Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSeeking uncorrelated returns via a trust trading on a big discount

Managed by James de Bunsen and Peter Webster, the primary focus of Henderson Alternative Strategies Trust (HAST) is to give private investors access to strategies and asset classes that are either not available to retail or are closed to further investment.

The investment trust can invest in private equity, hedge funds, credit funds, property and other alternatives which have the potential for uncorrelated returns and provide above-normal returns by exploiting underpenetrated markets.

Its benchmark is the FTSE World Total Return Index, but it is also a constituent of the AIC’s Flexible Investment sector. Co-fund manager James de Bunsen targets an informal benchmark of returning at least 8% per year over the medium term.

He hopes the investment trust will behave more defensively than some of his peers, while capturing a part of any upside in rising markets.

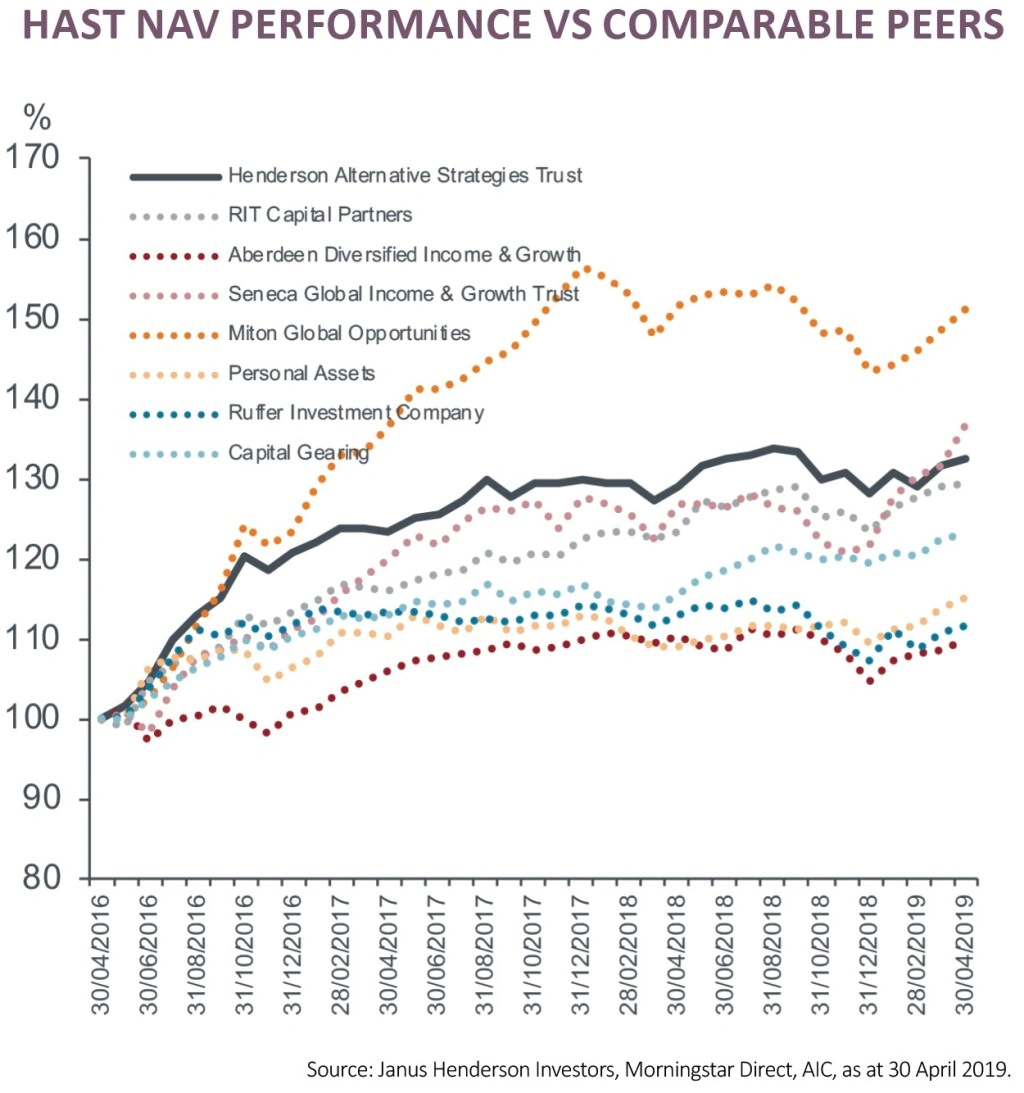

The last three years’ performance seems to be demonstrating the desired profile, with HAST having delivering the third highest return compared with peers, with the second lowest volatility.

TRADING AT A DISCOUNT

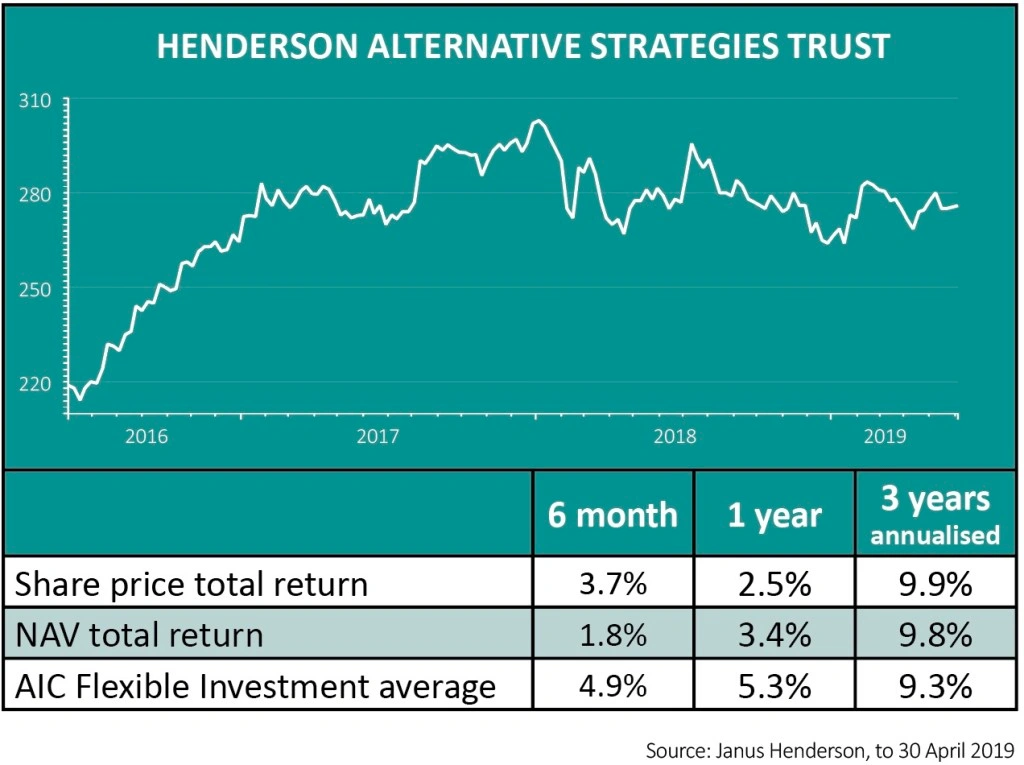

Despite the good relative performance and low volatility, HAST is on the biggest discount to net asset among investment trusts in the AIC Flexible Investment sector (19.9%). Perhaps one reason can be found by looking at the history of the fund before Janus Henderson took over the management.

The investment trust had a poor track record before Janus Henderson took over the reins. This may explain why the price is trading 38% below the peak levels in 2008, and should be born in mind when looking at the long term price trend. The previous manager had invested in very illiquid assets, and it has taken a few years to reshape the structure of the portfolio.

De Bunsen believes the fund is now structured appropriately, although there is approximately 10.9% of ‘legacy’ investments, half of which are listed, but are generally illiquid. However, collectively the managers believe this part of the portfolio will be accretive to net asset value.

INVESTMENT PROCESS

The team starts with a top-down analysis of the global economy in an attempt to unearth the opportunities and risks. When it comes to assessing the macro environment, the team can draw upon the depth of experience of the multi-asset team at Janus Henderson, which manages $6bn of assets.

The idea is to identify core holdings, which, in aggregate will provide a well-diversified pool of growth. It consists of quality assets that are well managed with the intention not to trade in or out of them, but hold on to them for the medium term.

Then there is a tactical part of the portfolio which takes a shorter term outlook. The team looks opportunistically for assets or products that look mispriced or misunderstood. They may even on occasion invest in single listed securities.

New holdings so far in 2019 include iShares World Energy ETF. The rationale here being that the recent fall in the price of oil has created an opportunity to buy a basket of the biggest oil companies on the cheap.

The fund has also invested this year in Deutsche Wohnen, a developer of German residential property in Berlin. There is a fundamental supply/demand mismatch in Berlin where asking rents are €10.34 compared with €6.93 for existing rents, measured in per square metre per month. However, shares in Deutsche Wohnen fell by 7.7% on 6 June amid chatter that authorities in Berlin were planning to impose a cap on rents.

RISK MANAGEMENT

Private equity tends to be the riskiest asset class in the investment trust’s portfolio, so the fund managers can effectively ‘dial-up or dial-down’ risk by adjusting exposures to the private equity component.

Private equity tends to be the most rewarding asset class to own in bull markets, but can detract from performance markedly in bear markets.

The team actively manages the fund’s holdings and if an investment doesn’t perform as expected, they will engage with the managers and try to get an understanding of what is driving the underperformance. If they judge the issues to be specific to the manager, rather than affecting the sector, they will sell their holding.

CAUTIOUS OUTLOOK

The team’s current top-down view is that there are many hidden risks in the global economy and that valuations are stretched in many areas of global markets. Therefore they are positioning the fund defensively by taking profits on certain areas and recycling the proceeds to increase exposure to high conviction positions.

De Bunsen sees lower returns and greater volatility in the future as high valuations are impacted by the withdrawal of central bank liquidity.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.