Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGamma run could speed up if it can nick a bit of Twilio’s limelight

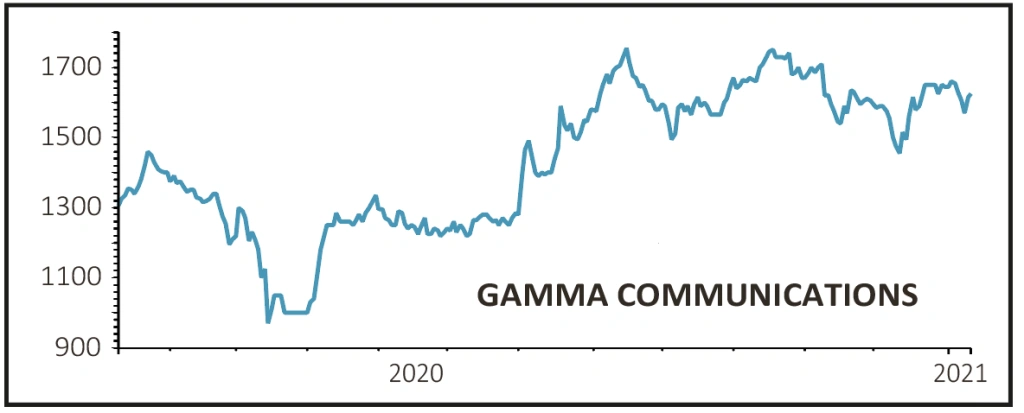

GAMMA COMMUNICATIONS (GAMA:AIM) £16.35

Gain to date: 9.4%

Original entry point: Buy at £14.95, 9 July 2020

Guiding investors towards sensible targets and then beating them is a very good habit for a stock to develop and it’s a box that Gamma Communications (GAMA:AIM) ticks.

The company recently revealed that earning for 2020 would be ‘slightly ahead’ of forecast with revenue at the top of the range.

The consensus range had been pitched at revenue of between £371.8 million to £396.7 million, adjusted EBITDA (earnings before interest,tax, depreciation and amortisation) of £73.9 million to £76 million.

The scale of the beat may be modest but as analysts at Megabuyte point out, organic revenue growth close to double-digits during this pandemic is ‘impressive’.

To remind readers, Gamma is a Unified Communications-as-a-Service (UCaaS) supplier, providing 21st Century cloud-based, integrated systems with access to the latest tools and apps. This is one of the few a growth areas in the otherwise mature telecoms space and is where US stock star Twilio has proved a real Covid winner. Its stock surged 250% in 2020 and now trades on a near-3,000 PE.

Maybe Gamma doesn’t deserve to be rated like that but it puts its own 12-month PE of 28.1 from a modest-looking 20% share price run into sharp relief.

SHARES SAYS: A quality business still worth buying for the long-run. [SF]

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

First-time Investor

Great Ideas

- Alibaba faces baptism of fire at start of 2021

- IP Group still offers upside as it eyes further realisations

- Play a regional recovery with BlackRock Latin American

- Buy Sainsbury's now before the shares surge

- Gamma run could speed up if it can nick a bit of Twilio’s limelight

- Recent acquisition provides growth and security for Gresham House