Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFit and wealthy: six funds to whip portfolios into shape

Investing requires discipline and patience. Regularly putting money into investments can pay off in the long term, and it’s this habit which can help to build up wealth over time.

A lot of people have the willingness to put money into stocks, funds or bonds every month – they simply don’t know where to start in terms of picking the right products.

To give you a helping hand and put your investment journey onto the right path for the years ahead, Shares has pulled together various fund and investment trust ideas to suit different types of people.

Investors in their 20s, 30s, 40s and 50s probably want to grow the value of their investments as a priority, so the emphasis will be on capital gains rather than dividends.

Those in their early sixties may want to dial down risk, though they may also wish to stay invested in the markets to ensure their pension pot lasts for as long as they do. Those in retirement will also be looking for decent income solutions.

Read on to discover funds and investment trusts which Shares believes are suitable for each of these groups and risk appetites. Each person’s circumstances and risk appetites will be different, so these ideas may not suit everyone in each of the age categories. However, they should provide a good starting point for research.

20s/30s/40s/50s

Looking for growth, medium risk appetite

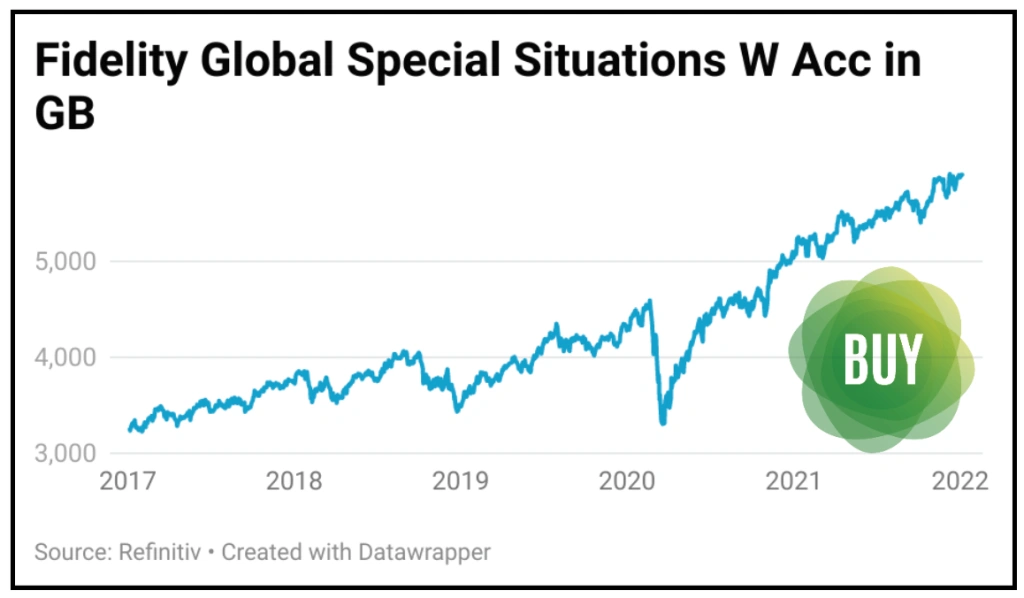

Fidelity Global Special Situations (B8HT715)

Most people when they think about saving or investing will be planning to build a pot for the future rather than drawing income or capital today.

The average person in their 20s or 30s has decades of work and salary earnings ahead of them so they have years over which to gradually accumulate meaningful savings. Even someone in their 40s or 50s will still be looking to grow their savings, so time is very much your friend.

The Fidelity Global Special Situations Fund (B8HT715) fund has several advantages for these people. It can take positions in less mature businesses where profits might be scarce, but the potential for faster growth is higher, implying bigger returns for investors in the future.

Take Amazon, for example, the fund’s third largest holding. It took six years from listing on the US stock market to make a profit, and lots of impatient investors would have given up and sold out before that happened. That would have been a huge mistake: $1,000 invested in Amazon shares 20 years ago would today be worth $298,018.

Fidelity Global Special Situations also targets companies that might have struggled for one reason or another but where, the fund believes, there is substantial scope to repair and improve performance. Japan’s Sony, also one of the fund’s top 10 stakes, is a great example, having rallied four-fold over the past five years.

At least 70% of the fund will be invested in stocks with ideas drawn from around the world, with about 55% in US markets currently, including names like Microsoft, Apple and United Health.

Performance speaks for itself. Over the past 10 years it has generated a 336.5% total return versus 247.2% from its benchmark, the MSCI All-Countries World index, according to FE Fundinfo. To put that another way, £1,000 invested in Fidelity Global Special Situations 10 years ago would today be worth £4,365 versus about £3,435 from an ETF that tracks the benchmark index. [SF]

Liontrust Global Innovation (B8DLY47)

Anyone with time on their side and who can let wealth accumulate before needing to draw an income from their investments should think about putting money into a fund which looks for the clever companies of tomorrow.

Liontrust Global Innovation (B8DLY47) has returned 52% since James Dowey and Storm Uru took over as managers on 1 July 2019, significantly ahead of the 38% from the MSCI All-Country World index, which is a popular benchmark for global stocks.

Dowey believes it is possible to make mid-teens returns each year from a portfolio of the most innovative companies. ‘If you can compound a portfolio of stocks at 15% a year, the portfolio becomes a 10-bagger in 16 years. History suggests it takes the broader market 25 years to do that,’ he adds. A 10-bagger is a term to describe an investment that increases in value by 10 times from its initial purchase price.

There are no guarantees that investors will achieve this return, and it is important to note that more speculative tech firms – some of which fall under the ‘innovation’ banner – are currently out of favour due to expectations for rising interest rates.

A lot of tech-themed companies trade on high valuations with the hope of large profit growth in the future rather than now, and these types of stocks are very sensitive to rising rates. With these types of companies, the market works out what a future stream of cash flow or earnings is worth today. Higher interest rates reduce the present value of the expected cash flow, so investors want to pay less for them. Investors taking a long-term view should be aware of this situation but mustn’t be put off completely by this headwind.

Dowey stresses that the Liontrust portfolio is not confined to the technology space as he and Uru look for innovators across all industry sectors. They don’t look at early-stage business and only invest when a company is worth more than $1 billion.

They look for businesses creating value, either by offering something that is cheaper or better than what’s currently available. These companies must have barriers to stop competitors copying them, management must have vision and good execution, and there must be evidence they are generating high returns from the money they spend.

Portfolio holdings include low-cost, no-frills gym operator Planet Fitness, flow measurement specialist Badger Meter, Sea which Dowey calls the South East Asia version of Amazon, and artificial intelligence-powered insurance group Lemonade. The ongoing charge on the fund is 0.88%. [DC]

Early 60s

Wants to stay invested in retirement but dial down risk

Bankers Investment Trust (BNKR) 124.4p

Bankers (BNKR) has two key ambitions which would make it a solid pick for someone approaching retirement (or in the early days of it) but still looking to capture some growth from the stock market.

It looks to achieve long-term capital gains better than those of the FTSE World index as well as annual dividend growth which is ahead of inflation.

The good news is it has largely achieved both these ambitions over the last 10 years with a total return (capital gains and dividends) of 313% against 231% for the FTSE World through that period. The company has increased its dividend for 54 consecutive years.

This consistency is underpinned by globally diversified investment remit and healthy revenue reserves which help to smooth out the impact of fluctuations in dividend payments from its holdings in individual years. It yields 1.75% which is a much better return that you’d find on cash savings.

The experienced Alex Crooke has been at the helm for nearly 20 years, taking charge in June 2003. He operates with no limits in terms of country or sector exposure and leans on specialists within the trust’s asset manager Janus Henderson, namely teams in the UK, North America, Europe, Japan and China.

The emphasis is on stock picking, identifying investments which are attractively valued with diversification intended to reduce the volatility of returns.

In total the trust has 175 holdings in the portfolio. Included in the top 10 are household names like Microsoft, Estee Lauder and Home Depot alongside less well-known firms such as financial software outfit Intuit and elevator manufacturer Otis Worldwide.

US-listed stocks account for more than 35% of the portfolio, but this is much less than a weighting of more than 64% in the FTSE World index.

Reflecting the impressive track record, the shares trade at a very modest premium to net asset value. The ongoing charge is a reasonable 0.5%, at the lower end of the peer group in the AIC Global sector. [TS]

RIT Capital (RCP) £27.25

An investment product which looks to preserve capital but still deliver growth is a decent choice for someone who wants to remain invested in retirement but also wants to start dialling down their risk exposure. RIT Capital (RCP) is the top performing UK investment trust with this remit.

The trust was founded by Lord Rothschild and manages a significant chunk of his family’s wealth. Combined the Rothschilds own more than 30% of the shares.

It is run by J. Rothschild Capital Management and Lord Rothschild also chaired the trust before stepping down in 2019. Being steered by an in-house team ensures a consistency of approach and commitment to the fund’s long-term and defensive approach to investing. The trust does make use of some exceptional third-party managers too and benefits from access to a network of some of the world’s top investors.

Its aim is to be diversified across different geographies and asset classes, including quoted and unquoted investments, to deliver strong returns with less volatility.

Since listing in 1988 RIT says it has participated in 73% of the upside in the market but only 38% of any market declines, and this has added up to an annualised total return of more than 11%.

Quoted shares represent a third of the portfolio; based on the latest reported data, top holdings included the likes of Alphabet, Walt Disney, Coca-Cola and T-Mobile.

The main downside is a relatively onerous ongoing charges figure of 1.55% according to the Association of Investment Companies, higher than its capital preservation trust peers, though this can be justified, at least in part, by its significantly better long-term performance. The shares trade at a small premium to net asset value. [TS]

60+

In retirement and wants income

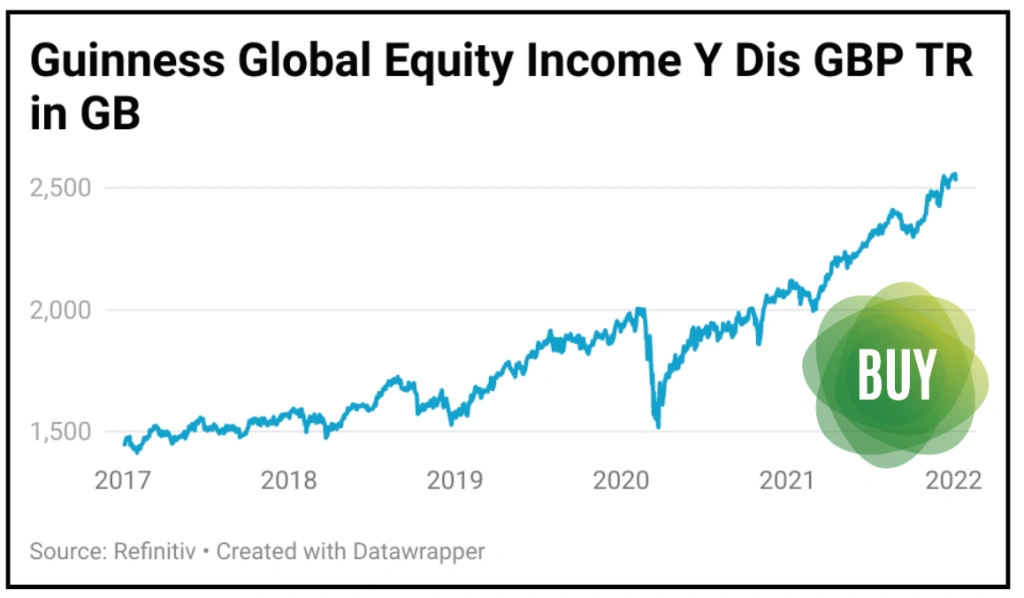

Guinness Global Equity Income (BVYPP13)

Guinness Global Equity Income (BVYPP13) might appeal to investors aged 65 years and over who have retired and want a growing income stream combined with some capital growth.

Managed by Ian Mortimer and Matthew Page, the fund is a one way to guard against the twin threats of equity market uncertainty and rising inflation given its focus on global equities with sustainable income growth.

Guinness Global Equity Income invests in companies that are well placed to be able to pay a sustainable dividend into the future, with a focus on profitable companies with strong balance sheets that have generated persistently high returns on capital over the last decade.

Starting with quality, not yield, their process identifies blue chip companies as well as some smaller companies that are outside of the traditional dividend paying regions and sectors.

The result is a concentrated, equally weighted portfolio of around 35 quality, attractively valued stocks offering a 2.4% yield with good potential for dividend growth. It has a 0.84% ongoing charge.

Since its 2010 launch, the fund’s focus on high quality and persistently profitable businesses, and a healthy balance between defensives and cyclicals, has generally meant performance has fared better during market downturns, while keeping up with rising markets.

Over the longer term, the fund has outperformed the IA Global Equity Income sector average over one, three, five and 10 years and since launch. For example, over 10 years it has generated a 235% total return versus 167% from the sector.

Top 10 holdings as of the end of November 2021 included technology group Microsoft, cigarettes seller British American Tobacco (BATS) and Marmite-to-Magnum ice cream maker Unilever (ULVR), as well as US-listed payroll services group Paychex and drug company AbbVie.

The fund also offers exposure to Taiwan Semiconductor Manufacturing, the globe’s biggest microchip maker; Medtronic, the world’s largest pure-play medical device manufacturer; as well as European industrial electrical equipment group ABB.

Investors considering this fund in retirement should note that equities are considered risky, and that performance could be volatile. Someone wanting a lower-risk option should instead look at a bond fund or even consider an annuity which pays a guaranteed income either for a fixed period or for life. [JC]

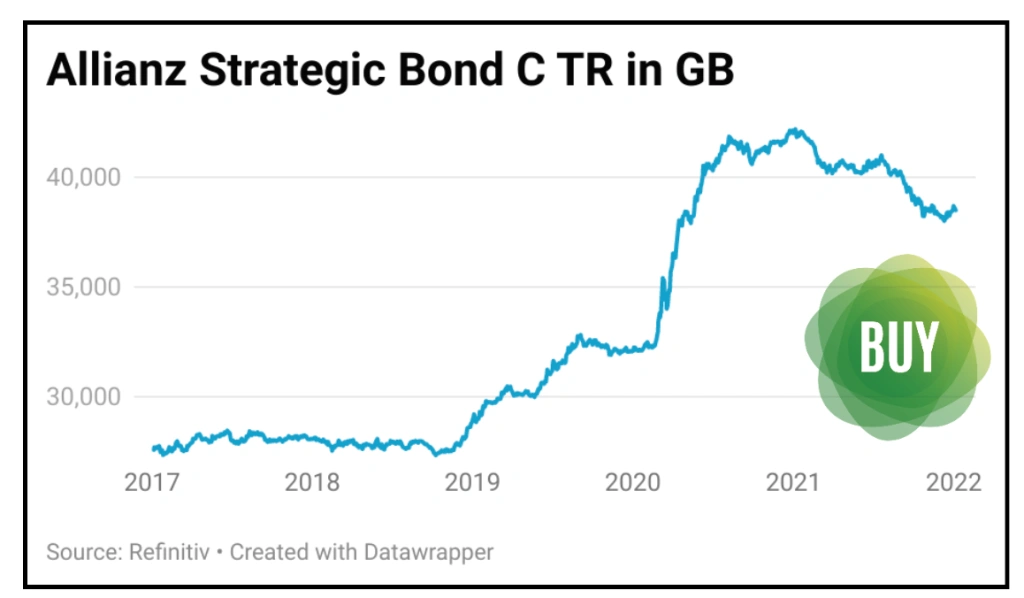

Allianz Strategic Bond Fund (B06T9362)

Investors who principally want income should consider the Allianz Strategic Bond Fund (B06T9362) which has a strong track record and is designed to provide safety during heightened stock market volatility. The fund has a trailing 12-month yield of 1.8% and income is paid twice yearly.

The £2.9 billion fund is lead managed by long tenured manager Mike Riddell and has an unconstrained mandate which allows it to invest across the whole fixed interest spectrum. This means the composition of the portfolio can differ significantly from its benchmark, the Bloomberg global aggregate bond market, hedged back to sterling.

The mandate gives Riddell the freedom to position the portfolio across parts of the global bond markets that he and his team find the most attractive, from corporate bonds, government bonds, emerging market bonds, inflation-linked bonds and currencies.

Allianz is the largest bond investor in Europe and one of the largest in the world, with deep resources and expertise.

The fund targets a low correlation to equities so that it behaves in a manner which protects investors when stock markets are volatile or weak, providing valuable diversification benefits. Correlation is a measure of the connectedness between things.

Over the last three years the fund has delivered a three-year annualised return of 10.3% a year, comfortably beating the 3.3% a year returned by the benchmark.

However, since the middle of July 2021 the fund has underperformed its benchmark which is principally down to Riddell’s negative view on UK inflation-linked bonds which has hurt returns.

Riddell believes the factors driving UK inflation-linked bond prices higher are technical in nature and he expects them to reverse during the second quarter of 2022. The fund has an annual ongoing charge of 0.63% a year. [MGam]

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.