Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUK banks’ profit margins under threat as pressure grows to boost rates on savings accounts

The banking sector is under pressure to be more generous with interest rates on savings accounts, which is negative for their profit margins.

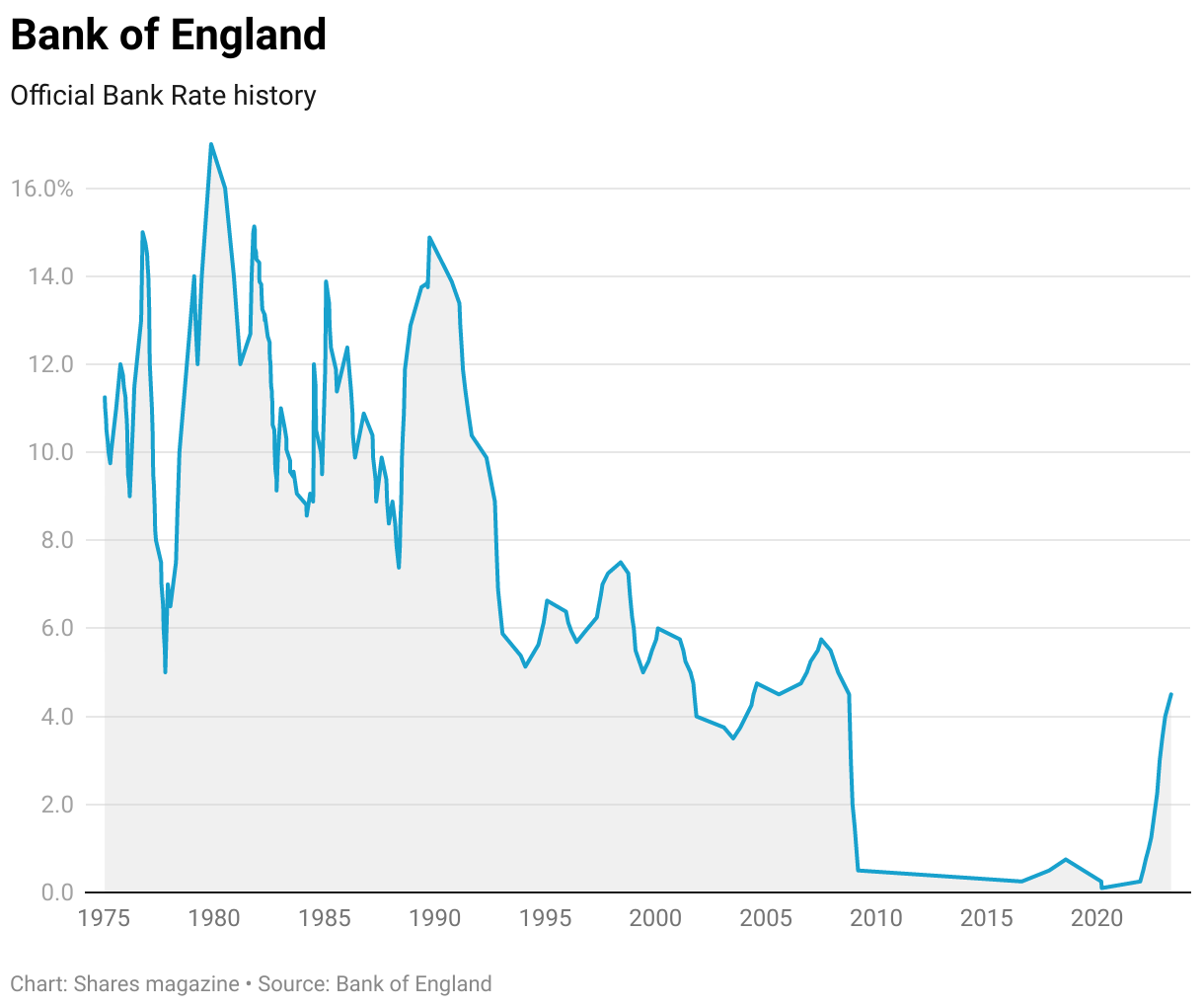

In February, an influential parliamentary committee opened an inquiry into why the interest rates paid on easy-access savings accounts by the ‘big four’ UK high-street banks – Barclays (BARC), HSBC (HSBA), Lloyds (LLOY) and NatWest (NWG) – were so much lower than the Bank of England base rate.

At the time, the big banks were offering between 0.5% and 0.65% on easy-access savings accounts compared with a base rate of 4%. Today, they are still only offering between 0.7% and 1.35%, while the Bank of England base rate is 4.5%.

Last week, the cross-party Treasury Committee delivered its verdict, blasting the ‘big four’ – and the four ‘scale challengers’, which include Virgin Money (VMUK), who account for a quarter of all personal current accounts – for charging what it called a ‘loyalty penalty’ on their customers, ‘especially elderly and vulnerable customers who may still rely on high street bank branches’.

‘With the Bank of England confirming the pass-through of base rate increases to easy access savings accounts has been unusually weak, it’s clearer than ever that the nation’s biggest banks need to up their game and encourage saving,’ declared chair Harriett Baldwin MP.

‘While other products are available to those who shop around, the measly easy-access rates on offer lead us to conclude that loyal customers are being squeezed to bolster bank profit margins.’

Jenny Ross, editor of Which? Money, also weighed in: ‘Our research has shown that high street banks have been short-changing savers by paying unjustifiably low rates for years – and MPs are right to hold them to account for this.

‘The introduction of the FCA’s (Financial Conduct Authority) Consumer Duty must mean tough action against firms who continue to offer such meagre rates.’

Whether the banks respond and increase their deposit rates we will have to see, but there is no question they have benefited enormously from the rise in base rates over the past year as their net interest margins have demonstrated.

Also, whether the Treasury Committee has the power – or even the right – to intervene in who offers what rate on UK bank deposits is debatable as it is not a regulatory body.

However, it is probably worth noting that while rates on easy access accounts have risen slowly, they have risen by more on ‘time deposits’ as the big banks attempt to lock in savings, resulting in a significant shift in deposit volumes out of instant access accounts over the last six months, according to the Bank of England’s latest Monetary Policy Report.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Great Ideas

News

- What El Niño means for commodity markets and how to play strong crop prices

- Gym Group faces macroeconomic headwinds and consumer behaviour shift

- UK banks’ profit margins under threat as pressure grows to boost rates on savings accounts

- Biotech companies in demand as pharmaceutical companies spend billions on takeovers