Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineIs the post-Covid luxury goods boom coming to an end?

Alongside the rally in mega cap tech names since January, one of 2023’s big themes is the popularity of global luxury goods stocks, with LVMH (MC:EPA), Richemont (CFR:SWX) and Hermès (RMS:EPA) hitting new share price highs amid an extraordinary boom in sales, supported by a demand rebound from China. LVMH even became the first European company to surpass $500 billion in market value.

But some parts of the sector have come off the boil more recently due to a post-Covid China reopening that appears to be losing momentum and softer sales in the US, which has been a major driver of luxury spending for the last three years.

Signs of cracks appearing in the luxury goods market, with diamond prices falling alongside the value of second-hand luxury watches in a market being flooded with supply, haven’t gone unnoticed by investors.

WHAT ARE COMPANIES SAYING?

Last month, British luxury goods brand Burberry (BRBY) reported a drop-off in sales in the Americas, while shares in high-end watches and jewellery seller Watches of Switzerland (WOSG) have tumbled more than 20% year-to-date after warning of a slowdown in growth.

Across the pond, shares in Capri (CPRI:NYSE), the owner of the Versace, Jimmy Choo and Michael Kors brands, are down 33% year-to-date and the company has cut its sales forecast amid weakening demand for its shoes and handbags.

Even luxury bulls will concede there is a cyclical aspect to industry demand linked to consumer confidence, but there is also a secular trend for affluent shoppers around the world to spend more time buying and enjoying luxury, premium and heritage-rich products.

The wealthy clientele of names like LVMH, the conglomerate behind Louis Vuitton, Christian Dior, Tiffany, Givenchy and Hennessy cognac, are relatively insulated from cost-of-living pressures.

Nevertheless, sales appear to be softening as even the well-heeled pare back spending, perhaps because the appetite for post-pandemic ‘revenge spending’ has been sated, or the rich are prioritising travel and experiences instead.

Morgan Stanley says: ‘Corporate messaging around performance in the US was relatively more subdued, albeit with management teams still pointing to a soft landing, with no dramatic slowing (on aggregate).’

However, in mainland China, Morgan Stanley says luxury management teams ‘alluded to strength in the higher-income consumer, and hence higher positioned brands. More encouragingly, we found companies upbeat on the return of incremental spend from the Chinese tourists, noting Chinese nationals have clearly started to travel and spend abroad, with Hong Kong and Macau raking in the first benefits.’

WHY INVESTORS LOVE LUXURY GOODS

Shares of the leading companies in the fragmented global luxury goods market are rarely cheap. The reason is that the businesses behind aspirational fashion brands or premium drink products are blessed with the pricing power and fat margins which are prized by investors.

These high margins enable them to generate oodles of cash which can be used to invest in marketing and brand building, fund acquisitions or pay progressive dividends.

Luxury stocks also offer exposure to structural drivers including the growth of the Chinese middle class as well as the unstoppable rise of digital sales and the ascendancy of internet-savvy Millennials and Generation Z.

One top money manager sitting on the sidelines for now is Freddie Lait, who manages the Latitude Horizon (BDC7CZ8) and Latitude Global (BMT7RH1) funds. ‘We like the luxury stocks,’ he informs Shares, ‘though we don’t own any at the moment but there’s definitely a few on our list. It is really a valuation point; they’ve done incredibly well. They are rare gems in the European market so they trade at a stark premium, but we keep models on three or four of those stocks and one day I’m sure we’ll reinvest back in.’

Lait believes it is ‘less likely’ luxury stocks will be immune to a slowdown if we get one later this year, yet stresses they’ve been great stories for the last 20 years. ‘They’ve had very steady volume and price growth, they haven’t just been gouging their customers. Unless you have a strong view that the upper echelon of spenders is going to suffer particularly, I think they’ve probably got a reasonably good future ahead of them.’

WHICH NAMES ARE CLASSIFIED AS LUXURY GOODS STOCKS?

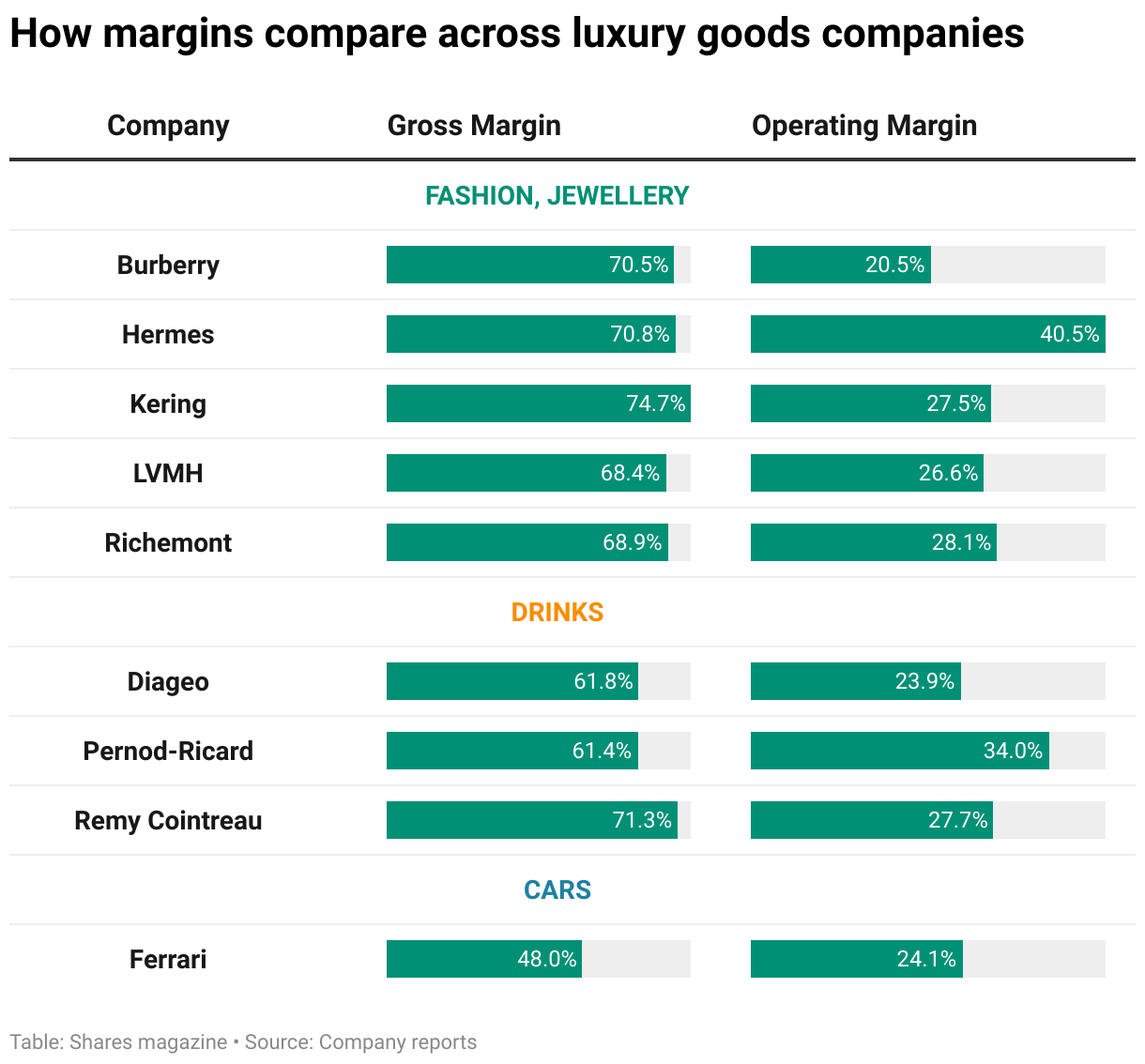

As the table shows, genuine luxury goods companies such as LVMH and Burberry, Cartier-to-Montblanc brands-owner Richemont, Birkin bag maker Hermès (RMS:EPA) and Yves Saint Laurent-to-Gucci owner Kering (KER:EPA) generate gross margins in the high sixties-to-low seventies percentage range, reflecting their ability to price coveted products materially ahead of inflationary costs.

Premium drinks companies such as Diageo (DGE) and spirits rival Pernod Ricard (RI:EPA) are routinely lumped in with the broader luxury sector, since they offer exposure to similar themes. But as the data demonstrate, their gross margins are lower than what we’ll call ‘genuine’ luxury goods companies, with Remy Cointreau (RCO:EPA) an outlier.

As Lindsell Train fund manager James Bullock explains, this reflects product mix, price point and positioning, since Remy Cointreau is overwhelmingly in the cognac category and the majority of its revenues are ‘premium, with a big proportion of super-premium within that’.

Diageo has a respectable proportion of revenues from premium and above, ‘but not quite on the same level as Remy,’ stresses Bullock. ‘Premiumisation is a very powerful driver of gross profit, as Diageo picked out in its 2022 annual report. So, we appreciate Remy’s distinct skew to premium and super-premium and are highly supportive of Diageo’s stated goal of further premiumisation across its entire brand portfolio.’

WHICH FUNDS PROVIDE LARGE EXPOSURE TO THE LUXURY GOODS SECTOR?

One way to get diversified exposure to lots of different luxury names is through exchange-traded fund Amundi S&P Global Luxury ETF (LUXG).

This product tracks the S&P Global Luxury index which is made up of various companies involved in the provision or distribution of luxury goods or services, including LVMH as well as Richemont, Kering, Estée Lauder (EL:NYSE) and Pernod Ricard.

Another relevant product is GAM Multistock Luxury Brands Equity Fund (B637645), which has 8.6% of its portfolio in LVMH, 5.6% in Hermès, 5% in Ferrari (RACE:NYSE) and 4.9% in Richemont.

Buy and hold investor Nick Train from asset manager Lindsell Train likes companies with luxury, premium or aspirational brands. His Finsbury Growth & Income Trust (FGT) holds cognac and liqueur maker Remy Cointreau, Johnnie Walker-to-Don Julio brands owner Diageo as well as Burberry.

The Zehrid Osmani-managed investment trust Martin Currie Global Portfolio (MNP) invests in Italian luxury apparel brand Moncler (MONC:BIT) as well as Ferrari, the high margin luxury carmaker able to price its products at a 25% to 75% premium to its nearest competitors with a focus on ultra-premium limited releases.

Martin Currie Global Portfolio has a position in L’Oréal (OR:EPA), as does the Gerrit Smit-guided Stonehage Fleming Global Best Ideas Equity Fund (BCLYMF3), whose top 10 also includes LVMH and lenses-to-sunglasses leader EssilorLuxottica (EL:EPA).

SHARES’ TOP STOCK PICKS

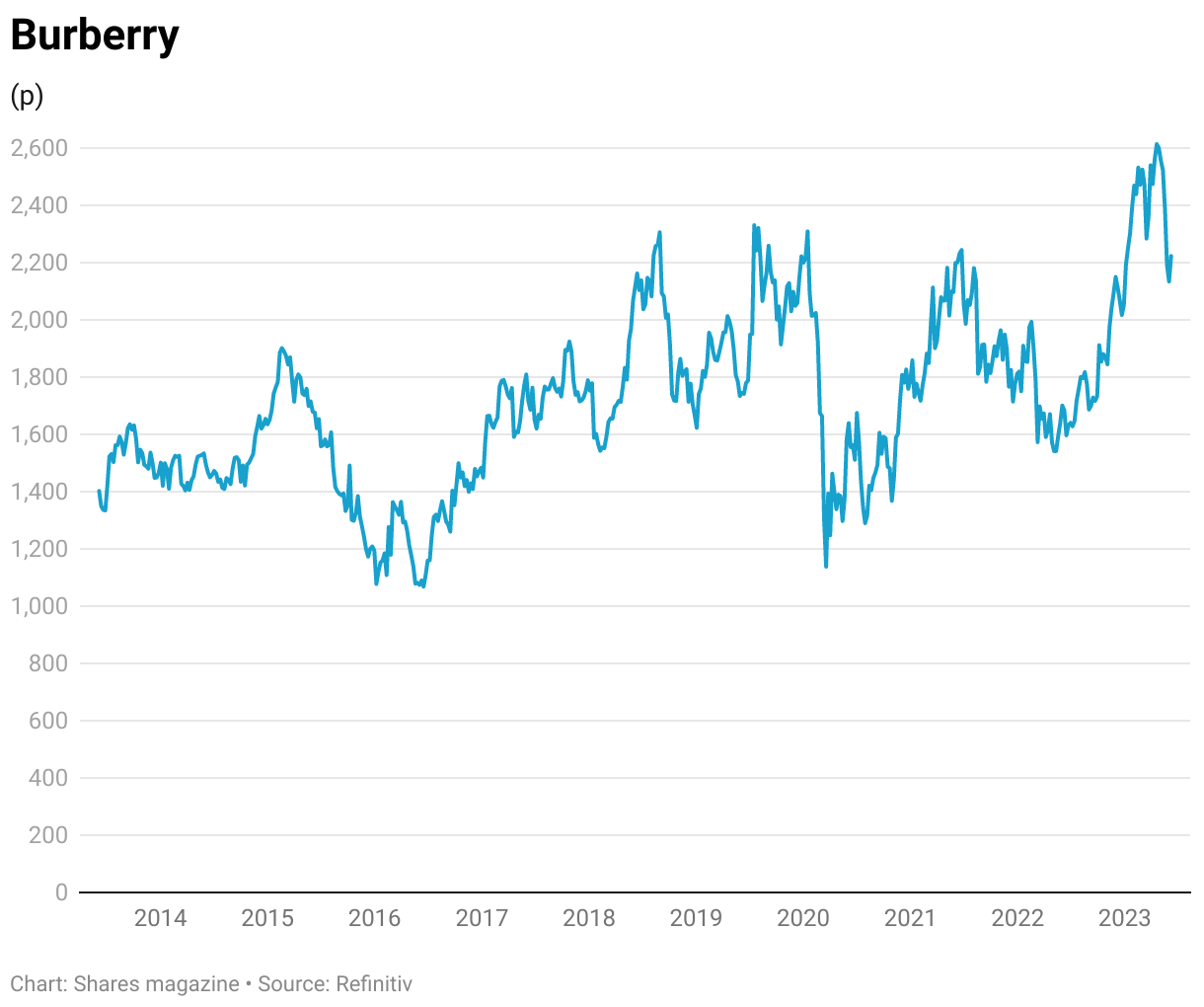

Burberry (BRBY) £22.17

A pullback from all-time peaks at Burberry presents a buying opportunity in what star stock picker Nick Train describes as ‘one of a rarefied group of truly global luxury goods brands’ with an important position in the hearts of Asian consumers.

At these levels, the rainwear-to-leather goods expert swaps hands for 17.9 times forward earnings, a material discount to LVMH and Hermes.

Results for the year to March 2023 showed profits, margins, free cash flow and dividends heading in the right direction with sales growth accelerating to 16% in the fourth quarter as growth rebounded in China.

Refocusing on ‘Britishness’ under chief executive Jonathan Akeroyd and new designer Daniel Lee, Burberry reported 19% growth in Asia Pacific for the fourth quarter.

Though the market was spooked by softness in the Americas, Burberry strutted in with double-digit growth in Japan and the EMEIA (Europe, Middle East, India, Africa) region. Often rumoured as a bid target, Burberry’s history as a quoted company is impressive, having listed back in 2002 at a share price of circa 200p and with annual sales of circa £500 million. Sales topped £3 billion last year and are forecast to exceed £3.3 billion in the year to March 2024.

L’Oreal (OR:EPA) €399

Paris-based personal care company L’Oreal’s long-run share price chart is a thing of beauty. And while a prospective price to earnings ratio of 33 appears punchy, it is actually cheap relative to L’Oreal’s trend PE history and is merited by the quality of the world’s largest cosmetics company’s model, strong margins and brand power.

The haircare, makeup and fragrances powerhouse demonstrated its pricing power in the first quarter of 2023 by generating better-than-expected 13% like-for-like sales growth and reporting a ‘spectacular performance’ in emerging markets.

Stonehage Fleming Global Best Ideas Equity Fund manager Gerrit Smit believes L’Oreal is ‘superbly positioned’ within the dermatological beauty market, with consumers eager to slow the ageing effects on their skin by splashing out on products such as La Roche-Posay.

A robust balance sheet is also enabling L’Oréal to complement organic growth with acquisitions such as Australian skincare brand Aesop, recently purchased in a $2.5 billion deal on approximately 1.4 times net asset value.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Great Ideas

News

- What El Niño means for commodity markets and how to play strong crop prices

- Gym Group faces macroeconomic headwinds and consumer behaviour shift

- UK banks’ profit margins under threat as pressure grows to boost rates on savings accounts

- Biotech companies in demand as pharmaceutical companies spend billions on takeovers