Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFRP Advisory poised to benefit from wave of insolvencies

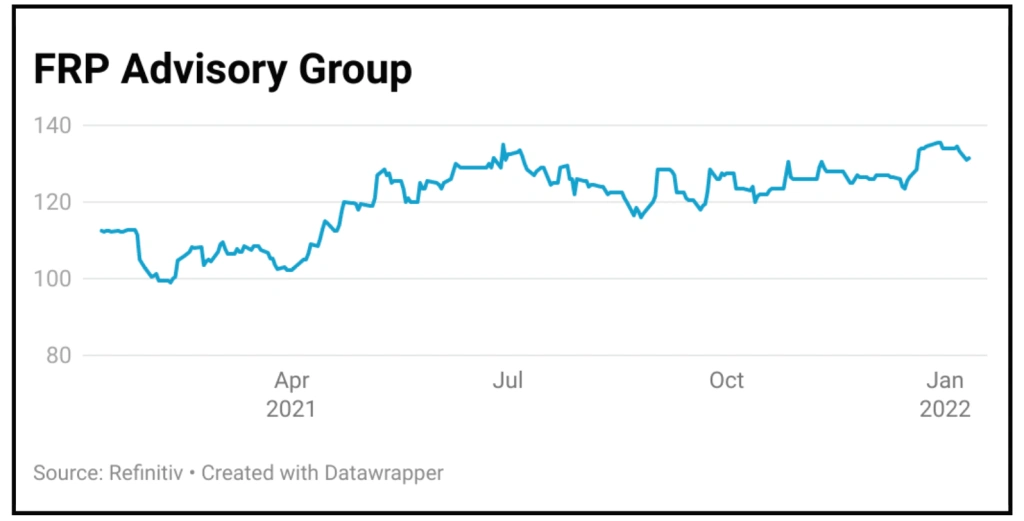

FRP Advisory (FRP:AIM) 132.3p

Gain to date: 8.4%

Original entry point: Buy at 122p, 16 September 2021

Since recommending specialist advisor FRP Advisory Group (FRP:AIM) in mid-September 2021 the shares have risen by a little more than 8%. We continue to believe that the shares offer good value and maintain our positive stance.

Results (16 Dec) covering the six months to 31 October 2020, saw the group deliver another period of impressive growth with revenue increasing by 14% and underlying adjusted earnings before tax depreciation and amortisation ahead by 7%. Significantly this was despite 2020 being a subdued period for the insolvency market.

Several factors have contributed to the placid nature of the insolvency business. These include the furlough scheme, state-backed initiatives including the bounce back loan schemes, and a slower (when open at all) court system.

However with government stimulus now unwinding and UK businesses increasingly facing a challenging macroeconomic environment FRP is well positioned to benefit from a surge in activity. Altradius, a trade credit insurer has predicted insolvencies will be 33% higher in 2022 than in 2019.

The star performer within FRP has been the corporate finance division. The business is starting to reap the benefits of the Spectrum and JDC acquisitions both secured at attractive multiples. Critically these have added increased scale and scope to FRP’s corporate finance offering.

At the beginning of March 2021 FRP acquired Spectrum Corporate Finance for £9.4 million, extended its geographical footprint into London and the South with the addition of 27 new employees.

The Spectrum deal was followed in September 2020 with the £5.3 million acquisition of JDC Group, the leading specialist corporate finance and forensic services firm. The deal provides FRP with an immediate presence in the East of England and bolsters FRP’s corporate finance and forensic services offering.

A vibrant deals market coupled with pent up demand to deploy capital has created an ideal market for FRP’s corporate finance team.

Total take private deals, based on value are at the highest value for the last 20 years, which bodes well for the recently acquired JDC and Spectrum teams. This chimes with official guidance that corporate finance have a ‘strong’ pipeline for the second half of the year.

Broker Liberum suggest that corporate finance will contribute 15-20% of group revenue in 2022, validating the view that FRP is more than a play on a downturn in the economy.

The most recent estimates from house broker Cenkos have FRP trading on a prospective price to earnings ratio of 18.3 times. Given the potential growth prospects in both the insolvency and corporate finance divisions they argue ‘the shares fail to reflect the upside potential’.

SHARES SAYS: Still a buy.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.