Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow Future bounced back to join the FTSE 250

Magazines as a format emerged to serve people’s interests and hobbies, and they have developed over time to cover everything from politics and gardening to photography.

The industry has gone through significant change in recent years because of people’s increasing reluctance to hand over hard-earned cash for a glossy print product. In 2018 figures from ABC showed sales and advertising for the top 100 UK magazines had more than halved since 2000.

Interestingly, the recent success of media group Future (FUTR) – newly promoted to the FTSE 250 index – has been built on recognising that people still want to read about their hobbies.

The company has a portfolio of more than 100 titles, including Techradar and Total Film. It was founded with just a single publication, Amstrad Action, in Somerset back in 1985.

Future has maintained a bias towards technology, and after a late 1990s stock market flotation it enjoyed spectacular gains amid the dotcom bubble. When the bubble burst the fall from grace was just as spectacular. Its recent resurgence is therefore all the more interesting.

RIDING THE CREST OF A WAVE

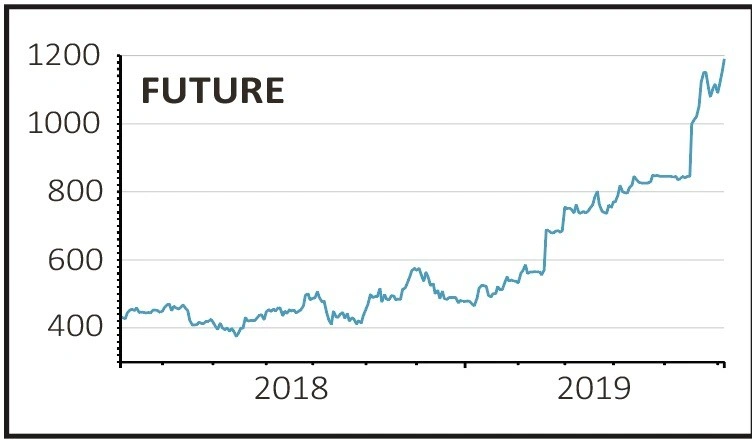

The shares are back riding the crest of a wave, three years ago valued at around £30m and today close to £1bn. Even as recently as December 2017, when Shares selected the stock as one of its top picks for 2018, it had a market cap of less than £200m.

The recent transformation of the group has been led by Zillah Byng-Thorne who joined as chief executive in 2014. She had experience of bringing an old media product into the digital age as finance chief at second-hand car marketplace Auto Trader (AUTO).

Since 2015 her own chief financial officer has been fellow Auto Trader alumni, Penny Ladkin-Brand. The pair have pursued a growth strategy driven by acquisitions.

The company has a platform which enables it to monetise specialist content and brands through a mixture of e-commerce, getting content users to click through to partnered retailers, events and online advertising. The plan is to feed newly-acquired assets into this platform.

Future’s in-house technology allows it to re-use its content in various formats, in different parts of the world and in different languages.

BIG US DEAL

The largest deal completed by Future under Byng-Thorne was the $135.2m capture of US-based publisher Purch in 2018.

Purch, which has several tech-focused properties, helped build a leading position for the company in US technology media.

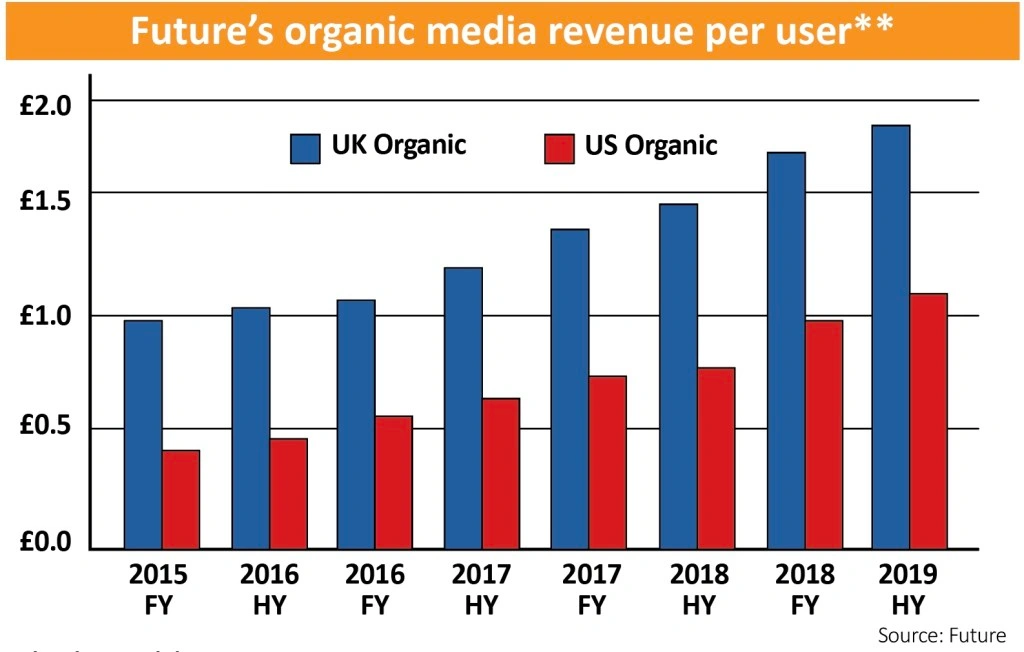

Expansion in the States was, and is, a key strategic priority for the group. This seems logical given it already had a large US audience but derived only a relatively modest proportion of its revenue from across the pond. The company still makes considerably more money out of its readers in the UK than those in the US.

The transaction was funded by a £105.7m rights issue at a 30% discount to the market value at the time. Frequent acquisitions can be a red flag for some investors but, so far at least, the company has done a good job of proving it can integrate businesses into its model.

Recent results for the first six months of its financial year (which runs until 30 September 2019) illustrated the journey the business has been on with adjusted earnings before interest, tax, depreciation and amortisation (EBITDA) up 169% to £23.7m. Year-on-year free cash flow was up from £10.1m to £27.5m.

What is Future’s structure?

Future is split into two divisions – Media and Magazine. The fast-growing Media

division has three revenue streams: e-commerce, display advertising and events. Currently this mix is dominated by display ads but e-commerce is growing rapidly.

The Magazine division derives revenue from news trade, subscriptions and advertising.

NOT RESTING ON ITS LAURELS

Byng-Thorne tells Shares that she is looking at new areas including podcasting but will only pursue these avenues if it makes commercial sense to do so.

She adds the expertise of writers on its own digital media titles can help it keep on top of trends in a fluid and rapidly shifting industry landscape.

Byng-Thorne is also confident the company has the balance sheet to fund further M&A, particularly as the increase in the share price means the company can offer stock as well as cash to potential targets. As at 31 March the company was on a net debt-to-EBITDA ratio of 1.1 times.

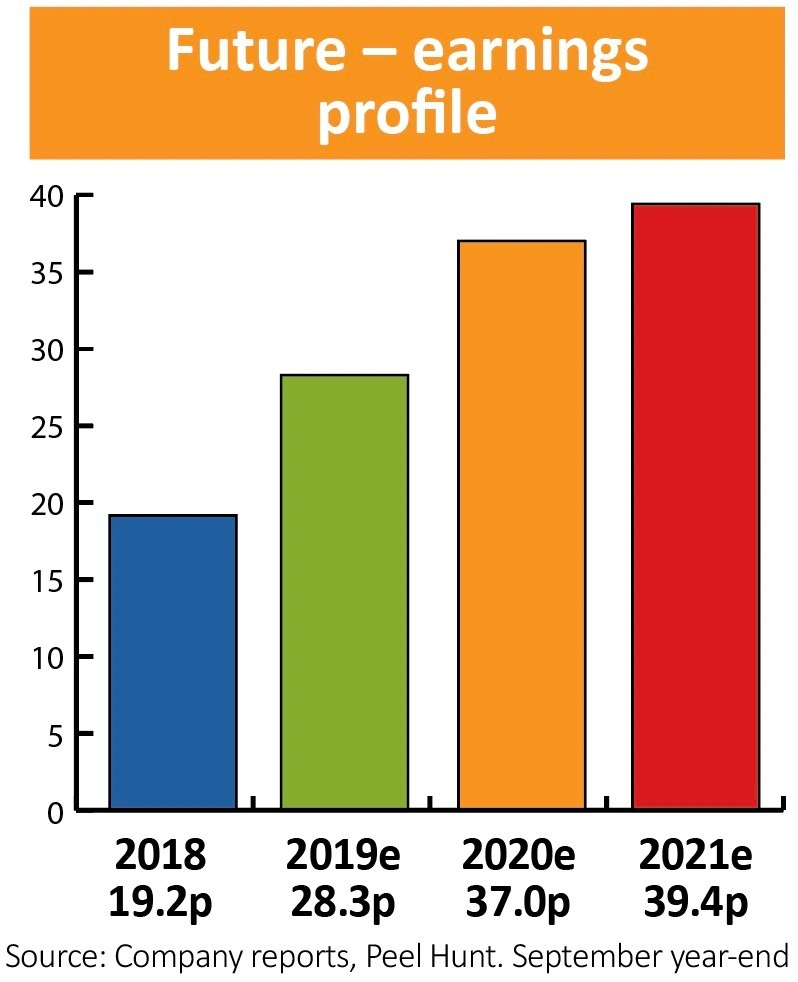

SHARES SAYS: We are big fans of Future, but the valuation looks up with events for now. At £11.48 the shares trade on 31 times forecast earnings for the year ending September 2020. This is a great business but given an uncertain backdrop in the wider market we think there may be opportunities to buy at a lower price in the future. Wait patiently for a better entry point.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.