Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLatest deal at newly focused DCC set to boost growth and margins

Once upon a time, Irish-headquartered distribution firm DCC (DCC) was a market darling. It traded on an elevated rating for years as it gobbled up competitors, until one day investors began to question the returns they were getting for the price they were paying.

Now, the firm is much more focused both in terms of its business areas and its capital allocation policy, with a real emphasis on generating a return on capital employed well above its cost of capital.

We think its latest deal, which broadens its presence in the US technology supply market, not only ticks that box but provides a good opportunity for us to reappraise the group.

GLORY DAYS

Investors may recall the hype about a decade ago over DCC and its so-called ‘roll-up strategy’, which drove the shares from below £15 to above £75 almost in a straight line from mid-2012 to mid-2017.

The group embarked on an aggressive programme of acquisitions to boost revenue growth, much to the market’s delight, but underlying progress was never that impressive as the markets where the firm was expanding simply didn’t grow that fast.

Operating profit margins barely budged from low single digits, and eventually the shares stalled due to their demanding valuation of over 30 times earnings. Today, at £60.96, the stock trades on a price to earnings ratio of around 17 times for the year ending in March, while margins are higher.

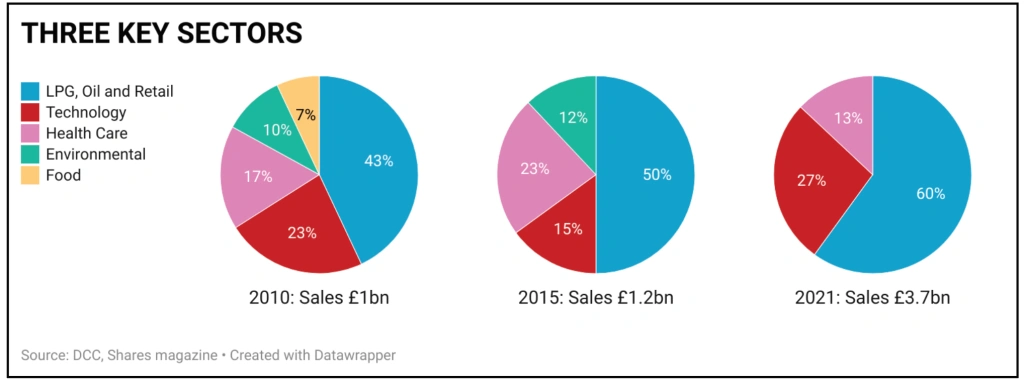

THREE IS THE MAGIC NUMBER

A decade ago, the firm turned over in the region of £1 billion a year across six different market segments. Wholesale and retail distribution of fuel oil, heating oil and LPG (liquid petroleum gas) accounted for just under half of all revenue, with the other half made up of distributing healthcare, technology, food and environmental products.

Last year, turnover hit £3.7 billion with LPG and oil accounting for 60% of sales, healthcare 13% and technology 27% of sales.

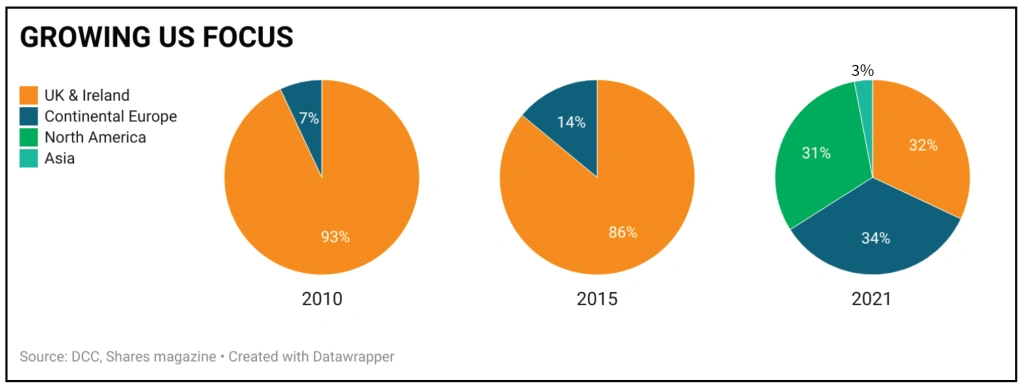

At the same time, the sales split has gone from 93% UK and Ireland and 7% Europe to 32% UK and Ireland, 34% Europe and 31% North America, with 3% coming from Asia.

ENERGY STILL CORE

DCC’s main business is the distribution of LPG and oil across the globe. It supplies LPG to industrial and commercial businesses as well as residential customers in Europe, North America and Asia.

The transition to cleaner, lower carbon energy sources and the introduction of bioLPG means demand is growing steadily, and the business generates a high return on assets.

Since entering the US gas market in 2018, the firm has spent $445 million on acquisitions to make it one of the leading players. In Ireland, its Flogas subsidiary is a top 10 supplier of LPG and has expanded into renewable electricity supply.

The second leg of the energy business is marketing and retailing oil for transportation, commercial and heating use across Europe. This business is slower growing but generates strong cash flows and high returns on capital.

The firm operates HGV re-fueling sites across the UK, helping to keep the logistics industry moving, and recently built a first-of-its-kind onsite fuel facility at the Hinkley Point nuclear power plant to supply construction firms during the build process.

ADDING VALUE IN HEALTHCARE

The healthcare division, DCC Vital, sells a range of medical and pharmaceutical products to healthcare providers ranging from acute care to GPs in the UK and Ireland as well as Germany, Austria and Switzerland.

Alongside this, the Health & Beauty business is sub-contracted by major international brands to help develop, formulate, manufacture and package their products.

While it isn’t as high-profile as the fuel business, DCC Vital is the number one supplier to GPs and the broader primary and acute care sector in the UK and Ireland, while Health & Beauty is the number one contract manufacturer in its sector in the UK.

The group uses the high returns on capital from its healthcare division to fund value-enhancing acquisitions and grow its market share, while benefitting from major tailwinds like demographics, increasing regulation, outsourcing by big brands and changing consumer tastes.

EXPANDING IN TECHNOLOGY

DCC Technology, which operates under the Exertis banner, supplies products from over 2,500 manufacturers to over 50,000 customers in retail and ecommerce as well as resellers and integrators.

It carries out product sourcing, website and category management, including localization and customization of products to different markets, and logistics, as well as stock hub and returns management.

Three years ago, DCC set itself the goal of increasing its presence in the US market while building a leading specialist international distribution business in technology and ‘lifestyle’ products.

To that end, $1 billion or 30% of the firm’s capital employed by region has been invested in North America since 2018. Further to this, in mid-December the group acquired Almo Corporation for an enterprise value (equity plus debt) of $610 million.

North America is the world’s largest B2B (business-to-business) and consumer technology market, and Almo is the largest player in the distribution of consumer appliance and lifestyle products.

The Almo deal takes DCC’s technology revenues to 27% of the group total and its North American revenues to 31% of the total, but the opportunities are still vast. The US technology and lifestyle market is worth $34 billion, and the firm sees scope for growth both in B2B and the consumer channel.

The acquisition will immediately increase the group’s earnings by 10% in the first full year of ownership and based on organic growth and synergies the group expects to achieve a return on capital from Almo of 15% within three years.

Analysts at Davy Research believe Almo is ‘a real competitive differentiator with its presence in Pro AV, consumer appliances and electronics and its sizeable e-commerce business. It also has strong margins and there are obvious synergies with Stampede and Jam, which were acquired in 2018.

UPSIDE FOR SHAREHOLDERS

The firm has a clear capital allocation policy in place now, which together with strong underlying cash flow and the introduction of new products and technologies is not only generating funds to reinvest in further growth opportunities but is funding a progressive dividend.

Even during the pandemic, the firm raised its dividend from 138p in the year to March 2019 to 145p in the year to March 2020 and impressively 160p in the year to last March, making for 27 years of unbroken growth.

Gearing is low in absolute terms and by historical standards at 0.4 times EBITDA (earnings before interest, tax, depreciation and amortization), and management believes it can deploy £6 billion on acquisitions without increasing its leverage.

With mid-single-digit underlying growth from its existing businesses and a similar contribution from the value-added deployment of capital the firm maintains it can continue growing earnings by double digits over the long term.

As we’ve said already, the shares aren’t expensive on an absolute or historic basis, and we applaud the more stringent capital allocation policy, but much depends on management’s ability to execute its growth strategy from here and we would be content to watch the firm’s progress over the course of the year before making a definitive call. This is definitely a story worth keeping tabs on for investors though.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.