Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat to do with lockdown cash

Another lengthy lockdown is upon us and that means few options to spend money on the little pleasures we took for granted before the pandemic. But when you put together all the money spent on meals out, coffee stops, evenings in the pub, or just getting a haircut, it actually adds up to a pretty tidy sum.

As a result £120 billion was saved into bank and building society accounts between March and November 2020, up from £42 billion in 2019.

We’re likely to see a similar trend in the coming months of social restrictions. While it’s definitely a good idea to have an emergency cash buffer, a current account is almost certainly one of the worst places to keep it.

Currently the typical interest rate on a current account is just 0.13%, and £220 billion sits in instant access accounts paying zero interest. Savers can’t do anything about the economic situation that has prompted such low interest rates, but they can take concrete steps to improve their own lot.

PAY DOWN CREDIT CARDS

Paying down expensive debt is one of the best investments you can make. The average interest charged on credit card balances is currently over 17% according to financial information company Moneyfacts, so by paying this off you are effectively getting a 17% guaranteed return, and that compares with getting 0.13% on average for money sitting in a current account.

You may even be able to get such a return without committing any cash, by transferring expensive credit card debt to a provider who is offering 0% on balance transfers. Make sure you factor in any fees charged for the balance transfer, or ongoing fees for the credit card.

PAY DOWN YOUR MORTGAGE

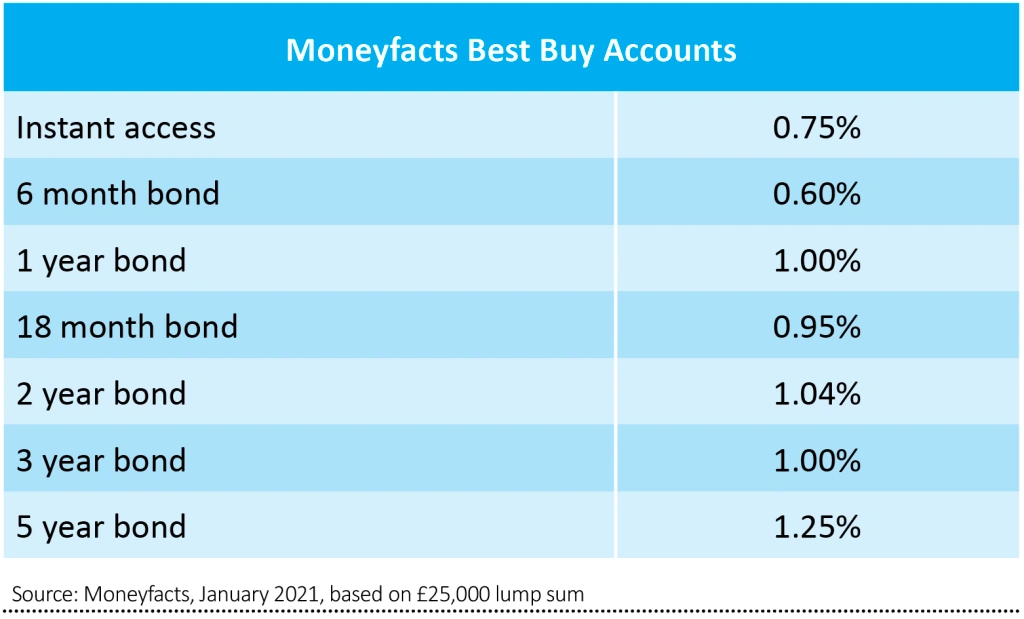

After you’ve paid off more expensive debt, it’s worth considering overpaying your mortgage. The average mortgage interest rate right now is 2.1%, which compares favourably to the best rate you can get on an instant access savings account, which Moneyfacts identifies as 0.75%.

There is a big but – many mortgages will only allow you to overpay a certain amount each year before you start to incur punitive charges, so you may find there is only a limited amount of cash you can funnel in this direction.

ACTIVELY MANAGE YOUR CASH

Shopping around for the best rate on your savings is always a good idea. You should also consider locking away your money for longer in a fixed term bond to harvest higher rates.

Normally the longer you lock your money away for, the higher the rate you will get. However, that picture is a little distorted at the moment because there are some expectations in the market that there will be an interest rate cut. Based on current rates, the best one year bond looks reasonable value, but there’s not a great deal of compensation for locking your money around for longer terms, though that can change.

Savers also now have access to savings account supermarkets, or cash hubs. These portals give you access to savings accounts from a number of banks, building societies and even investment platforms paying competitive rates of interest in one place, making it much easier to manage your cash holdings.

CONSIDER PREMIUM BONDS

While NS&I has slashed rates on many of its most popular accounts, premium bonds still look like a decent option, as the 1% interest rate on the prize pool remains higher than the best easy access account right now. On top of that it’s tax-free so anyone who’s used up their personal savings allowance would actually need to get an even higher rate from a standard taxable account to match the post-tax interest from premium bonds.

SET UP OR TOP UP AN ISA

Cash ISAs allow you to receive interest tax-free. However, for many people this might not be so different to a normal savings account, seeing as there is currently a personal savings allowance of £1,000 for basic rate taxpayers and £500 for higher rate taxpayers. With interest rates as low as they are, you would therefore need a lot held in cash to start to pay tax. Unless you are an additional rate taxpayer and therefore don’t get a personal savings allowance.

Rates on Cash ISAs also tend to be a bit lower than the best rates from other savings accounts. However, there are still some reasons to consider a Cash ISA. If in the future you decide you want to invest your money, Cash ISAs can be converted into Stocks and Shares ISAs without using any more of your ISA allowance.

Stocks and Shares ISAs are free from income tax and capital gains tax, though of course you must be willing to invest for the long term and be prepared to ride out the ups and downs of the stock market.

Annual dividends above £2,000 are taxable if not held in an ISA (or pension) and with the UK stock market tending to yield between 3% and 4%, it won’t take a huge portfolio to make the ISA shelter worthwhile, particularly if you factor in stock market growth. Gains are also free from capital gains tax, so if you have some big winners, you get to keep more of the profits.

TOP UP YOUR PENSION

Another option if you’re able to leave your money invested for the long term is to top up your pension. In the first instance, check if your employer will match any additional contributions you make. If they do, it will probably be on regular savings rather than lump sums, so you’ll need to ask to increase your monthly contributions. If your employer doesn’t match contributions and you want a wider investment choice than your workplace pension offers, a SIPP might be the way to go.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

First-time Investor

Great Ideas

- Alibaba faces baptism of fire at start of 2021

- IP Group still offers upside as it eyes further realisations

- Play a regional recovery with BlackRock Latin American

- Buy Sainsbury's now before the shares surge

- Gamma run could speed up if it can nick a bit of Twilio’s limelight

- Recent acquisition provides growth and security for Gresham House