Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStrike it rich: three oil and gas stocks with big opportunities

After a strong 2022 as energy prices surged in the wake of Russia’s invasion of Ukraine, the UK’s contingent of UK small and mid-cap oil and gas companies has endured a much more challenging time in 2023. Windfall taxes have taken a big bite out of profits and commodity markets have fallen back as fears of recession dampen demand expectations.

Facing the prospect of an unstable and more onerous fiscal regime in the UK, North Sea operators are having to broaden their horizons. There are also signs of a recovery in exploration activity, which means there are still opportunities for investors in the sector, particularly given the depressed valuations. However, the sector remains high risk and prospective investors should only buy shares in smaller oil and gas companies if they are comfortable with potentially losing money.

A CRUCIAL ROLE TO PLAY

Political and regulatory uncertainty is an undeniable challenge for the sector but the last 18 months have offered a reminder of the need for energy security alongside a gradual transition away from fossil fuels.

Even if fewer new projects are going to be sanctioned in the future, existing oil and gas fields still require careful stewardship and there needs to be a healthy independent sector beyond the big integrated energy companies.

In this article we dive into some of the big issues facing the industry, do some number crunching to identify the best and worst performers and the highest dividend yields on offer as well as identifying three stocks to buy now.

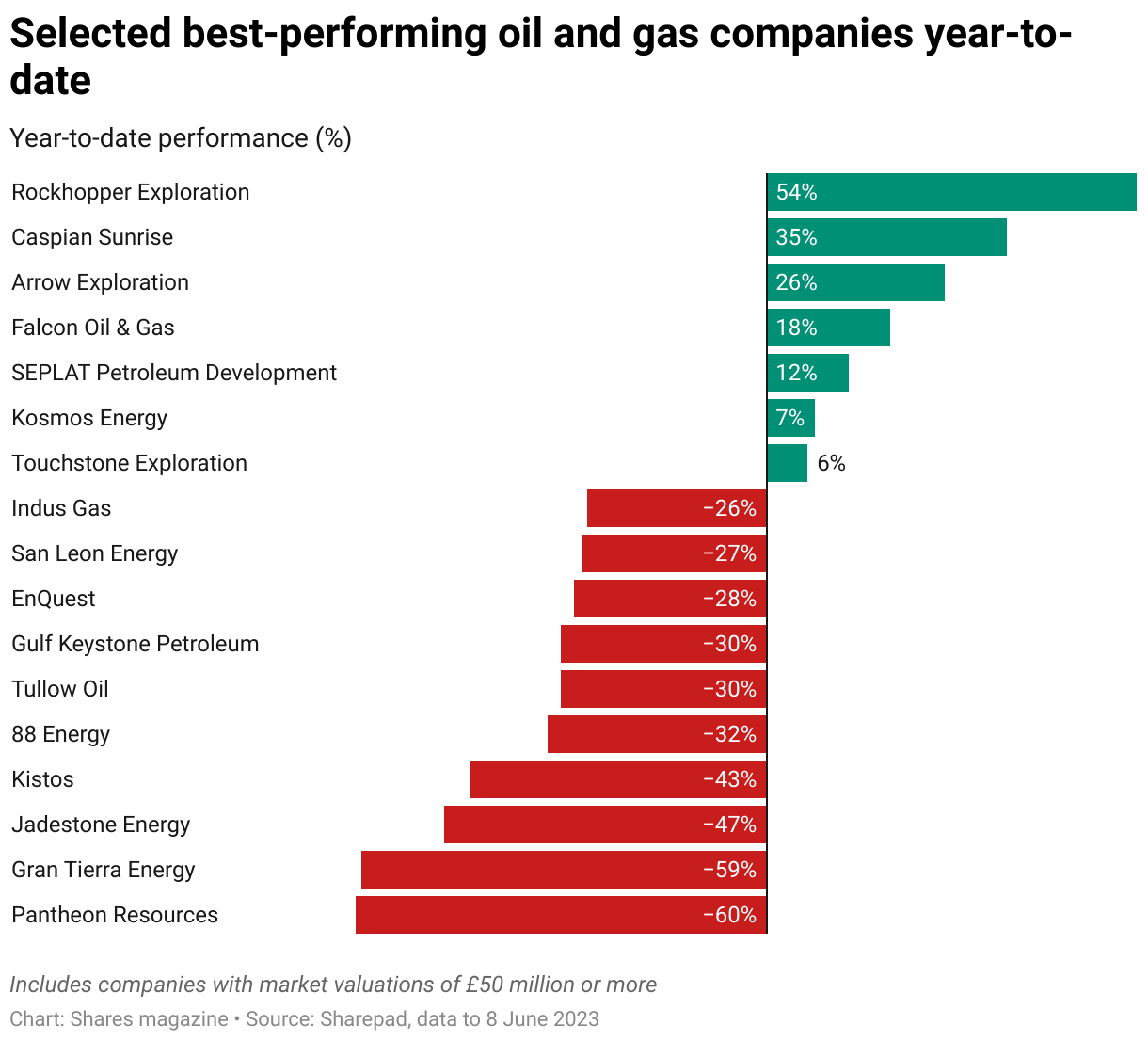

Our list of worst performers in the oil and gas space includes two prominent names with assets in the North Sea, Kistos (KIST:AIM) and EnQuest (ENQ), reflecting the impact UK windfall taxes have had on sentiment towards the sector.

As Kistos CEO Andrew Austin observes, the first version of the EPL (energy profits levy) put in place by Rishi Sunak when he was still chancellor had a mechanism by which it would drop away if hydrocarbon prices returned to the pre-invasion levels. The updated levy subsequently introduced by Jeremy Hunt once he entered Number 11 had no such get-out.

Stephen Brown at fellow North Sea play Orcadian Energy (ORCA:AIM) told Shares: ‘Hunt’s intervention in November was such a disaster and made no-one believe the windfall tax would ever go away.’

The Government has since brought forward plans for a mechanism where the tax will be suspended and the tax rate will change from 75% to pre-energy crisis levels of 40% if oil and gas prices fall below their long-term average for two consecutive quarters. This level is $71.40 for crude oil and £0.54 per therm for gas.

Brown believes that while this will not make a stark difference to the amount of tax revenue brought in by the levy it could make a difference to the financing of North Sea projects. The Orcadian boss, who is looking for an injection of capital to help progress the Pilot project in the North Sea, says: ‘In November you were like “will the phone ever ring again?” but now people are looking at opportunities once more.’

However, a Labour Party enjoying consistent polling leads ahead of a likely election some time in 2024 is also suggesting it would not award new oil and gas licences and would retrospectively remove the investment allowance afforded North Sea operators.

A ‘SHORT-SIGHTED’ APPROACH ON TAX

Kistos has assets in the West of Shetland section of the UK North Sea and Andrew Austin says: ‘Taxing the industry is seen as a victimless crime but it is very short-sighted.’

This argument may get short shrift in some quarters, particularly from those which have seen the bumper profits unveiled by BP (BP.) and Shell (SHEL). However, these companies’ largely global profits are mainly untouched by a UK windfall tax, something which is not true for the smaller, independent companies operating in the North Sea.

Unsurprisingly, there have been dire warnings from the industry about investment being pulled from UK oil and gas assets. Action is backing this dramatic rhetoric. The latest development saw reports emerge that Harbour Energy (HBR) is considering a merger with Gulf of Mexico-focused outfit Talos Energy (TALO:NYSE) with a potential move to a US stock market listing.

The boss of Serica Energy (SQZ:AIM), Mitch Flegg, told the audience at a Shares investor evening earlier this month that although ‘no-one likes paying more tax’ the ‘short-cycle’ nature of the company’s investments, which encompass mature, producing fields which it aims to manage more efficiently than their previous owners, typically pay back within six to 12 months. According to Flegg, this means Serica is in a different position from peers who need to make plans on a multi-year view.

For his part, Austin says: ‘We went from making 65p to 20p in the pound. It is incredibly risky to invest in the UK right now, there is too much uncertainty to make rational decisions.’

The company has already added to its UK and Netherlands assets with an acquisition in Norway, which has a more stable tax regime and generous incentives for exploration and appraisal drilling, and Austin says he is ‘not ruling out anything out’ in terms of future deals in other geographies. ‘We can’t afford to,’ he concludes.

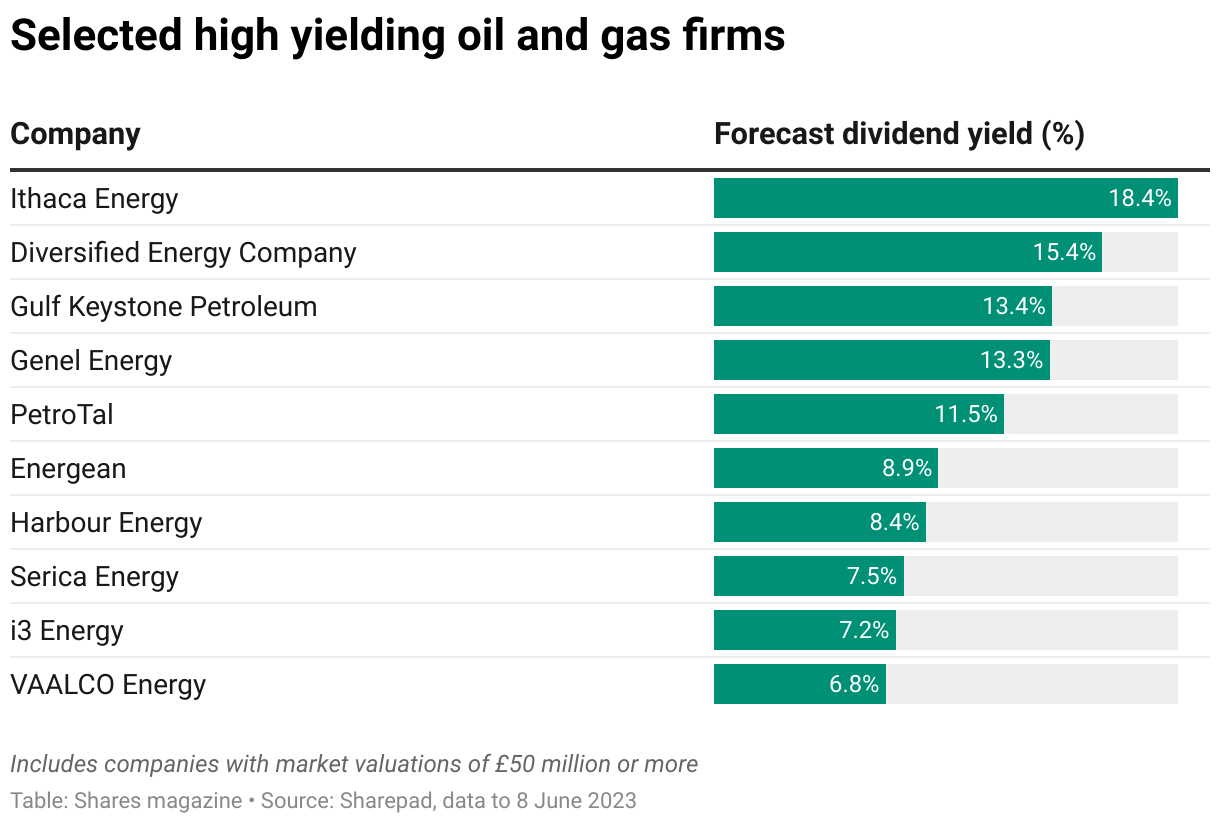

High-yielding oil stocks

Small and mid-cap oil and gas firms have not historically paid dividends but after years of being neglected by investors who were not getting the kind of outsized returns they anticipated from oil and gas exploration, amid a lack of big discoveries, a number changed direction and started returning cash to shareholders.

Diversified Energy Company (DEC) 93.6p

A significant sell-off in the shares of US natural gas producer Diversified Energy Company (DEC) reflects weaker North American gas prices. However, the company’s model of acquiring mature fields with low rates of production decline and using its cash flow to sustain generous dividends is a tried and tested one.

The company has hedged gas prices out to 2025 which should provide greater visibility on revenue and cash generation. The company also received a boost after a syndicate of 14 banks reviewed the North American oil and gas firm’s borrowing base and maintained it at $375 million, giving the company liquidity to pursue further deals to increase its production. On this basis we think a 15.4% dividend yield is an anomalous opportunity rather than being too good to be true. Buy the shares.

A RECOVERY FOR EXPLORATION

As well as broadening geographic horizons, there are signs companies are becoming more expansive when it comes to exploration.

Morgan Stanley analysts note: ‘Concerns around the energy transition and volatile energy prices meant exploration (particularly of frontier basins) was an unloved theme for the European majors for much of the past decade.

‘Although companies have not changed their selective stated approach towards new exploration frontiers, there are a few hotspots that appear to be attracting genuine interest from the majors.’

The investment bank flags Namibia, Suriname and the East Mediterranean. This revival in exploration is highly relevant for small and medium-sized exploration plays as it raises the prospect of majors helping to fund drilling to own a stake. For companies like Eco Atlantic Oil & Gas (ECO:AIM), which has acreage in Namibia and Suriname, this is a particularly relevant consideration.

Serica Energy (SQZ:AIM) 247p

Though Serica Energy is exposed to fiscal and regulatory risks in the UK, the nature of its approach which involves improving the performance of mature fields should insulate it from the worst of the impact.

A dividend yield of 7.5% and a price to earnings ratio of just three times consensus forecasts suggests the aforementioned risks are priced in.

Investec analyst Alex Smith observes that the 210% reserves replacement ratio (meaning Serica replaced reserves lost to production more than two times over) reported for 2022 ‘underlines the potential of the portfolio to extend the current plateau production rate for longer and to grow from current levels.’

The £367 million acquisition of Tailwind, which completed earlier in 2023, shifted the portfolio from a heavy bias towards natural gas to more of a 50-50 split with oil has also helped the company absorb the impact of lower gas prices. Cash of nearly £400 million gives Serica the firepower to pursue M&A opportunities in the sector.

Eco Atlantic Oil & Gas (ECO:AIM) 17.1p

This is a higher risk stock given it has no production and is entirely focused on exploration. However, with assets in South Africa, Namibia and Guyana, Eco Atlantic Oil & Gas is operating in attractive ‘postcodes’ in close proximity to where the majors have been making some significant discoveries.

According to investment bank Berenberg the company has prospective resources across its portfolio of 12.5 billion barrels of oil equivalent.

If the company were able to prove up even a fraction of that total through drilling it could be transformational for the group’s valuation.

The limited drilling Eco has carried out to date, including four wells in Guyana and one in South Africa, hasn’t yet yielded a commercial find but exploration often takes multiple shots at the goal to achieve success. The next stage is to agree a farm-out deal to bring new partners into its various projects and progress on this front in 2023 could act as a catalyst for the shares.

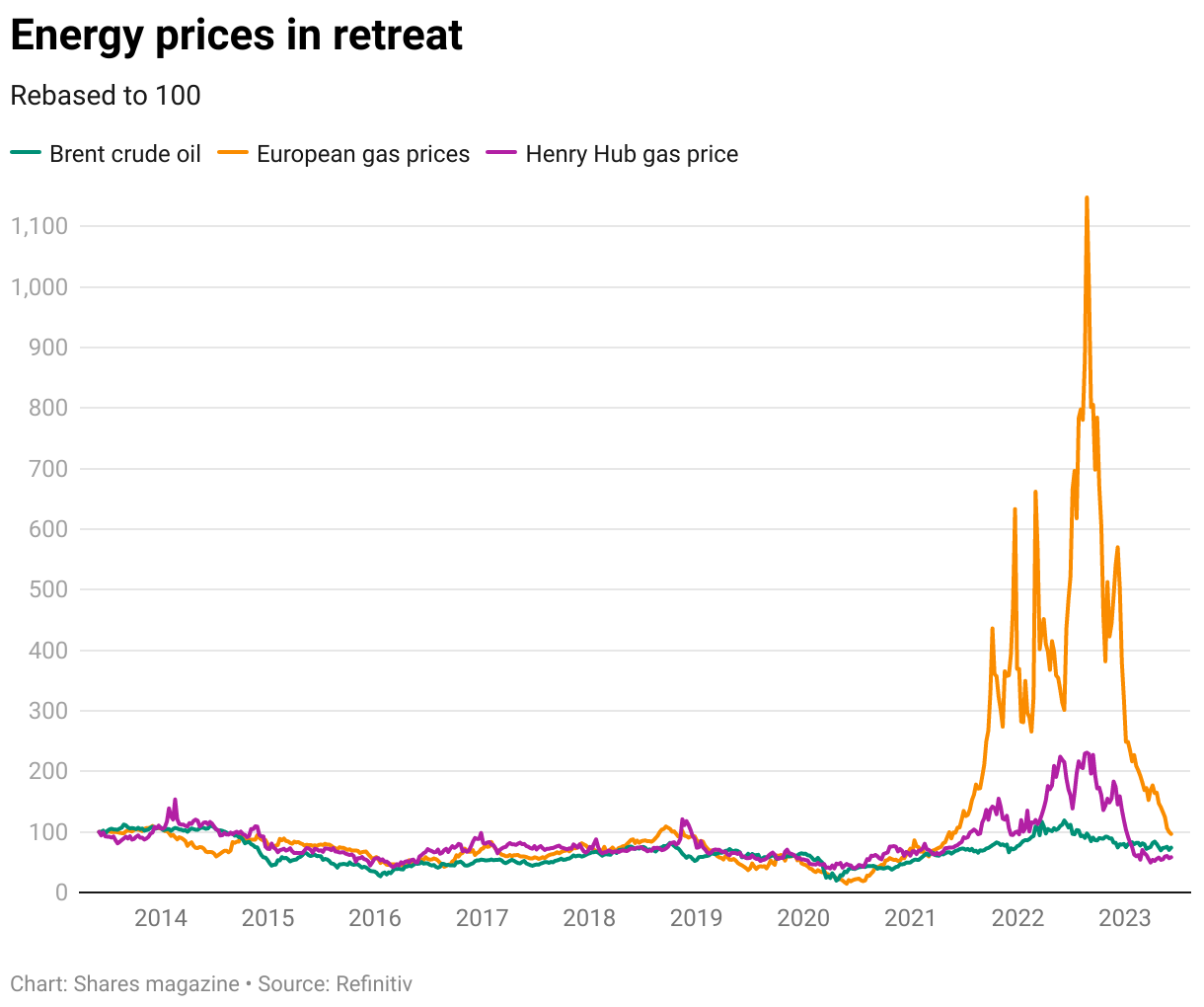

Prospects for oil and gas prices

The drop in European gas prices from 2022 highs has been more dramatic but US gas prices (represented by the Henry Hub benchmark) and oil prices have also fallen back materially as the supply problems created by the conflict in Ukraine and the subsequent sanctions imposed on Russia as well as the impact of rising interest rates have raised question marks over demand.

Francisco Blanch, commodity and derivatives strategist at Bank of America, says: ‘Two main forces have come together to pull down commodity prices from the steep increases observed last year. First, the Fed has increased interest rates at one of the fastest rates in decades in the past 15 months to contain the most pronounced spike in inflation in four decades.

‘In turn, rapid rate hikes have led to a steep contraction in money supply, triggered a banking crisis, and helped bring down inflation.

‘Second, faced with the twin evils of inflation and the first war in Europe since 1945, the US Treasury engineered a set of economic sanctions that have both minimised global commodity supply losses while also cutting tax revenues to Russia’s government.’

Saudi Arabia has looked to prop up oil prices, unilaterally deciding to cut one million barrels per day of output at the beginning of June while its partners in the OPEC+ cartel pledged to maintain their own levels through to 2024.

Bianch adds: ‘At their core, markets are witnessing a battle royale between Saudi Arabia and the US Federal Reserve, pitting prince Abdulaziz bin Salman against chair Jay Powell.

‘In this battle royale, oil has the losing hand until money starts easing again, and we maintain our average $80 per barrel Brent forecast for 2023.’

Analysts at Third Bridge do not rule out more aggressive actions from OPEC+ but argue: ‘The tug-of-war right now in the market is the seasonal versus the cyclical. We are watching to see how strong the developed world’s summer demand uptick will be relative to the struggles of China’s cyclical recovery. This will determine how effective OPEC+ will be.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Great Ideas

News

- What El Niño means for commodity markets and how to play strong crop prices

- Gym Group faces macroeconomic headwinds and consumer behaviour shift

- UK banks’ profit margins under threat as pressure grows to boost rates on savings accounts

- Biotech companies in demand as pharmaceutical companies spend billions on takeovers