Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

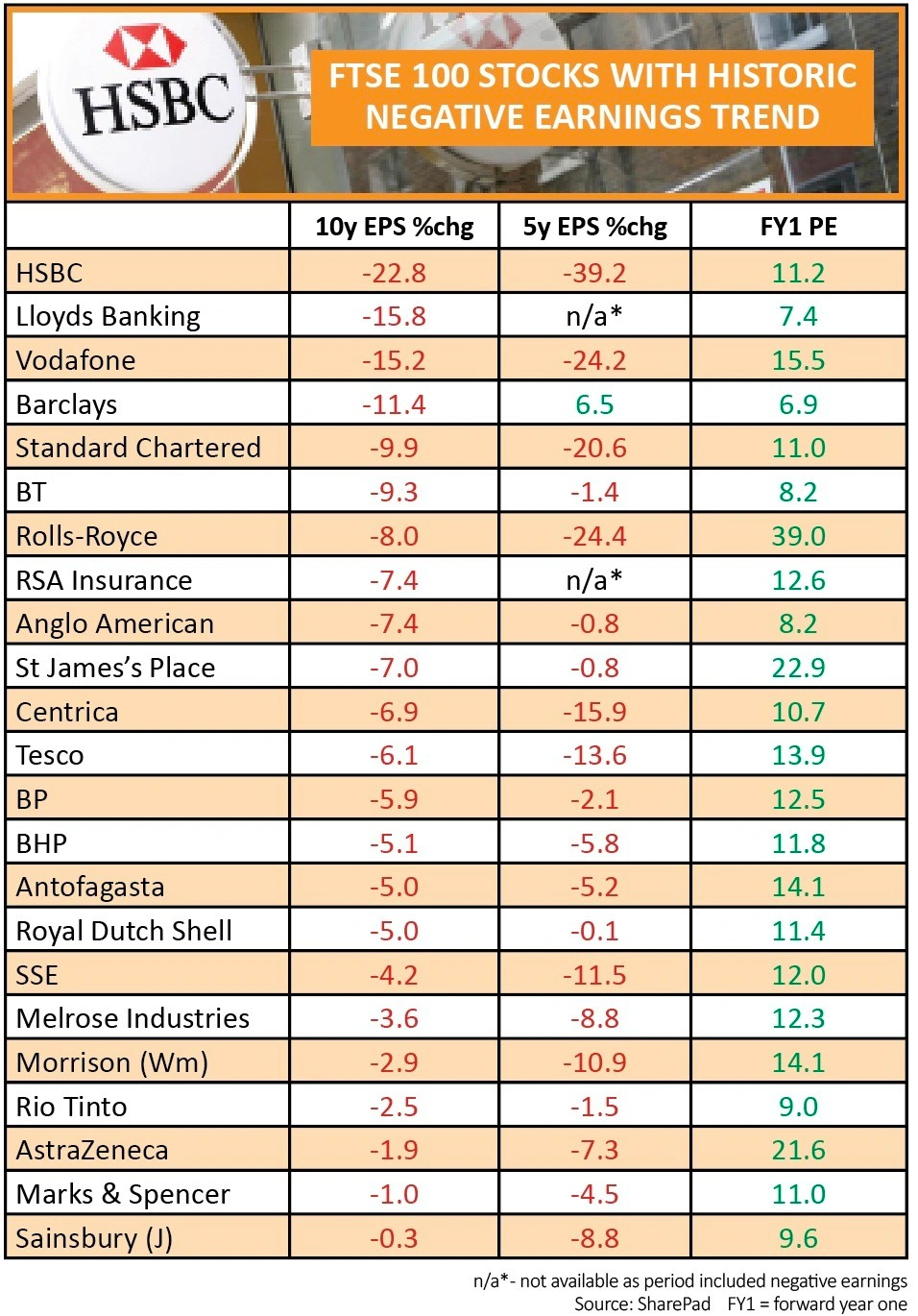

magazineFTSE 100 stocks with a negative earnings trend

Last week we looked at which stocks in the FTSE 100 index had the fastest earnings growth over five and 10 years and what price investors were prepared to pay for them.

This week we’ve delved into the murky waters of the stocks with the worst record of growing earnings. We have used the same metrics, looking at five and 10 years of data, supplied by SharePad.

Again, the question boils down to what should you pay for a stock given its past (and implied future) earnings growth?

LOW DOWN AND DIRTY

The average rate of earnings growth across both five and 10-year periods in our screening is roughly 10%, the average 12-month forward rating is 15.5-times and the average discount to the 10-year share price peak is 23%.

Again these are mean or average values, not market capitalisation-weighted like the indices, but they are still useful for context.

We found negative earnings growth concentrated in a few sectors, principally basic materials (essentially mining), consumer discretionary, financials and what we would call utilities. There were also a couple of energy stocks, a couple of industrials and even a healthcare stock.

This group of miscreants has managed to destroy earnings by between 7% and 9% per year on average over the last five and 10-year periods, and trades at an average discount to its 10-year high of 38% which sounds fair.

Strangely though, the average forward earnings multiple for these stocks is 14.3-times which is not that different to the market average. Even stranger, for some stocks which consistently destroy earnings, we are actually paying a hefty premium.

NAMING AND SHAMING

The biggest stock in our sample by market value, and surprisingly the stock with the worst record bar none of destroying earnings over the past five and 10 years, is mega-bank HSBC (HSBA).

We’ve said on several occasions in the past that you should avoid investing in HSBC yet it still trades on the highest forward multiple of any high street bank and the smallest discount to its 10-year price high (11.2-times and 18%). Clearly investors see something in its future which we don’t.

The other bank to find itself in the ‘sin bin’ is Standard Chartered (STAN), which like HSBC has a large Asian business and has somehow managed to destroy earnings at almost a double-digit rate every year for the past decade while still commanding a multiple of 11-times.

As way of comparison, former bad boy Barclays (BARC) has actually grown its earnings by 6% a year over the last five years so it doesn’t feature on our list. Despite this, investors still won’t pay more than 7 times earnings for its shares which seems perverse in this context.

The other financial stock on the list is St James’s Place (STJ) which trades on a whopping 23-times despite having shrunk its earnings by an average of 7% a year over the past decade.

INDEX HEAVYWEIGHTS GALORE

The big oil pairing of BP (BP.) and Royal Dutch Shell (RDSB) both feature thanks to volatile commodity prices.

Yet both have seen an improvement in their earnings generation over the last five years (i.e. earnings have shrunk, just at a slower rate) and both trade at a discount to the group and the market average on forward multiples.

The miners are also well represented thanks to the period including a long spell for metal and mineral prices falling from the previous bull-run which ended circa 2012.

Anglo American (AAL), Antofagasta (ANTO), BHP (BHP) and Rio Tinto (RIO) are all on the list, as are what we’ve have collectively called utilities such as BT (BT.A), Centrica (CNA), SSE (SSE) and Vodafone (VOD).

Another big name which we were surprised to see on the list is £80bn healthcare giant AstraZeneca (AZN). Despite shrinking profits over both periods, with a worsening trend over the past five years, the stock still trades on over 20 times earnings and is less than 10% below its 10-year high. This may be down to a resurgence in earnings growth in the past year and a stronger outlook for earnings.

In comparison, rival GlaxoSmithKline (GSK) has grown its earnings consistently over five and 10 years, trades on less than 14-times and is 12% below its 10-year high.

ON YOUR MARKS, GET SET, GO

The last cluster of stocks in our screening is supermarkets, which is less surprising given the brutal turf war being waged by the discounters and the continued investment in prices needed to keep market share.

Sainsbury (SBRY), Tesco (TSCO) and WM Morrison (MRW) have seen their earnings fall in both periods but at an accelerating pace over the last five years.

While some would argue otherwise, we would put Marks & Spencer (MKS) in the same camp as its earnings growth – or lack thereof – and its lowly rating is more reminiscent of a grocery business than a fashion retailer.

Which begs the question, if the market treats M&S like a grocer, maybe the company should sell off its clothing business, return cash to shareholders and focus on food?

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.