Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRising bond yields start to weigh on popular stocks

US technology stocks sold off on 22 February following a period of mounting concern about inflation, reflected in rising yields on government debt, and the implications for interest rates. This had a knock-on impact for UK-related tech stocks and funds including a big decline in Scottish Mortgage Investment Trust (SMT).

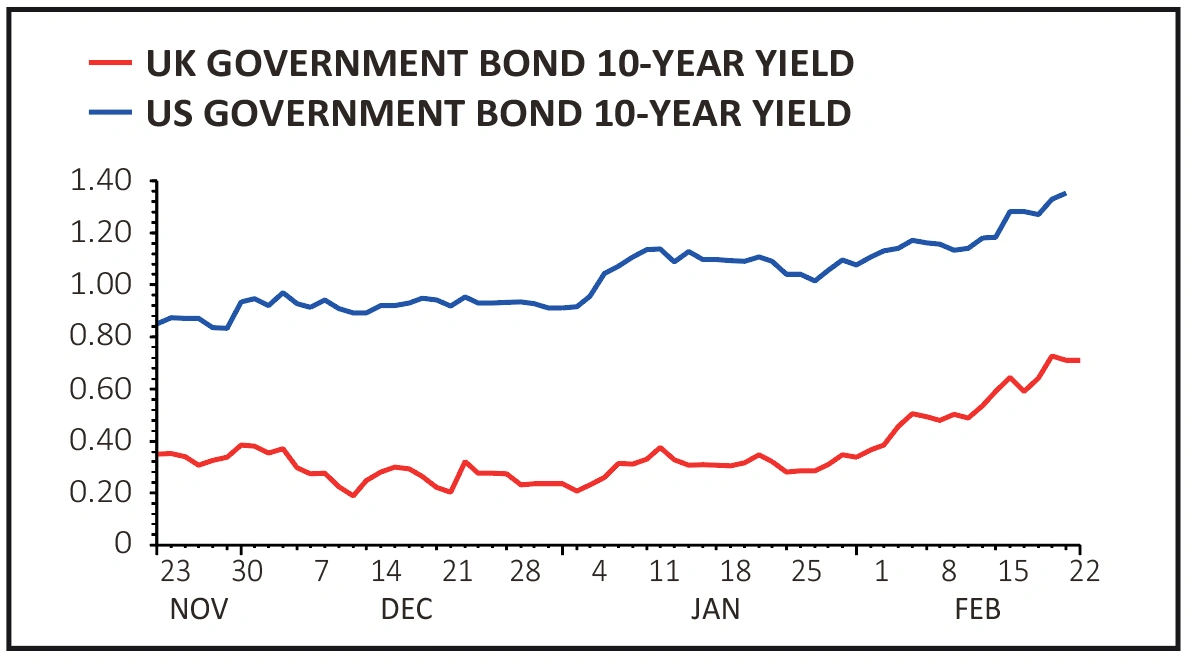

In the UK 10-year government bond (gilt) yields have gone from 0.2% at the start of the year to 0.7%. The US 10-year Treasury yield has surged above 1% for the first time since the pandemic to now trade at 1.36%.

WHY RATES MATTER TO INVESTORS

Government bond rates matter because they are used as a cost of capital or the risk-free rate by investors to calculate fair values for stocks.

Everything else being equal, higher rates make stocks less attractive.

Until recently, investors have broadly welcomed higher rates as confirmation that economies will rebound strongly later this year.

Consequently, companies are expected to generate better than average earnings growth. According to investment bank Société Generale analysts expect global earnings to surge by 30%

this year.

The prospect of higher earnings growth has driven demand for so-called value shares and away from growth shares, because the value stocks are considered more cyclical and have better earnings growth potential in an economic rebound.

In addition, higher interest rates penalise the theoretical valuation of longer duration stable growth companies (such as tech names) more than shorter duration cyclical companies.

Many analysts and strategists view higher rates as part of a normal economic recovery and helpful for stocks and especially cyclical shares.

US investment bank Bank of America says: ‘Rising bond yields should support value versus growth, banks and insurance, while weighing on pharma and utilities.’

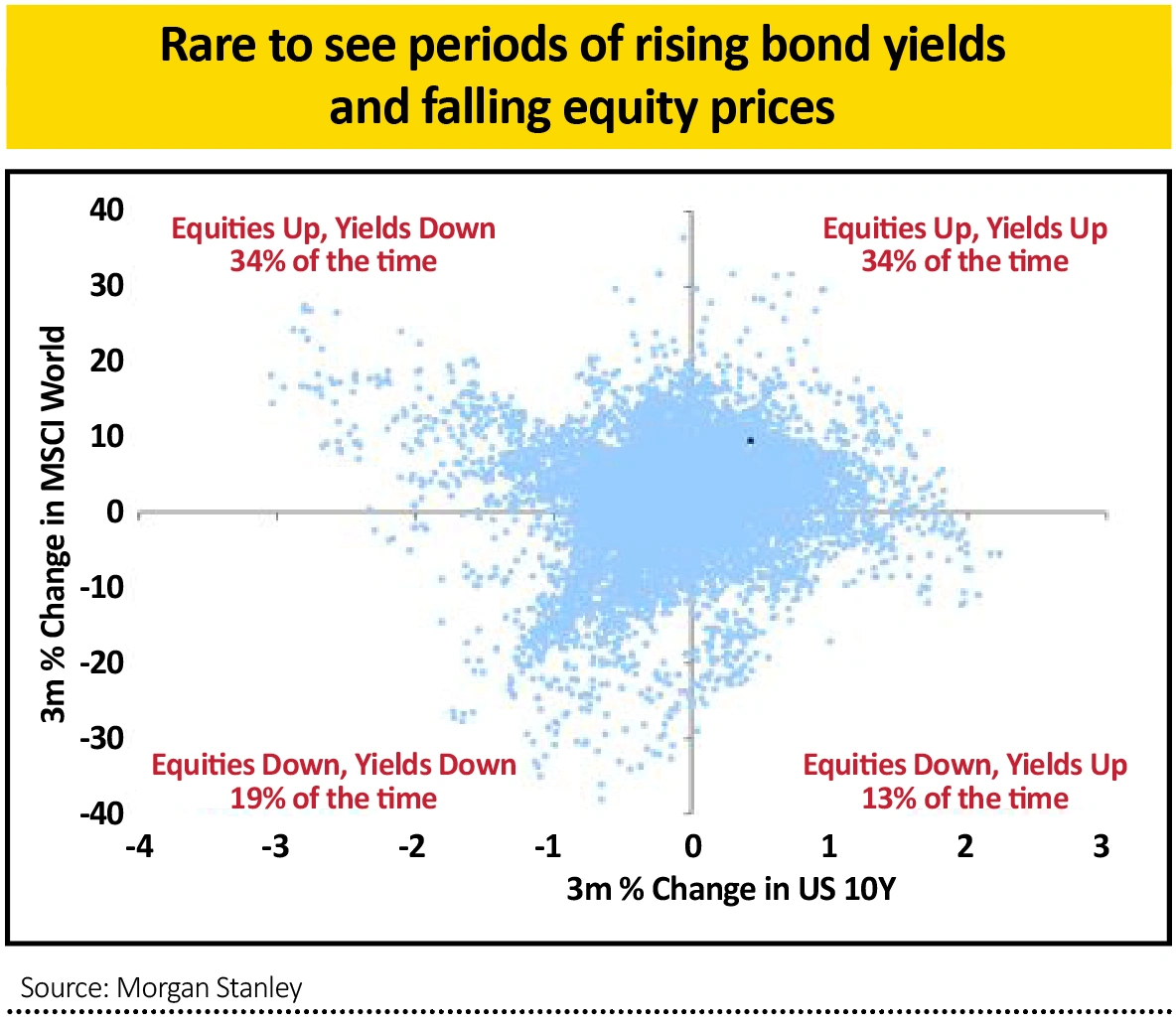

Morgan Stanley argues that it’s not unusual for interest rates and equities to rise at the same time, pointing out that over the last 40 years it has been relatively rare to see periods of rising bond yields and falling equity prices.

John Paulsen, chief strategist at research house Leuthold agrees, and points out that since 1900 whenever rising bond yields stayed below 3%, stocks have thrived.

Government bond yields in the US and UK are certainly nowhere near the 3% level at present.

IS THE MARKET TOO RELAXED ABOUT INFLATION?

The reflation narrative and assumption that central banks will keep a lid on interest rates for longer, regardless of higher inflation, has arguably become the consensus view and priced into markets.

For example, the latest Bank of America fund manager survey showed cash levels had been whittled down to eight-year lows while allocations to commodities were at their highest since 2011.

In other words, investors have already gone ‘all-in’, spurred on by accommodative central bank policies.

Investment bank ING’s comments on inflation illustrate the consensus view very well. It says: ‘We are all aware the run rate of monthly inflation numbers has picked up a bit, no one really expects inflation to push up and stay at levels that will require central bank tightening anytime soon, especially not the Fed (US Federal Reserve) or the ECB (European Central Bank)’.

But with the US $1.9 trillion fiscal stimulus likely to be voted through in March and a strong rebound in economic activity already baked in, some observers see the prospect of pent-up consumer spending as potentially worrisome for markets.

One such observer is Chetan Ahya, chief economist at Morgan Stanley, who believes that US policy makers have been very generous supporting households and businesses.

SPENDING SPREE AHEAD?

In aggregate, US households will have around $2 trillion of excess savings assuming the latest package is passed and Ahya argues that consumers are only holding onto savings because their spending options have been limited.

Pent-up demand could lead to a splurge in spending once economies fully open, paving the way for a ‘regime shift’ towards higher inflation.

The risk of higher inflation is heightened by the huge national debts that have been built up to deal with the economic damage inflicted by the pandemic. This may crimp central banks’ policy response should inflation overshoot, allowing inflationary pressure to get out of control.

It’s noteworthy that more institutional investors have added inflation protection strategies to their armoury including the controversial gold alternative, bitcoin.

UK fund manager Ruffer is backing cryptocurrency bitcoin, believing it is only in the early stages of being adopted as a mainstream asset. The firm has since seen a return on investment of up to £693 million after the currency surged to record highs above $50,000.

ANOTHER ISSUE TO CONSIDER

Finally, there is some debate about the common wisdom that higher inflation is good for equities and bad for bonds.

Companies need to replace assets over time and if inflation drives prices of plant and machinery higher, then historical profits and returns on capital are overstated, leading to theoretically lower valuations for shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.