Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAll you need to know about open-ended funds

Choosing the funds in which to invest your hard-earned cash is an important yet complex decision.

Not only do investors have to choose between funds investing in different geographies, sectors and asset classes, they also have to weigh up the pros and cons of funds that are structured differently too.

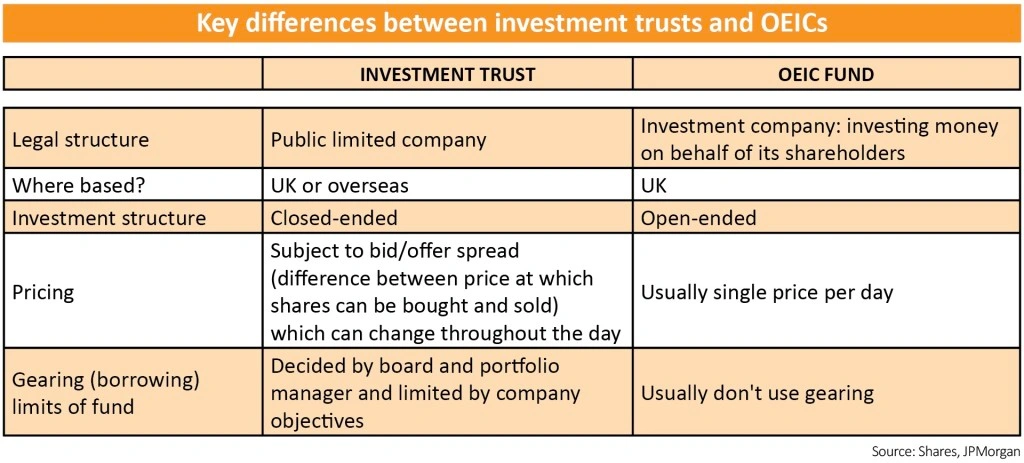

Among the two most commonly debated are closed-ended and open-ended funds, by which we mean investment trusts and unit trusts/open-ended investment companies (Oeics) respectively.

Arguably the UK’s best-known open-ended fund has hit the headlines for all the wrong reasons. Following months of investors cashing out of star manager Neil Woodford’s largest fund (known as redemptions), dealing in LF Woodford Equity Income Fund (BLRZQ73) was suspended on 3 June meaning investors are temporarily unable to sell.

The struggling fund has been ‘gated’ to protect investors and provide Woodford with the time to reorient the portfolio to hold more liquid investments.

Following the major property funds that suspended pricing and redemptions after the Brexit vote in 2016 in order to avoid having to conduct a fire-sale of their assets, the suspension of Woodford’s fund has reopened a debate on the open-ended fund structure and whether it is suitable for holding illiquid assets such as property or unquoted companies.

Before you can discuss the suitability of certain types of holdings in different types of funds you first need to understand the basics of how open-ended funds work. Read on.

WHAT DO YOU MEAN BY ‘OPEN-ENDED’?

Open-ended funds are a type of collective investment scheme that enable you to cost-effectively build a diversified portfolio of investments.

They are the most popular types of collective in the UK and consist of unit trusts and OEICs. The great advantages of open-ended funds are their flexibility to make more units, as well as the fact there are far more funds available than in the investment trusts sector, giving investors greater choice.

Open-ended funds allow you to pool your money with other investors so that you can invest more cost-effectively in many different equities and bonds than if you were to buy each security separately.

The term ‘open-ended’ simply means more shares or units can be issued each time someone invests, which (usually) means you can always buy or sell whenever you want.

These UK-domiciled funds offer a wide range of choice by region, sector or type of investment such as equity, bond or property.

SOME OF THE BENEFITS

Arguably, the open-ended structure is beneficial as it is often cheaper and easier for investors to buy and sell.

As the manager can create an infinite amount of units, investors are able to get in and out of a fund without restriction. At the same time, open-ended funds trade at the net asset value (NAV) of their underlying portfolios rather than at a discount or premium, which is overwhelmingly the case with publicly traded investment trusts, whose shares are subject to the vagaries of supply and demand.

But, as the Woodford Equity Income debacle demonstrates, when there isn’t liquidity an open-ended fund has to suspend buying and selling. These funds have no maturity date and can grow larger or smaller depending on the number of investors wishing to buy or sell their shares or units, which can rise and fall in number.

THE IMPORTANT STUFF ON UNIT TRUSTS

While operating in broadly the same way, there are a few key differences between OEICs and unit trusts.

With unit trusts, the fund is split into units and these are what you purchase as the investor. The portfolio manager creates units for new investors and cancels units for those selling out of the fund.

Since the creation of units can be unlimited, a unit trust is referred to as ‘open-ended’. And the price of each unit depends on the NAV of the portfolio’s underlying investments and is priced once per day. The value of the units you buy directly reflects the underlying value of the investment.

When you put money into a unit trust, you receive units and are referred to as a unit-holder, whereas OEIC investors receive shares and are called shareholders. Another key difference is that unit trusts have an offer and a bid price, whereas OEICs have a single price and a ‘cleaner’ or simpler pricing structure.

WHAT IS AN OEIC?

Most new funds launched today are established under the OEIC structure, whose simpler pricing structure is the reason they’ve been described as a ‘what you see is what you get product’, since its share price equals the value of all the assets held divided by the number of shares in issue.

OEICs are structurally different to their more established unit trust counterparts too; as limited liability companies rather than trusts.

OEICs operate in a similar way to unit trusts, except that the fund is actually run as a company, quotes a single price rather than a bid and offer price and is governed by company law rather than trust law.

And whereas a unit trust entitles an investor to participate in a fund without actually owning its assets, OEIC investors actually hold shares in the company.

Unlike unit trusts, an OEIC can act as an umbrella scheme holding various sub-funds, each with their own investment goals.

For investors, the advantage here is that you can invest for income and growth in the same umbrella fund, shifting money from one sub fund to another as priorities change. Some OEIC providers allow you to move your money without charge, since you are staying within the same share class and charging structure.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.