Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

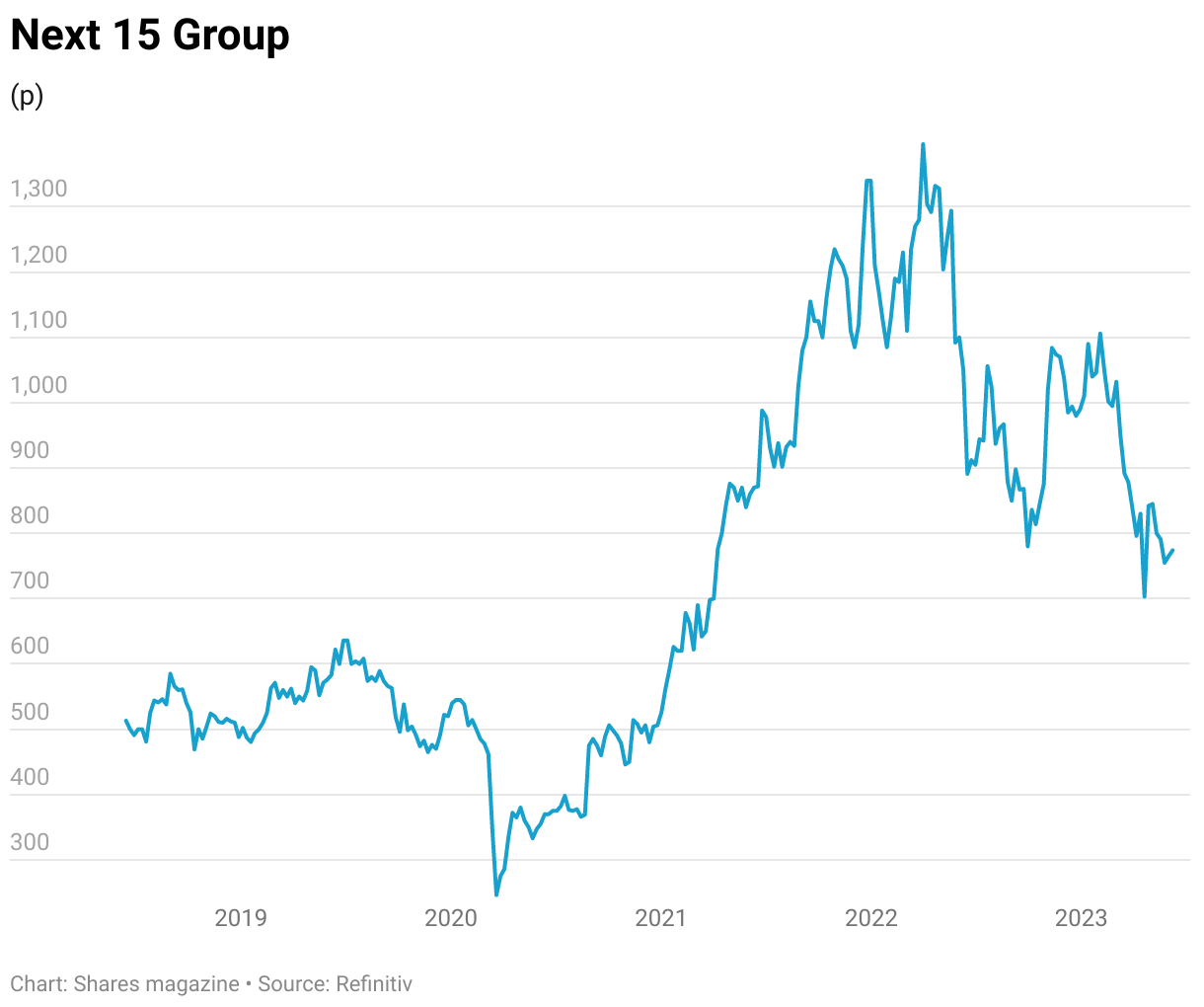

magazineBargain shares: Next 15 at a 40% discount to its 10-year average valuation

The current share price of digital communications and media firm Next 15 (NFG:AIM) represents a compelling buying opportunity.

With a strong track record, plans to double its 2022 sales of £362 million by 2026 and robust cash flow underpinning future acquisition opportunities, we think the value on offer will be unlocked. If that doesn’t happen, we believe an industry or private equity player will step in with a takeover bid.

Based on forecasts from Berenberg, Next 15 trades on a free cash flow yield of 10.8% and a PE (price to earnings) ratio of 8.4 for the year to 31 January 2024. This represents a near-40% discount to its 10-year average rating.

Market sentiment towards Next 15 has been hit by job cuts and retrenchment in spending by big technology companies in the US, where the company has some exposure. However, in a reassuring set of full-year results in April the company noted a pullback in client spend in the global technology sector had been balanced out by growth in other areas, including the public sector.

The firm is not just a play on tech. A confluence between advertising and technology creates its own opportunities for a company like Next 15 which has a growing portfolio of digital consultancy and data analytics specialists to complement an already well-regarded and established content and branding operation.

Next 15 operates across four divisions with four separate skill sets including: Insight – delivering business insights through data analytics and online research; Engage – optimising digital brands to drive engagement with consumers; Delivery – helping its client base improve sales through areas like e-commerce platforms and account-based marketing (focusing resources on winning accounts in a specified market); and Transform – providing support on business set-up and corporate positioning.

As a group, Next 15 generates an operating margin from these activities of around 20%. Clients span Google-owner Alphabet (GOOGL:NASDAQ) to the Department for Education and AstraZeneca (AZN).

The company generates lots of cash and this is reflected in a strong balance sheet, with net cash of £26.1 million as at the end of the 2023 financial year despite allocating £93.6 million to takeovers in the preceding 12-month period. The largest of which was creative agency Engine for an enterprise value of £77.5 million.

The integration of this business is going well and Next 15 has form for successfully executing on M&A, with acquisitions set to play a key role in achieving the group’s ambitious sales target.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Great Ideas

News

- What El Niño means for commodity markets and how to play strong crop prices

- Gym Group faces macroeconomic headwinds and consumer behaviour shift

- UK banks’ profit margins under threat as pressure grows to boost rates on savings accounts

- Biotech companies in demand as pharmaceutical companies spend billions on takeovers