Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

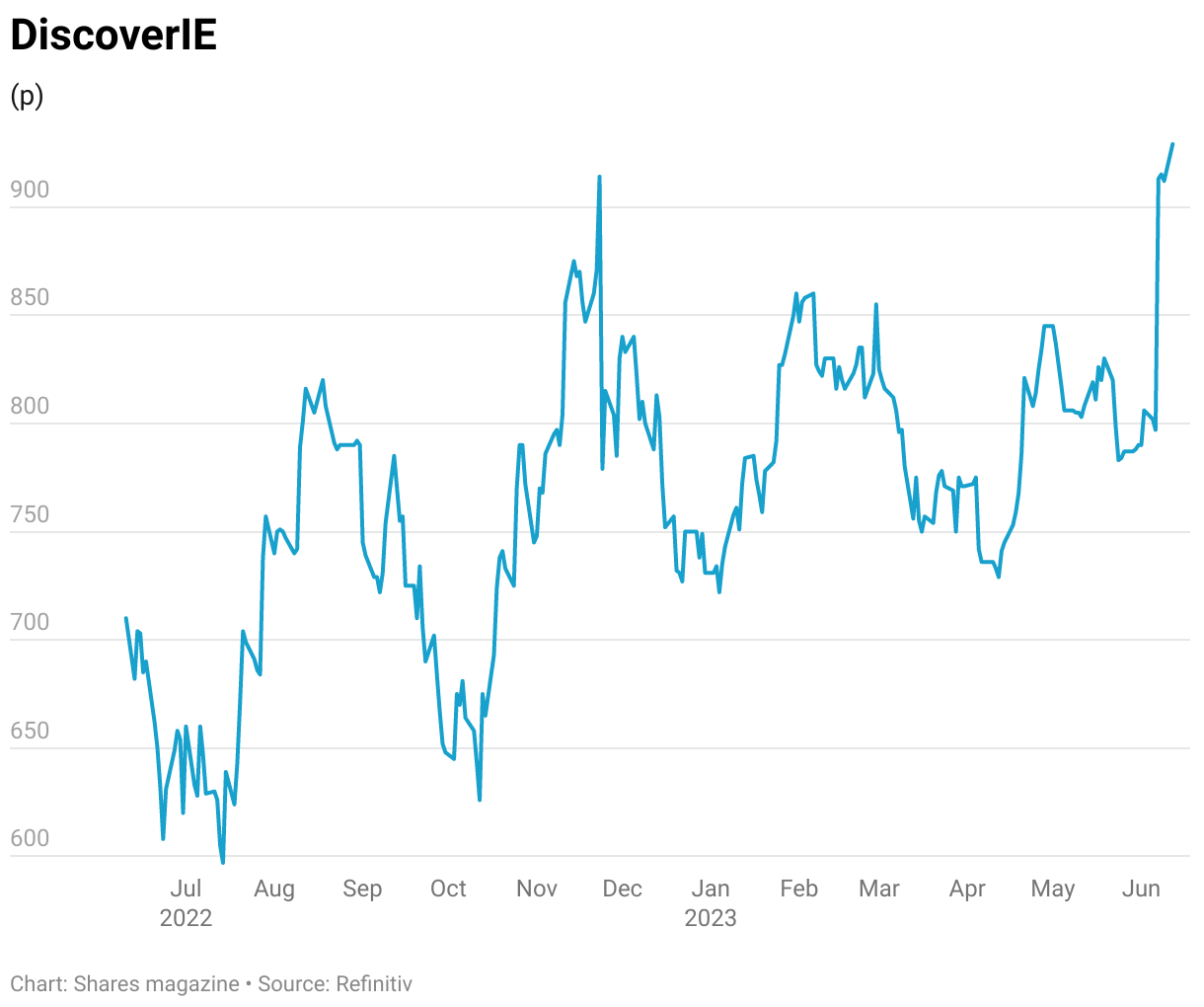

magazineThe story behind a 27% advance in DiscoverIE shares since last August

DiscoverIE (DSCV) 930p

Gain to date: 26.9%

We flagged the appeal of electronics engineer DiscoverIE (DSCV) in August 2022 at 733p, arguing the company was not being given credit for its inherent qualities and its growth potential.

WHAT’S HAPPENED SINCE WE SAID TO BUY?

We have been proved right in spades. The market has reacted positively to good news from the company which culminated in a robust set of results for the 12 months to 31 March, published on 7 June. Revenue increased 18% to £449 million but even more significantly, underlying profit surged 23% to £45.3 million as the company’s profitability improved despite ongoing inflationary pressures.

Free cash flow was up 51% to £31 million which CEO Nick Jefferies tells Shares was achieved thanks to a combination of strong growth and ‘tight control of inventory and working capital’ or ‘good housekeeping’ as he describes it.

The company is well-positioned for further growth with an order book of £223 million and a strong pipeline of acquisition opportunities. The financial ability to execute on M&A opportunities is clear with the company on a comfortable 0.7 times debt to earnings ratio.

FinnCap analyst Guy Hewett says: ‘The group’s products are designed-in and essential to customer applications but only represent a small proportion of the total cost, representing a highly valuable strategic position within the structurally growing target markets of renewables, transportation, medical, and industrial and connectivity.’

Hewett adds: ‘DiscoverIE’s proven growth strategy, focused on long-term, structurally growing markets across Europe, North America and Asia, and a diversified customer base, continues to deliver despite the difficult macro background.’

WHAT SHOULD INVESTORS DO NOW?

Keep buying shares in this excellent company. It has the levers to pull to achieve further growth despite a rocky economic backdrop and, while the shares are no longer the value opportunity presented last August, a price to earnings ratio of 26 times looks more than justified in our view.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Great Ideas

News

- What El Niño means for commodity markets and how to play strong crop prices

- Gym Group faces macroeconomic headwinds and consumer behaviour shift

- UK banks’ profit margins under threat as pressure grows to boost rates on savings accounts

- Biotech companies in demand as pharmaceutical companies spend billions on takeovers