Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

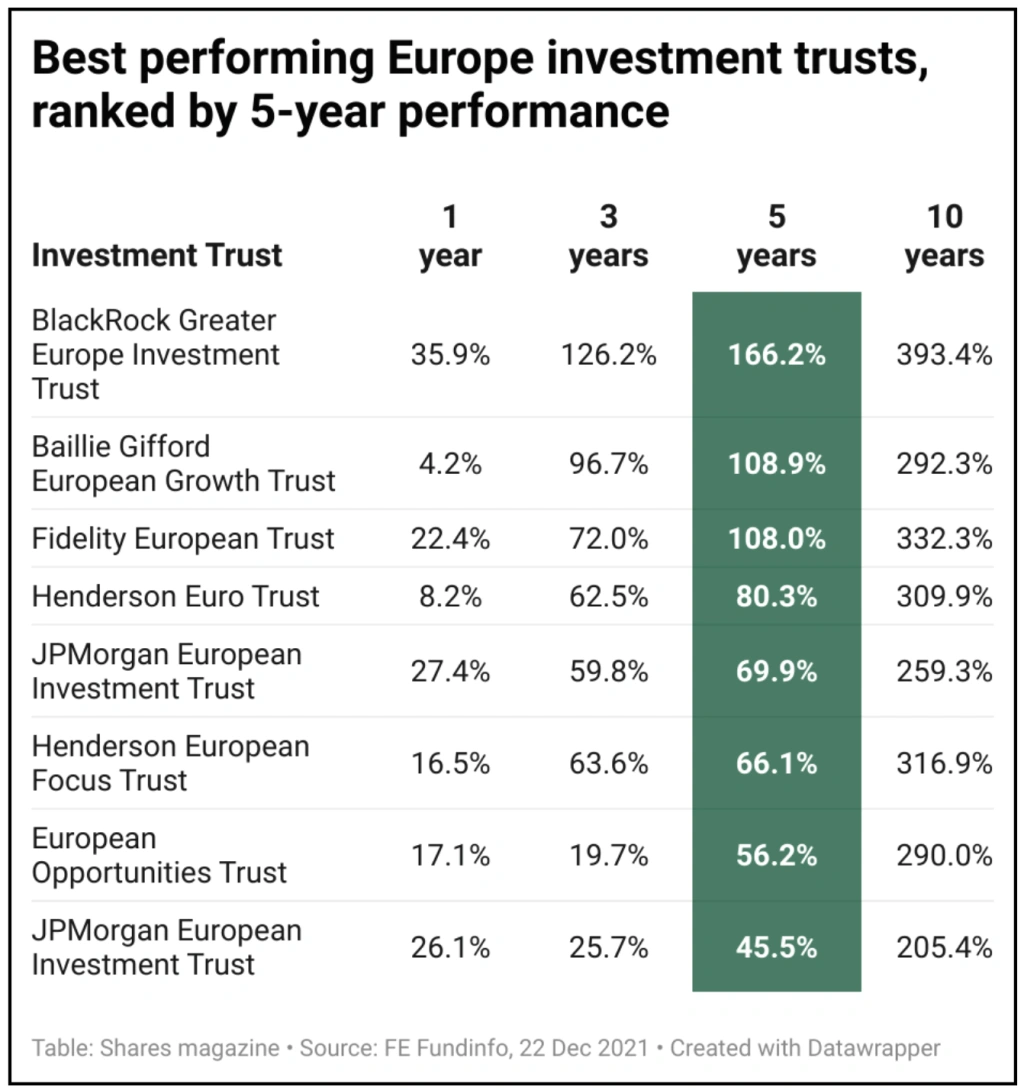

magazineThe top performing European funds and trusts

The performance of the top Europe (ex-UK) funds is proof that the European equity market offers a multitude of opportunities for active investors to acquire overlooked and undervalued growth companies.

The BlackRock Greater Europe Investment Trust (BRGE) is a £676 million fund with two co-managers. Stefan Gries covers developed European markets (90% of the portfolio); and Sam Vecht covers emerging European markets (10% of the portfolio).

Gries’ investment approach is to be ‘an investor in businesses not a trader in shares’. Shares are chosen on the basis of bottom up fundamental analysis. On a sector basis, the fund has consistent heavy exposures to technology, consumer discretionary, industrials and healthcare companies.

ASML which makes equipment to support chip manufacturers, is the largest position in the fund. Gries likes its high market share, pricing power and strong order book visibility.

BlackRock Greater Europe’s net asset value total returns rank first out of eight funds in the AIC Europe sector over the last one, three, five and 10 years, and have also outpaced the broader European stock market over these periods.

DIVERSIFIED APPROACH

The £542 million Ballie Gifford European Growth Trust (BGEU) aims to achieve long-term capital growth from a diversified portfolio of European equities.

The fund is co-managed by Stephen Paice and Moritz Sitte who invest in high quality, growth orientated companies with a strong competitive position. These businesses have a tendency to be managed by owner-operators.

A key point of differentiation is the fund’s ability to invest in private companies, although its current 4.5% weighting to non-public investments is relatively modest.

The portfolio is relatively concentrated with between 30 and 60 listed and private companies. Paice and Sitte are big advocates of asset light digital platforms that benefit from network effects (a process whereby increased numbers of people or participants improve the value of a good or service).

Adyen, a Dutch company which is disrupting the traditional payments industry is a good example of this, and represents the second largest holding in the fund.

Adyen makes it possible for companies such as Uber, Spotify and Netflix to accept payment from consumers around the world, using a variety of different payment methods. This enables companies to scale quickly, which previously was not possible.

In marked contrast to its competitors, Adyen has built its technology from scratch which confers a powerful competitive advantage.

MID CAP FOCUS

The Premier Miton European Opportunities Fund (BZ2K2M8) is a £2.39 billion fund investing in European companies with a mid-cap bias. Fund managers Carlos Moreno and Thomas Brown look for companies with high and accelerating sales growth.

This can be from new products, market share gains, new markets or pricing power. They demand a high rate of return on capital, and evidence that this will be sustained over the long term.

Moreno and Brown believe that stock markets are poor at understanding long term change. As a result, they adopt a bottom up stock picking approach over the long term, being five years or more.

‘This means traipsing around Europe on EasyJet flights looking for businesses you think are going to be a lot bigger in the future’.

Swiss industrial manufacturer Interoll is a significant holding in the fund. It supplies products including rollers, conveyors and pallet flow solutions for courier and postal services.

Clients include Coca-Cola and Amazon. Moreno believes ‘Interoll is a brilliant play on the movement of small packages’.

HIGH QUALITY GROWTH

The objective of Comgest Growth ex-UK (BQ1YBM1) is to create a portfolio consisting of high-quality growth companies. The fund is aimed at investors with a long-term investment horizon.

Comgest fund manager Alistair Wittet explains ‘we like sectors with defensive growth characteristics and healthcare is an excellent example of this’.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.