could speed up if it can nick a bit of Twilio’s limelight

- Recent acquisition provides growth and security for Gresham House