Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePlay the rotation into value stocks with Temple Bar

January has seen a rotation in the market, with investors moving out of technology-related stocks and into more value style investments where the story is all about slow to medium growth today, not super levels of growth in the future.

The UK market has quite a few stocks that fall under the value category – namely immediate profit and cash flow, or ‘jam today’, trading on undemanding ratings versus the ‘jam tomorrow’ of many more speculative tech stocks.

The fact investors are looking at the value space again bodes well for Temple Bar Investment Trust (TMPL) as it specialises in investing in value-style stocks.

ROTATION REASONS

Tech stocks have fallen out favour with investors due to expectations for rising interest rates. A lot of tech companies trade on high valuations with the hope of large profit growth in the future rather than now, and these types of stocks are very sensitive to rising rates.

The market works out what a future stream of cash flow or earnings is worth today and bond yield and interest rate expectations play a key role in this calculation.

Higher interest rates reduce the present value of the expected cash flow, so investors don’t want to pay as much for tech-related stocks. That’s why you have seen movements such as a 15% fall in Tesla and a 13% decline in investment trust Allianz Technology (ATT) so far this year.

NEW MANAGER

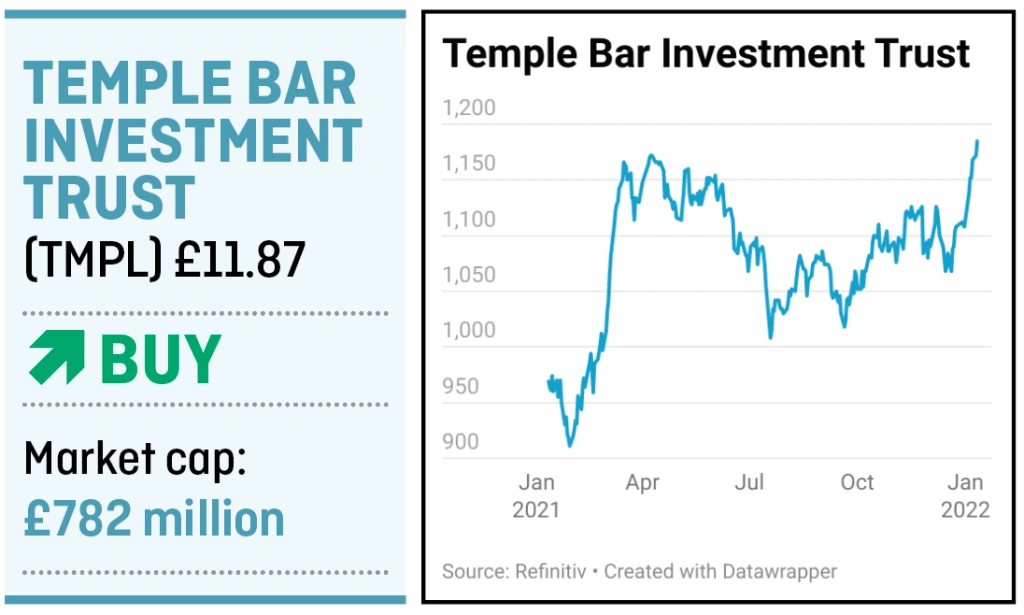

Temple Bar Investment Trust saw a change in manager just over a year ago, coinciding with another rally in value stocks. Its shares hitched a ride with this rally until June 2021 when the market started to switch back to favouring higher growth-orientated stocks, leaving the trust’s share price to lose momentum.

However, Temple Bar’s shares perked up in late 2021 when expectations increased for interest rate hikes, together with a resurgence in Covid cases. Investors started to seek safety in seemingly more boring companies and that trend has accelerated in 2022.

Not only is Temple Bar’s style back in favour, but investors are able to access its portfolio for less than the market value of the underlying holdings. That’s because its shares continue to trade at a discount to net asset value, the latest being 7.9% versus a 12-month average of 6.8% according to Winterflood.

One possible explanation behind the lingering discount to NAV is that value as a style has been out of favour for much of the past decade and so the market might think the current rotation won’t last long. That’s a risk for prospective investors to consider.

INVESTMENT PROCESS

Temple Bar is managed by RWC and the goal is to provide a greater total return (share price gains and dividends) than the FTSE All-Share index.

RWC considers a company’s growth prospects and sustainable levels for profit margins and then calculates an intrinsic value for the business. It looks to invest when the shares trade below this intrinsic value.

A lot of companies are cheap for a reason and RWC is keen to avoid so-called ‘value traps’ where the businesses could stay cheap for a long time because of structural issues.

Instead, it looks for companies on cheap ratings which have a strong enough balance sheet to survive any short-term problems.

‘The value opportunity arises because investors have an irrational dislike of a business, or misunderstand it, or are too focused on short-term problems, for example,’ explains QuotedData, an investment trust research specialist.

QuotedData says that just as some investors become over-exuberant about some stocks, they become overly pessimistic about others, which creates value opportunities. The challenge is sifting through the pack and seeing which ones can bounce back.

The investment trust’s portfolio has large positions in energy, materials and financials – all sectors which tend to do well when the value investment style comes into fashion.

PORTFOLIO HOLDINGS

Oil and gas companies Royal Dutch Shell (RDSB), BP (BP.) and Paris-listed TotalEnergies are among the biggest holdings in the Temple Bar portfolio. These companies generate lots of cash, which is used to reduce debt, fund dividends and share buybacks, and help finance expansion into renewable energy.

Life insurance provider Aviva (AV.) is a top 10 holding for Temple Bar. James Pearse, an analyst at investment bank Jefferies, believes that following the recent disposals of Aviva’s non-core overseas businesses, it has enough surplus capital to return £5 billion to investors this year. One might expect this money to be split between special dividends and share buybacks.

Temple Bar also has a stake in media group WPP (WPP) which last year benefited from a recovery in advertising spend. Trading on 13.5 times forecast earnings for 2022, WPP’s valuation is ‘extremely modest for a well-managed, market-leading, global player experiencing robust trading and offering the prospect of strong medium-term growth and cash generation,’ says broker Shore Capital.

‘We also note that, based on consensus forecasts, it is trading on an EV/EBITDA discount to its international peers despite offering the prospect of superior earnings growth. Our fair value estimate is currently £16.24 suggesting substantial upside potential (from the current £11.69 trading price).’

Other holdings in the Temple Bar portfolio include Vodafone (VOD), Marks & Spencer (MKS) and Royal Mail (RMG).

The trust targeted a minimum of 39p in dividends for the 2021 financial year, with three quarterly payments of 9.75p having already been paid. While we expect dividend growth from the trust in the future, for now investors should use guidance for 2021’s payment as an indication of how much income the stock could provide in 2022, namely a yield in the region of 3.3%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.