Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy your pension provider will soon warn you about holding too much cash

New rules from the regulator will mean that from December this year you will get an email or letter from your pension provider if you have a lot of cash in your pension.

There are a few criteria you’ll have to meet: that more than 25% of your pension is in cash, that this figure is more than £1,000 and that you are more than five years from normal minimum pension age, which is 55 for most people. Your pension provider will have to assess this every three months, sending out a notification if you’ve met the criteria for six months.

WHAT’S IN THE LETTER?

Your pension provider will tell you about your cash levels, provide you with a calculation about how inflation is eating away at your cash, and prompt you to think about your investments and whether you need to move some of that cash into other assets. Once it has sent the letter it will do so again every 12 months that you meet the criteria.

You don’t have to take any action off the back of the email or letter and you don’t have to reply to your provider – it’s more intended as a prompt for you to think about your cash levels and whether they are right for you.

HOW MUCH CASH SHOULD YOU HOLD?

That sparks the next question, how much cash is the right amount to have in your pension? We’ve previously talked about the right levels of cash to hold generally, but the parameters are a bit different when it comes to your pension, particularly because cash in pensions doesn’t earn very much, if any, interest.

Everyone will usually have some of their pension in cash, to meet the fees and charges from their pension provider.

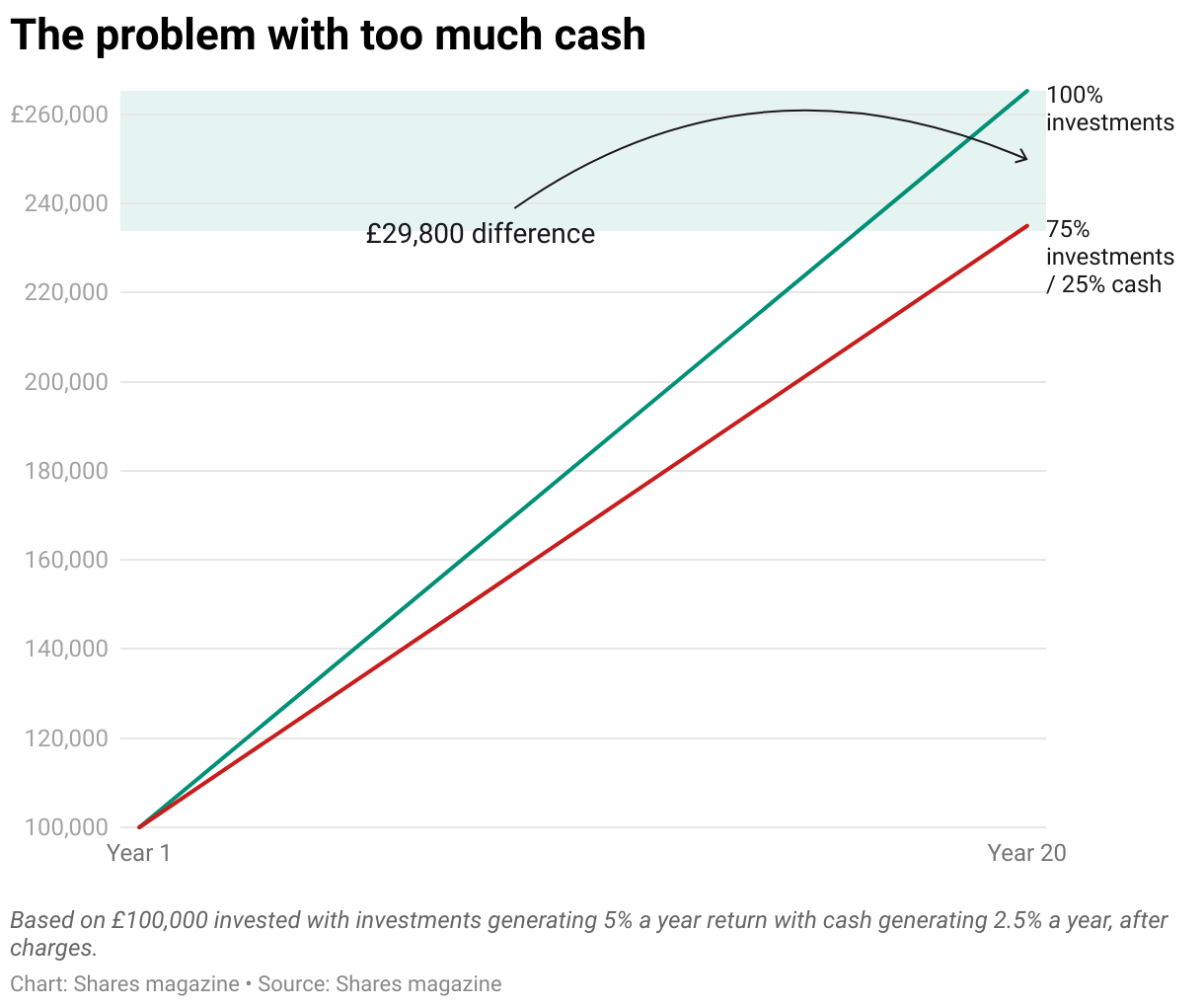

But generally it’s not a good idea to have large sums in cash, particularly over the long term. Here’s an example: A pension pot worth £100,000 that is always 75% invested and 25% in cash would be worth £235,500 after 20 years, assuming no further contributions and that the investments generate 5% annual return while cash generates 2.5% a year, after charges.

If instead that money was 100% in investments, earning 5% a year, the £100,000 pot would grow to just over £265,300 after 20 years – almost £30,000 more.

WHY INVESTORS STILL LIKE TO HOLD SOME CASH

There are a few reasons why you might have more cash than a basic amount.

1. You’re doing it as a strategic move

Some investors might want to keep money in cash if they think markets are quite expensive at that point in time and they want to keep some cash on the sidelines.

They might have sold down some investments to lock in gains and not want to deploy that money back into markets.

While it’s a tricky game to try to accurately time the markets, it’s also fair to strategically keep some money on the side if you think markets or certain investments are too pricey at the moment and you’re waiting for them to fall.

2. You want less risk in your portfolio

Whether you’re feeling nervy about markets or you just want to dial down the risk in your pension, you might decide to increase your cash levels temporarily. There’s nothing wrong with this so long as it’s a considered decision, and that you review it regularly.

Many people end up with their pension’s cash levels gradually rising over the years with no intention behind it, and that can be problematic as you could be needlessly missing out on potentially higher investment growth.

While cash isn’t going to beat inflation over the long term and isn’t going to grow your wealth by a lot, it’s fine if you want some no-risk assets in your portfolio. But it’s also worth considering whether there are some other, lower-risk assets you could invest in instead of leaving the money in cash.

3. You’re nearing the time when you want to access your pension

Previously, pensions used to be gradually moved into lower and no-risk assets as people neared retirement, with a view that they would then use that pot of money to buy an annuity. Now, most people keep their pension money invested and draw on the money as they need it.

However, you’ll likely still want to de-risk your assets as you near retirement to ensure they aren’t exposed to market falls just when you need access to the money.

Everyone will have a different timeline, depending on their financial circumstances and risk tolerance, but for many this de-risking could start many years before retirement.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Great Ideas

News

- What El Niño means for commodity markets and how to play strong crop prices

- Gym Group faces macroeconomic headwinds and consumer behaviour shift

- UK banks’ profit margins under threat as pressure grows to boost rates on savings accounts

- Biotech companies in demand as pharmaceutical companies spend billions on takeovers