Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThere are big obstacles to a Boohoo recovery

Investors in online fast fashion retailer Boohoo (BOO:AIM) could be forgiven for being pretty depressed when examining the share price chart.

The stock is languishing some 75% below the 420p peak reached in June 2020 as the pandemic drove young fashionistas online.

Boohoo has been hit by the continuing fall-out from a hugely damaging modern slavery scandal and more recently (16 Dec), a punishing profit warning.

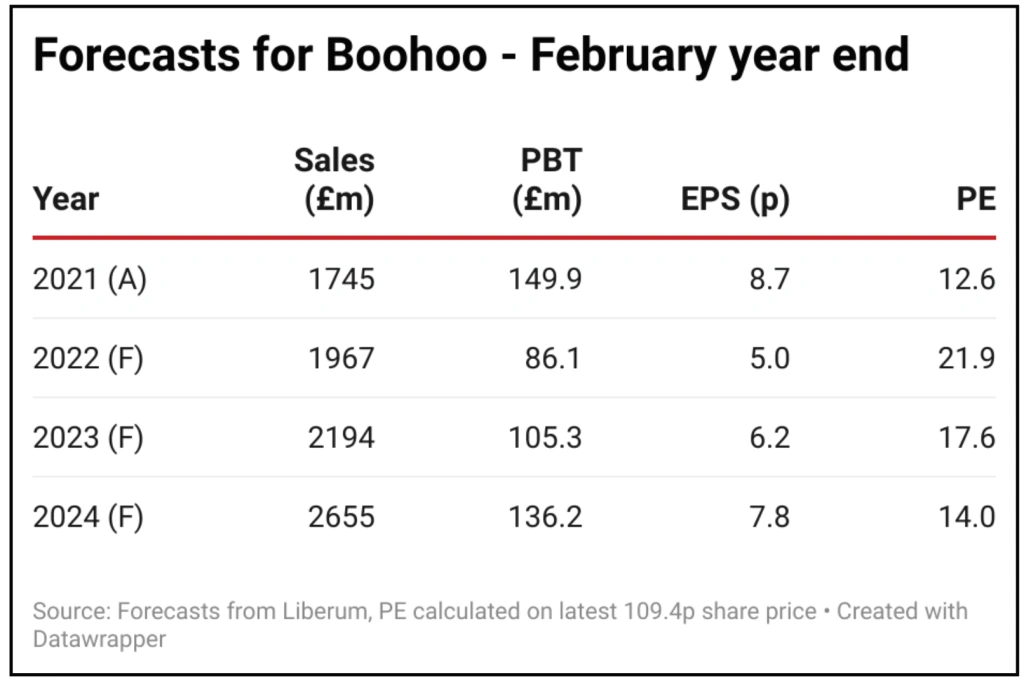

Based on downgraded estimates from Liberum Capital, Boohoo now trades on only 14 times forecast earnings for the year to February 2024, a massive discount to a June 2020 peak of 63 times. Despite this big discount we don’t think Boohoo is a buy.

WHY BOOHOO WARNED

Boohoo’s pre-Christmas alert had been partly expected by the market, as it followed supply chain-induced profit warnings from e-commerce companies including key rival ASOS (ASC:AIM) as well as the likes of AO World (AO.) and Gear4music (G4M:AIM) and the shares had weakened further in the run-up to the announcement.

Boohoo reported disappointing third quarter growth and warned profits for the year to February 2021 will be much lower than previously expected, blaming a spike in product returns rates and rising freight costs for a massive downgrade to annual sales growth and margin guidance.

On top of pandemic-linked costs, profitability has also been impacted by investments in acquired brands and the Debenhams platform; to recap, the Boohoo, PrettyLittleThing and Nasty Gal brands owner snapped up the Debenhams, Dorothy Perkins, Wallis and Burton brands at the beginning of 2021 and has relaunched Debenhams as a digital department store for fashion, beauty and homeware.

A comment that the Omicron variant could ‘pose further demand uncertainty and elevated returns rates particularly in January and February’ also rattled investors.

The upshot is Boohoo now expects to deliver sales growth of 12% to 14% this year, sharply below previous guidance of 20% to 25%.

The annual adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) margin is expected to be 6% to 7%, south of earlier guidance of 9% to 9.5% and implying adjusted EBITDA of between £117 million to £139 million for the year.

Shoppers returning more and more products is a particular issue for online-only retailers such as Boohoo and ASOS.

Whereas handling product returns through a brick and mortar shop is relatively simple, digital retailers work to thin profit margins that are supported by high turnover of stock, low costs and seamless logistics, meaning returns are a much bigger nuisance for them.

RISKS REMAIN

Jefferies cut its full year 2023 EBITDA forecast by 46% to £135 million and slashed its price target from 430p to just 165p on the warning: ‘While the extent and timing of reversion back to historical levels remains to be seen, we see clear logic in defining these factors as transitory rather than structural’, remarked the broker.

Liberum Capital is excited by the progress at Debenhams, which ‘offers a good opportunity for Boohoo to develop its beauty business and platform operations’. And while growth over the next 12 months is ‘likely to be muted and profitability will remain low’, Liberum expects a recovery after that and ‘a return to double digit profitability in the medium term’.

Nevertheless, the broker slashed earnings estimates for full years 2022, 2023 and 2024 on the grounds higher supply chain costs and Boohoo’s weakened delivery proposition will persist for the next 12-18 months.

Not only does Liberum envisage an ‘industry-wide permanent rebasing of supply chain costs at a higher level after the pandemic’, it also believes Boohoo will need to invest in marketing and cut prices to recover lost ground in the US and Rest of Europe regions, with its international deliveries being impacted by the pandemic.

Liberum estimates Boohoo’s EBITDA margin will remain below the 10% target ‘until full year 2027’, and flags that the increased rate of returns, with the product mix shifting back towards going-out wear including dresses, ‘brings in an added element of concern around product quality’.

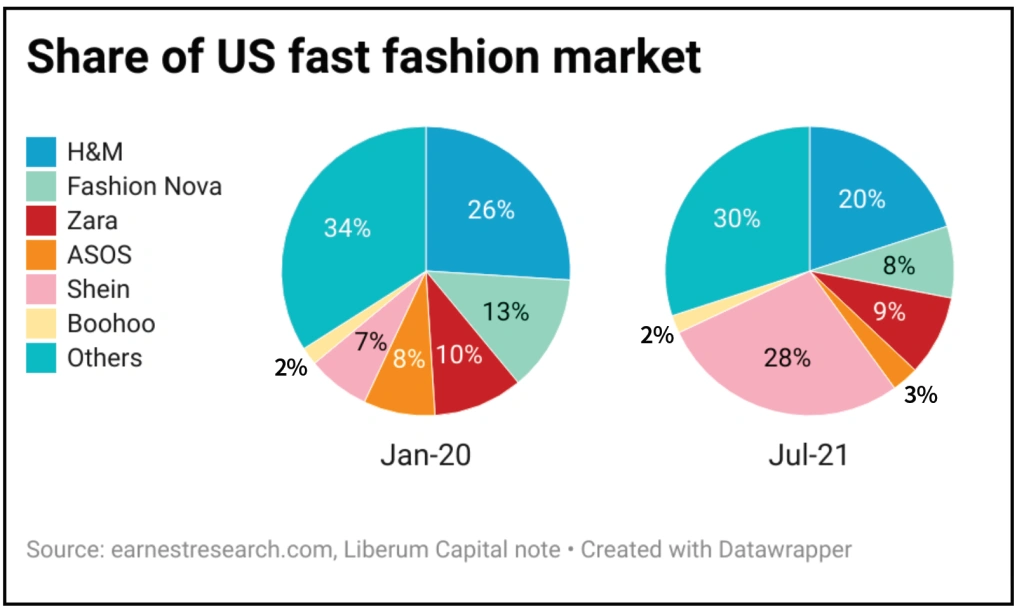

Boohoo’s weakened proposition in the US and European markets also means the retailer is likely to lose share to local players whose delivery proposition is maintained, such as Zara, Zalando, ASOS and About You in Europe and H&M, Zara, Forever21, fashionnova and Shein in the US.

RISE OF SHEIN

Worryingly for Boohoo, at a time when consumers are searching for bargains, Chinese ultra-fast fashion retailer Shein has taken over the US market during the pandemic and is emerging as a significant player here in the UK too.

Although Liberum stresses Shein’s ascent across the pond ‘may not be the worst thing for Boohoo in the long run’. The thesis is that Shein’s meteoric rise has accelerated the development of the US online fast fashion market and Boohoo can continue to ride that wave.

The work put in by Boohoo over the last 18 months to ensure strong compliance and transparency in its supply chain puts Boohoo ‘well-ahead of Shein, where there remains very little transparency on the practices and conditions of workers supplying the group’.

However, besides Shein, several other Chinese operators have entered the western fast fashion market, including Alibaba with Allylikes.com, though Liberum believes Boohoo’s ‘relatively stronger brand equity in the UK, as well as the greater penetration of online fast fashion before the rise of Shein, should insulate Boohoo in the UK more than in the US’.

Boohoo’s acquisition of more mid-market brands like Coast, Karen Millen and more recently, Debenhams, ‘makes its growth in the UK more defensible against Shein’, says Liberum.

STEER CLEAR FOR NOW

The success of Shein and Primark in the US demonstrates consumer appetite for keenly-priced fast fashion remains and once supply logjams clear, Boohoo’s proposition leaves it well-positioned for growth in this vast market.

Still popular with fast fashion savvy, digitally-minded millennials, Jefferies notes that Boohoo’s transition from a predominantly mono-brand, mostly UK business to a multi-brand, global fashion retailer has been ‘smoothly executed’.

The acquisitions of Karen Millen, Coast, Warehouse and Oasis, combined with the Arcadia brands Dorothy Perkins, Wallis and Burton, have opened up ‘new demographics, with supply chain enhancements underpinning long-term growth prospects’, argues the investment bank.

Boohoo has make progress in auditing its UK supply chain following 2020’s modern slavery shocker and outlined a sustainability strategy – it is adding more sustainable ranges across its brands – while in the wake of earnings downgrades, the shares trade at a massive discount to their historical average.

That said, the shares also looked cheap last year too, before overly-optimistic earnings forecasts were forced down and hammered a stock with a nosebleed rating that left no room for disappointment.

Shares suspects stock market sentiment towards interest rate sensitive growth stocks including online retailers will remain poor near term and there are myriad risks to consumer spending to consider too, all of which make us reticent to recommend Boohoo as a recovery trade.

Plus there is the risk that the whole concept of disposable fashion, while still popular for now, becomes more and more at odds with people’s increasing awareness and engagement around environmental issues, something which looks particularly likely for Boohoo’s largely younger target audience.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.