Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

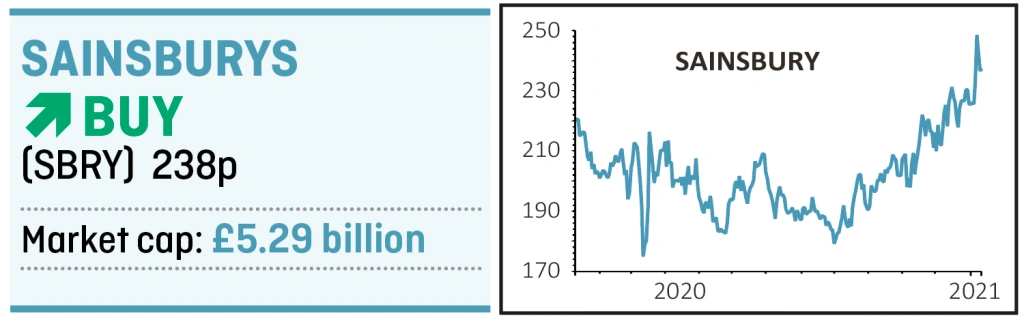

magazineBuy Sainsbury's now before the shares surge

Supermarket Sainsbury’s (SBRY) is starting to feel the benefits of the investments it has made into its business but its share price is still attractively valued, making now an opportune time to buy.

The firm released a trading update last week which has made investors and analysts sit up and take note, as it reported a record increase in sales over the Christmas period and raised its full year earnings guidance.

CRACKING CHRISTMAS

Revenue for the third quarter to 2 January was up 8.6% on a like-for-like basis excluding fuel, with sales over the nine-week Christmas period up 9.3% on a like-for-like basis.

Grocery sales for the quarter were 7.4% higher thanks in part to a 128% surge in online revenues, with its upmarket Taste the Difference range posting an 11% rise as customers treated themselves over Christmas.

Chief executive Simon Roberts said the supermarket’s customer satisfaction scores were at their highest level ever during the key Christmas week.

Significantly, online sales grew to 18% of grocery revenues during the quarter thanks to the company more than doubling its slots for home delivery and Click & Collect and increasing its productivity with more orders delivered per van.

The growth in online sales is a significant advancement year-on-year, and this route to market is now demonstrably profitable for the firm, something which hasn’t always been the case in the past and could help change investor sentiment towards Sainsburys and the supermarket sector.

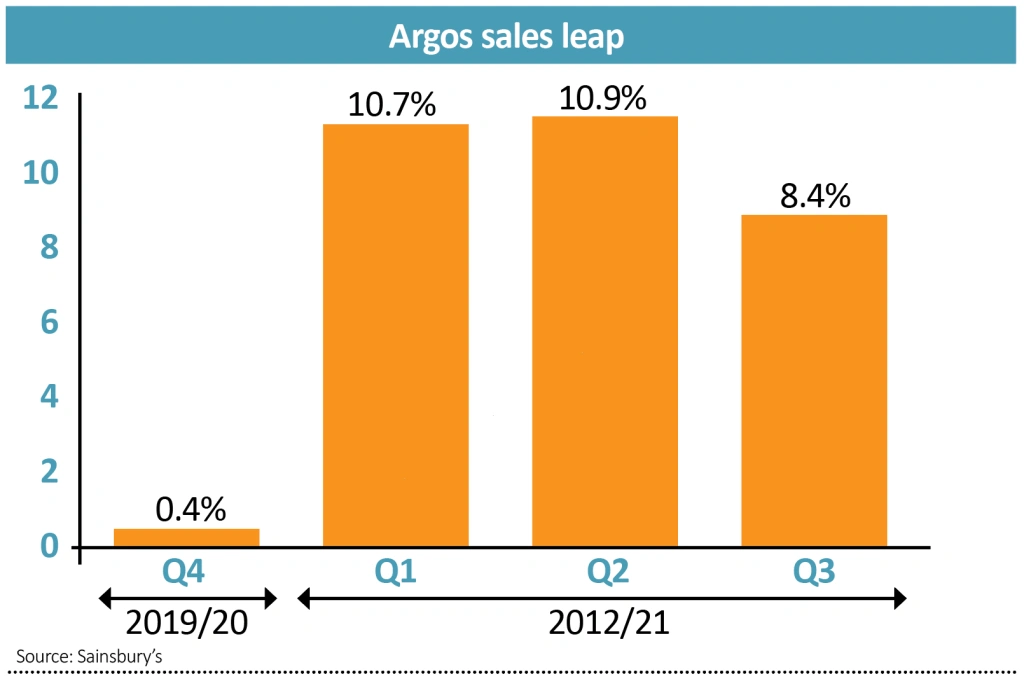

Pleasingly, sales of general merchandise were also robust, rising 6% during the quarter thanks to an 8.4% increase in sales at Argos, confirming our bullish call on the prospects for the non-food business in our November ‘Christmas winners’ feature.

After forgoing business rates relief of £410 million, the retailer now expects to report underlying pre-tax profits for the year to March of ‘at least £330 million’, compared with the company-compiled consensus of between £270 million and £285 million.

ARGOS DRIVING GROWTH

Argos, which has done a great job of sharpening its delivery service, looks to be a key growth driver for Sainsbury’s and a differentiator for the firm against peers like Tesco (TSCO) and Wm Morrisons (MRW).

Its decision to close 420 standalone Argos stores might have given the impression Sainsbury’s failed with its £1.4 billion acquisition of the catalogue retailer in 2016, but that couldn’t be further from the truth, with the latest update again confirming the division’s, (and the group’s) prospects. Sainsbury’s says 90% of Argos orders are now made online versus 55% four years ago, representing a major shift in customer behaviour.

The supermarket’s strong trading update comes after it booked £438 million in one-off costs in the 28 weeks to 19 September as it closed the Argos stores, and invested in its online capability as well as its Nectar and Habitat brands and Sainsbury’s Bank, which has returned to profitability in the quarter just gone after reporting first-half losses.

That investment looks like it is starting to pay off with the supermarket now in a better place to capture upside from the shift to online.

Despite the clear progress made the company is still on a very attractive valuation. According to Stockopedia its trades on a 12-month forecast rolling price-to-earnings ratio of 12.7 times, and a price-to-book value of 0.75 times.

The Sainsbury’s share price has admittedly gone nowhere in the past decade, and the supermarket has been one of the most shorted stocks over the last year.

RISKS TO WEIGH

There are still risks to keep in mind and the supermarket itself has warned the impact of the pandemic on sales and costs adds additional uncertainty to its outlook for the remainder of its financial year to March 2021.

However, Shore Capital analyst Clive Black believes investors should change their view on the stock and that the short sellers should think again.

Following its latest trading update the broker Black argued its shares are materially undervalued with scope for a ‘rating expansion’. He thinks the shares could reach 320p.

Black explains: ‘Sales comparatives will be very challenging [next year], but working from home is here to stay, Sainsbury’s has a firmer market share base than it would have expected a year ago, a much more profitable online capability, volume boosted working capital and with capital discipline, noting the step up for two years to £750 million to reshape Argos, so the scope to deliver strong free cash flow.’

He says that free cash flow can de-lever the business and fund the group’s attractive dividend with a yield in excess of 5%, while like the rest of its sector, Sainsbury’s faces favourable cost comparatives in its 2022 financial year. [YF]

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

First-time Investor

Great Ideas

- Alibaba faces baptism of fire at start of 2021

- IP Group still offers upside as it eyes further realisations

- Play a regional recovery with BlackRock Latin American

- Buy Sainsbury's now before the shares surge

- Gamma run could speed up if it can nick a bit of Twilio’s limelight

- Recent acquisition provides growth and security for Gresham House