Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTaking the temperature of the market

It’s not easy to be an investor in the summer of 2019. The market continues to swing from one extreme to another and the headlines are dominated by geopolitical turmoil, trade wars and worries over global growth.

Fortunately, Shares is on hand to cut through the noise and look at some of the key developments in the markets and what they are telling us, while also considering the most significant political and economic factors.

WHAT’S BEEN GOING ON?

After a big stock market sell-off in the last three months of 2018, the New Year seemed to herald a change in fortunes. That was until US president Donald Trump intervened with renewed escalation of trade tensions with China and put the Dow Jones Industrial Average on course for its worst May for years.

June started in similar fashion before hints of rate cuts in the US and Eurozone helped shift global stocks back on to the front foot.

The deteriorating relationship between the US and China is just one of several factors the market is having to contend with, along with fluctuating interest rate expectations, volatile commodity prices as well as Brexit. Many of these issues are inter-connected and investors would be wise to take time to understand them.

WHAT CAN INVESTORS DO?

It is important to keep on top of all this activity. However confident you are in your own investments, you should not blind yourself to what is happening in the wider market.

And if you want to make use of your investment pot in the near future then you might need to consider reducing your exposure to shares.

Should we be headed for a period of more pronounced market turbulence then having some cash on hand to take advantage of market opportunities as they arise could be a logical approach.

However, an investor with a long-term horizon needs to think carefully before acting. Rather than seeking to time the markets, staying invested through the ups and downs helps you avoid crystallising a loss at the bottom and could see you benefit as your investments recover.

It is always sensible to review your portfolio regularly and now could be a good time. If any of your holdings look particularly exposed to some of the factors discussed in this article, or if there’s anything more speculative or something you’re less than sure about, now could be the time to switch into different investments which provide necessary diversification.

WHAT ARE EQUITY MARKETS SIGNALlING TO INVESTORS?

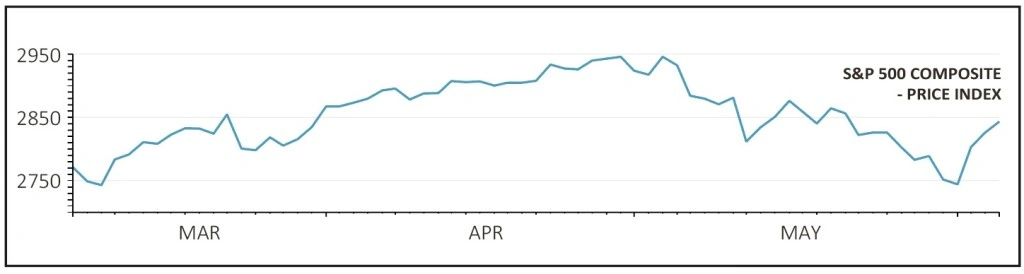

Since 30 April this year, the main equity markets around the world have fallen from anywhere between 2% and 9%, while US 10-year bond prices have rallied by around 3%, as their yields have fallen. Equity, or equities, is another word for stocks and shares.

Defensive sectors such as healthcare, beverages and leisure are holding up best with gains of 2% to 6% while economically sensitive sectors like industrials and autos have seen the brunt of the damage, down 10% to 13%. Often seen as an asset with safe-haven qualities, gold has risen during the recent market turbulence.

This all points to markets pricing in fears over flagging global growth, exacerbated by the increasingly fractious US-China trade negotiations. This was given extra impetus on 10 June when Donald Trump tweeted that he would place tariffs on Mexico until it stopped illegal migrants crossing the border into the US. He has since backed down.

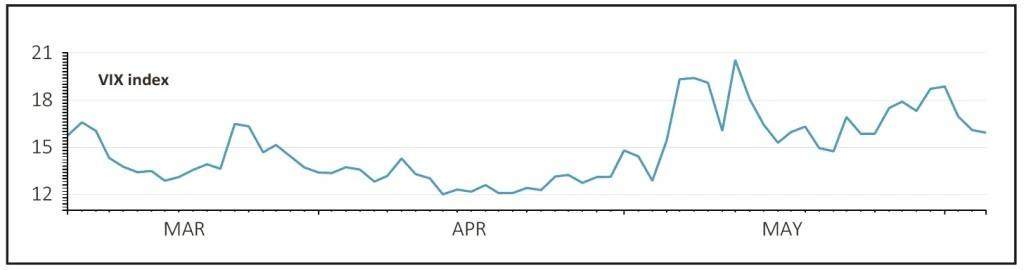

A knock-on effect has seen equity market volatility on the rise, with the VIX ‘fear gauge’ up from a reading of 12 in mid-April to 20.55 in mid-May and 16.14 on 10 June.

The index was nearly twice the latter level at the end of 2018 when investors were particularly nervous going into the New Year. It suggests that despite the move down in global equities, investors are not yet in panic mood.

FED U-TURN

Federal Reserve chairman Jay Powell surprised markets in January after opening up the possibility of interest rate cuts, despite six weeks earlier indicating that at least two rate rises were on the agenda for 2019.

Financial futures markets have quickly moved to price in a response to Powell’s comments.

Investors currently seem convinced the Fed will continue to prop up the equity market through accommodative policies. However, several experts including investment bank Goldman Sachs believe the markets are being too hopeful about a succession of rate cuts in the US.

WHAT ARE GLOBAL BOND MARKETS TRYING TO TELL US?

The past six months have seen a remarkable change in expectations for US interest rates. In January the chances of a 0.25% rise in the Federal Reserve’s discount rate this year was put at 90%. Today the chances of a 0.25% cut at the next meeting of Fed governors in July are put at almost 70%.

Towards the end of last year there were concerns that the US economy was over-heating thanks to the growth stoked in part by Trump’s generous tax cuts for US firms.

Fast forward and Trump’s tariffs are now prompting fears of a global recession. As well as imposing levies on Chinese goods, the president has threatened to punish Mexico, one of America’s biggest trading partners, and has stripped India of its ‘developing country’ status thereby exposing it to tariffs on billions of dollars of exports.

WHAT’S ALL THIS ABOUT INVERTED CURVES AND NEGATIVE YIELDS?

Fearing a global contraction, bond investors have rushed back to the safety of government bonds pushing US 10-year Treasury yields close to two-year lows below 2.10%. This has forced long-term rates below short-term rates, creating what is known as an ‘inverted yield curve’.

Typically, longer-dated bonds trade at a higher yield than shorter-dated ones to compensate for the higher risk of inflation over long holding periods, and an inverted yield curve has preceded every US recession of the last 60 years.

ARE INTEREST RATE CUTS GOOD OR BAD FOR STOCKS AND BONDS?

Interest rates cuts have historically been good for equities. A decrease in the cost of borrowing can help companies and it also encourages them to invest in their business. This can increase their earnings potential which is positive for share prices.

Bonds can also benefit from lower interest rates as when new bonds with lower yields than older fixed-income securities are issued in the market, investors are less likely to purchase new issues. Hence, the older bonds that have higher yields tend to increase in price.

At the moment it seems like equity markets are telling us that many investors are still happy to take higher risks by owning shares, although the fact that markets aren’t racing ahead implies that some investors are worried about the risks of a recession.

And the rally in bond prices (which move in the opposite direction to bond yields) would suggest investors are indeed getting worried and are loading up on fixed income for fear of economic turmoil.

In Europe, yields on German government bonds, known as bunds, last month hit their lowest level in 700 years as money rushed into supposed safe havens. The yield on the German 10-year bund hit -0.2% meaning that investors are now paying the German Treasury to own its bonds.

The collapse in eurozone bond yields is being exacerbated by a sharp fall in inflation as its core economies contract. The key issue for the European Central Bank should be to avoid the spread of a deflationary mindset.

At the moment it faces its own internal battle as France and Germany vie to install their respective candidates as the next president.

WHAT IS THE LATEST ECONOMIC DATA TELLING US?

With investors fretting over inverted yield curves, trade wars and falling stock markets, does it really mean the global economy is about to go into recession? Thankfully the answer is no, at least not yet.

The US has record high employment and corporate profits, and economic growth is expected to decelerate from its peak toward a more sustainable level around its long-term potential.

The trade war with China is escalating to the point where growth could be meaningfully impacted.

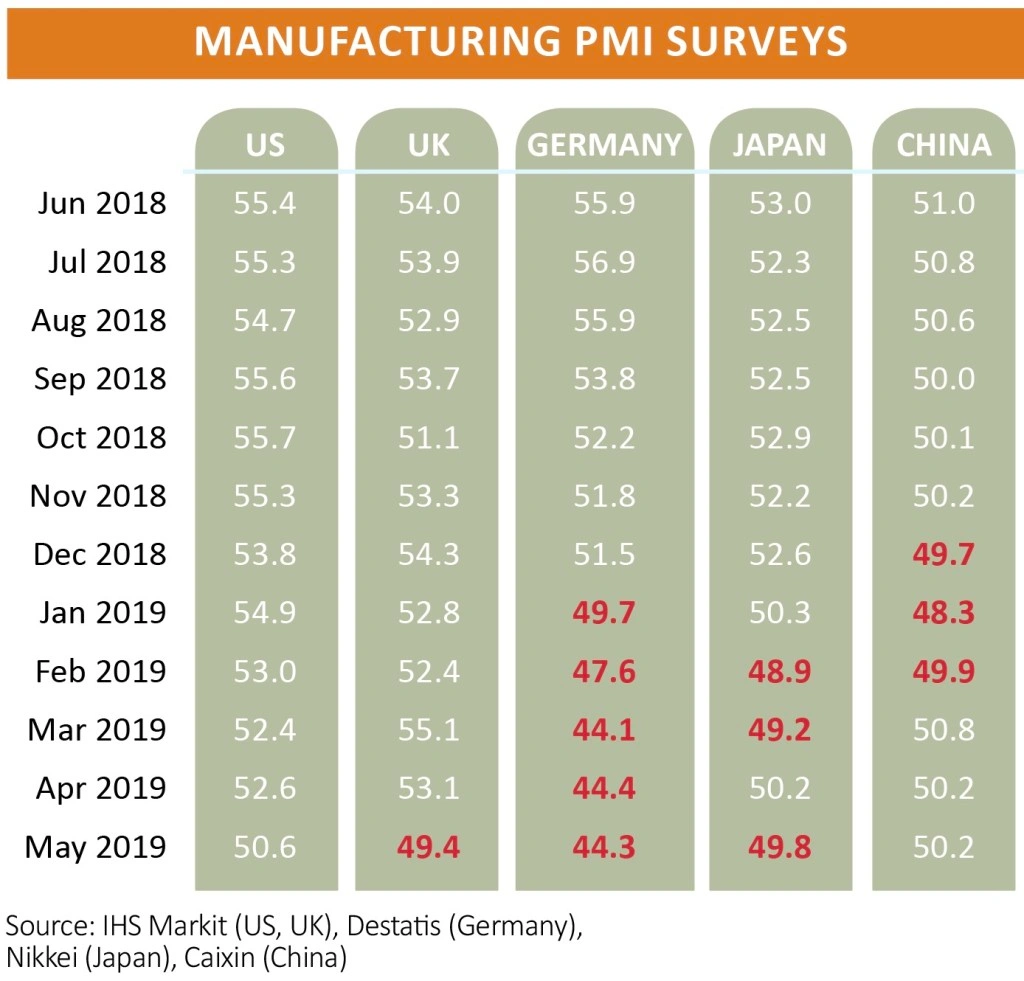

The May US purchasing managers’ index (PMI), our preferred measure of industrial confidence, was well below estimates hitting its lowest level since mid-2016 at 50.6. On the plus side it was still above 50 which is the level separating economic expansion from contraction.

China’s PMI is also just above 50, but it has been flat-lining for the past year. PMIs in Japan, South Korea, Malaysia and Taiwan are all below 50 as fears of a slowdown in global trade spook manufacturers.

The worst PMI reading for any major country is Germany at 44.3, and worryingly the reading has been below 50 all year. It’s tempting to blame global trade wars or one-offs like the change in car regulations, which hammered the auto-makers, but the fact is trade within Europe is slowing.

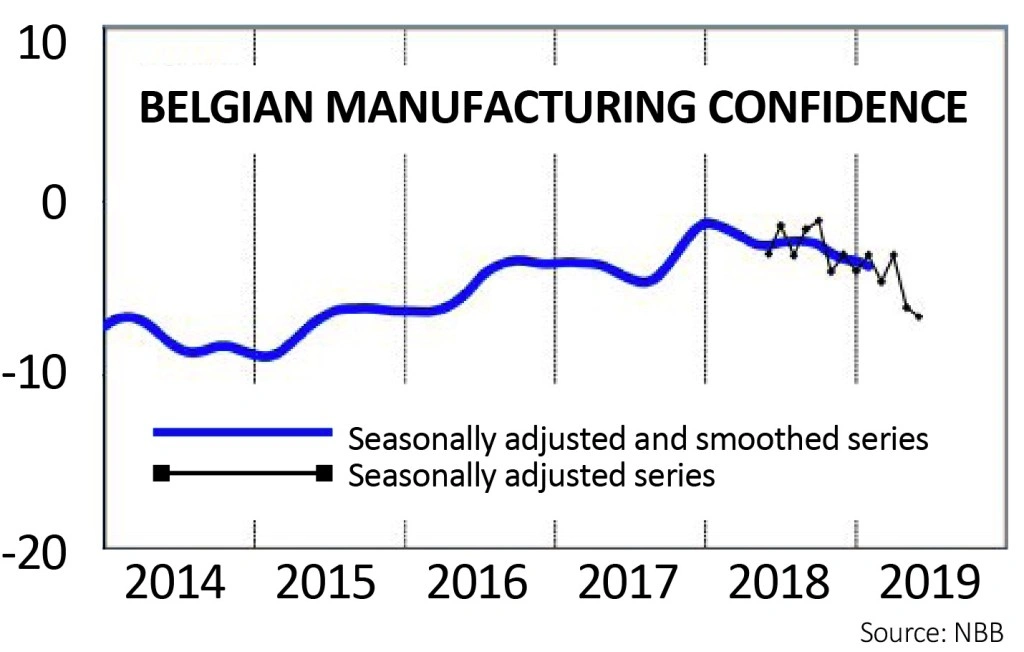

Few people bother looking at Belgian economic data, yet Belgium matters when weighing up Europe. Over 70% of its imports and exports are intra-EU. Imports in particular have slowed sharply in the last year and manufacturing confidence is lower than three years ago. And three years ago it was rising, now it’s falling.

Thanks to the ongoing Brexit saga, UK economic data is mostly gloomy. Manufacturers are as glum as elsewhere with the May PMI sinking to 49.4, the lowest since the referendum.

Business confidence and consumer spending are down and loan growth hit a five-year low in April. Yet perversely consumer sentiment is up so it would seem the hopes of the nation rest on its shoppers.

THREE BIG GEOPOLITICAL ISSUES TO WATCH

1. Slowing growth

It is little wonder Trump’s trade policies are having such an influence on the market mood. The latest report from the World Bank suggests Trump’s trade wars with everyone from China to Mexico, Canada and the EU are depressing global investment, prompting it to downgrade growth expectations for the global economy this year to 2.6%, down from 2.9% predicted in January.

A G20 leaders’ summit in Osaka, Japan at the end of June could be significant in either escalating or dialling down trade tensions.

The managing director of French asset manager Carmignac, Didier Saint-Georges, says: ‘For the first time in thirty years, geopoli-tics could once again take prece-dence over world trade.’

2. Commodities supply and demand

A drop-off in global trade has negative implications for commodities demand including crude oil, and a continuing surplus of US oil is also depressing prices. These situations are naturally bad for shares in mining, oil and gas companies.

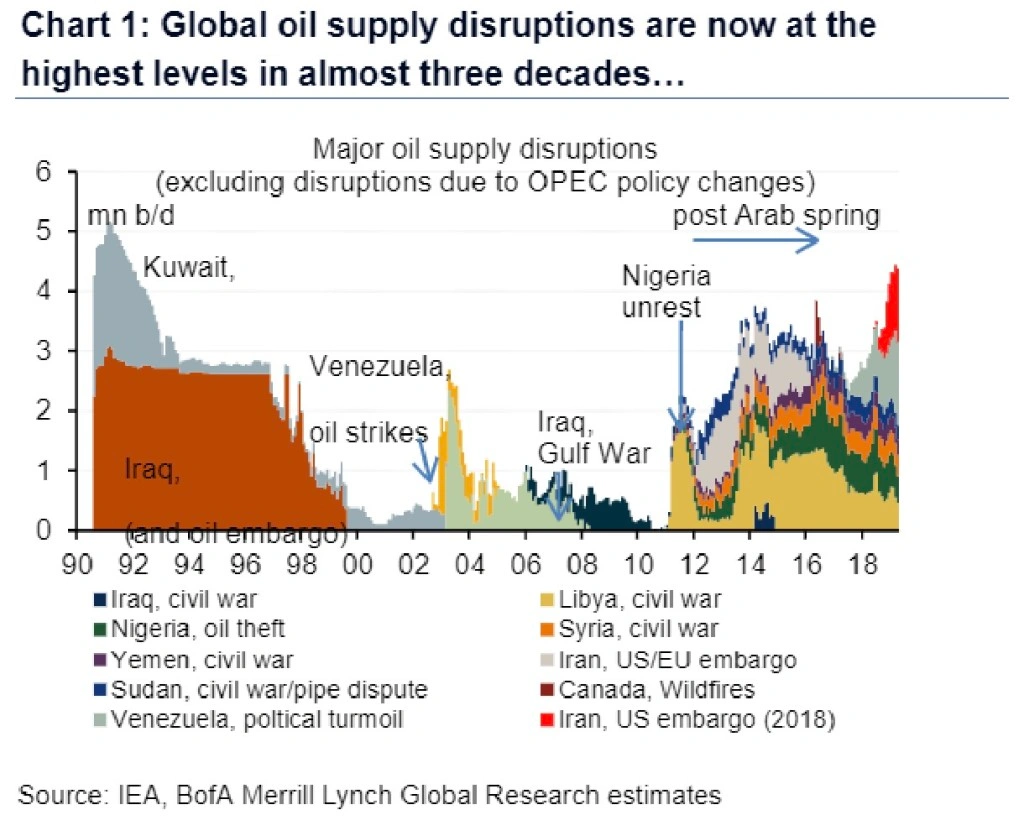

Another geopolitical issue dominating the agenda is the growing turmoil in the Middle East and the impact this could have on the supply of crude oil. This includes the impact of renewed sanctions on Iran, conflict-driven supply disruptions in Libya as well as recent incidences of industrial sabotage on key infrastructure in Saudi Arabia.

Oil producers’ cartel OPEC faces a tough balancing act at its meeting on 25 June as it determines whether it should extend production cuts.

Investment bank BoA Merrill Lynch says: ‘Global oil supply disruptions are now at the highest levels in almost three decades. Global oil demand growth is running at the weakest rate since 2012.’

3. Conservative Party leadership contest and Brexit

In the UK, the ongoing Brexit saga means the markets will have to take an interest in how 330 Conservative MPs and 100,000 party members vote in the leadership battle later this summer – with the winner likely to take the keys to Number 10.

Brexiteer Boris Johnson is the favourite with the bookies to win, although in previous Tory leadership contests the eventual winner has often come out of the left field.

In order to win the support of the membership any candidate will likely have to espouse support for a hard Brexit, although where the parliamentary arithmetic will allow them to deliver remains to be seen.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.