Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat is the future of Woodford Patient Capital Trust?

Following the suspension of LF Woodford Equity Income (BLRZQ73), the big question for a lot of retail investors is what’s going happen to Woodford Patient Capital Trust (WPCT)?

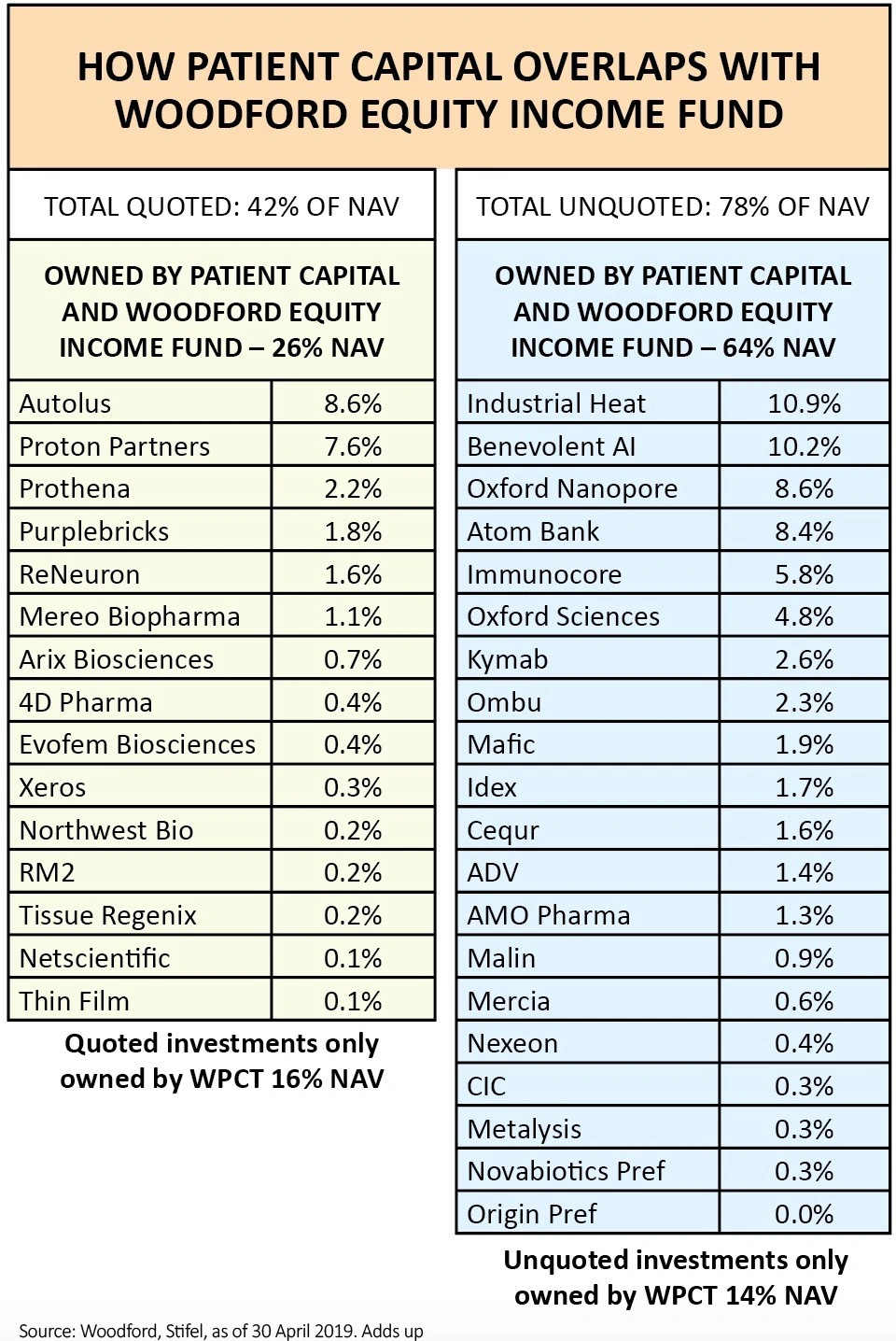

Equity Income and Patient Capital have a big overlap in holdings, so what happens in one fund can have a big impact on what happens in the other.

Kieran Drake, a research analyst at Winterflood, estimates that 74% of Patient Capital’s portfolio by value at the end of April was also held in the Equity Income fund.

He believes that as Woodford restructures the Equity Income fund portfolio and exits all the illiquid holdings, valuations in the Patient Capital portfolio could fall and hurt its net asset value (NAV). We’ve already seen the market start to price in this scenario, as reflected by a sharp decline in its share price.

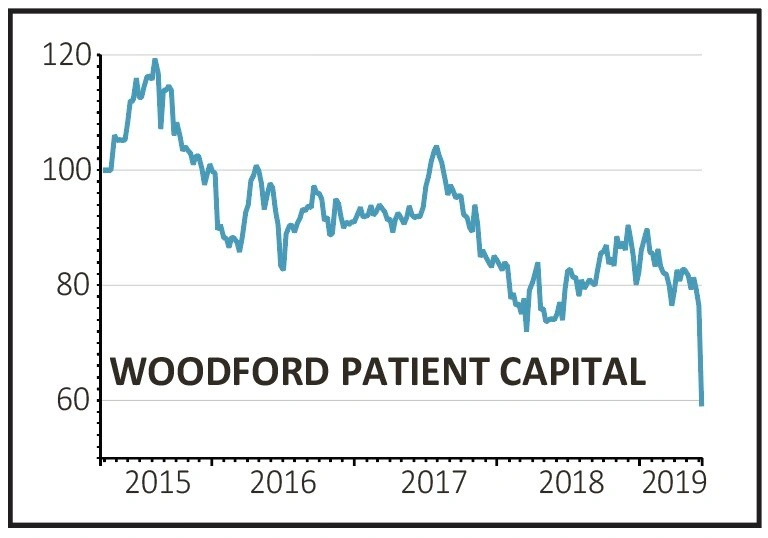

The stock fell from 90p in January to an all-time low of 58.2p on 11 June. At the time of writing it had recovered slightly to 62.79p.

In addition, Drake thinks negative sentiment surrounding suspension of dealing in the income fund could cause Patient Capital’s discount to NAV to widen, which would be exacerbated if the income fund became a seller of its Patient Capital shares (it owns 9% of the investment trust).

He says: ‘While many of Patient Capital’s portfolio companies are making good operational progress and there are several potential catalysts expected later this year, in our view the situation at the Equity Income fund poses a potentially significant headwind.

‘This may also impact the manager’s ability to continue to support the portfolio’s early stage businesses.’

In addition to the share price going down, if you hold Patient Capital you may have to begin paying for it now. The investment trust is unusual in that it currently doesn’t charge a management fee, so the manager only gets paid if it hits a certain level of performance, which it has failed to do since launch.

Analysts at Stifel believe if fees from Woodford’s other funds continue to decline due to more people asking for their money back, this could result in it being necessary for the Woodford asset management business to start charging a management fee on Patient Capital to make it viable.

Three potential scenarios for Patient Capital

Stifel has identified three potential events which could affect the investment trust and its shareholders:

1 The Equity Income fund offers to put investors into two categories – those who want to continue with the fund, and those who want to get out.

For those in the latter category, the fund’s listed investments would be sold quickly and the cash returned to investors. This would then give time for the unquoted investments to be sold gradually.

In this case Patient Capital, Stifel hopes, would benefit from being able to write up the value of some of these investments and sell to third parties at above current market valuations, boosting returns for Patient Capital holders. But this isn’t certain and it could still have to sell at a loss.

2 Investors who hold Equity Income ask for that fund to be wound up with cash returned to investors, which could have a knock-on impact on Patient Capital and its total returns due to having some portfolio cross-over.

This would potentially take quite a long time given the lower liquidity of a lot of the fund’s holdings, and Stifel says Patient Capital would be impacted by the valuations of the unquoted stocks in Equity Income when Woodford sells them, given a lot of them are also held in Patient Capital.

3 Woodford Investment Management resigns as manager of both the income fund and Patient Capital, or the board of Patient Capital think a new manager is needed to either continue managing the portfolio or run it off and return cash to investors.

In the latter case, Patient Capital would then only exist so that all its holdings can be sold off in order to return cash to investors.

But Stifel adds that one danger of a new manager taking over the portfolio would be that they could look to ‘kitchen-sink’ the valuation of the unlisted portfolio when they take on the management contract.

This essentially means they’ll sell the unlisted stocks for a cheap price, which would damage the trust’s share price and shareholder return but then make it a lot easier to grow the share price and total return the following year, given the low comparative. It would be in the manager’s interest to do this as they get paid for a certain level of growth compared to the previous year.

COULD IT BE TAKEN OVER?

JPMorgan Cazenove has gone one step further and thinks Patient Capital could become a takeover target for ‘predators’ given its plunging share price.

Investment trust analyst Christopher Brown says this could be plausible given the damage to Woodford’s reputation, the fact the trust is trading at a big discount to NAV, and that Patient Capital currently doesn’t charge a management fee.

Theoretically there would be an opportunity for a company to make money by taking over the trust, especially if they managed to narrow the discount to NAV and turn around its fortunes.

However, the takeover options appears to be an outlier view and is generally considered an unlikely option.

WHAT SHOULD PATIENT CAPITAL SHAREHOLDERS DO NEXT?

While there are clear headwinds which could depress Patient Capital in the near term, selling now while sentiment is very weak could be the wrong thing to do, particularly as the shares have already priced in a lot of potential bad news.

Go back to the reasons why you bought the investment trust in the first place. Hopefully it was to get exposure to a portfolio of companies with good prospects, some of which could be big winners in the future, albeit ‘patience’ is needed as these companies go through their development stage.

Nothing has changed in terms of Patient Capital’s strategy. However, Neil Woodford’s reputation has been damaged by the latest debacle, which means the investment trust could trade at a wide discount for some time as the market questions his skills.

Shareholders will need to decide themselves whether to cut their losses now or hang in and wait to see if the situation can be fixed. In particular, it is worth noting that many private equity funds are awash with cash and may be interested in picking up some of Woodford’s illiquid investments.

If you are no longer patient then get out and move on. But if you originally bought the trust as a five to 10-year holding then further patience could pay off, albeit nothing is guaranteed.

What might the new version of Woodford Equity Income fund look like?

Fund manager Neil Woodford has said he is looking to reposition the portfolio of Woodford Equity Income Fund and get rid of its illiquid holdings.

This means the fund is likely to predominantly contain bigger companies, so it could end up looking a lot like Woodford’s other open-ended fund, LF Woodford Income Focus (BD9X6D5).

There is therefore a possibility that the funds could merge, given the likelihood of a significant overlap in holdings.

Ryan Hughes, head of active portfolios at AJ Bell, says: ‘It is certainly possible that the funds could merge particularly as it looks as if Woodford is repositioning Equity Income into large cap stocks.

‘Any merger will need regulatory and investor approval and therefore would take some time but is it certainly an option that may be explored at a later date.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.