Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTarget Healthcare continues to be a dependable source of income

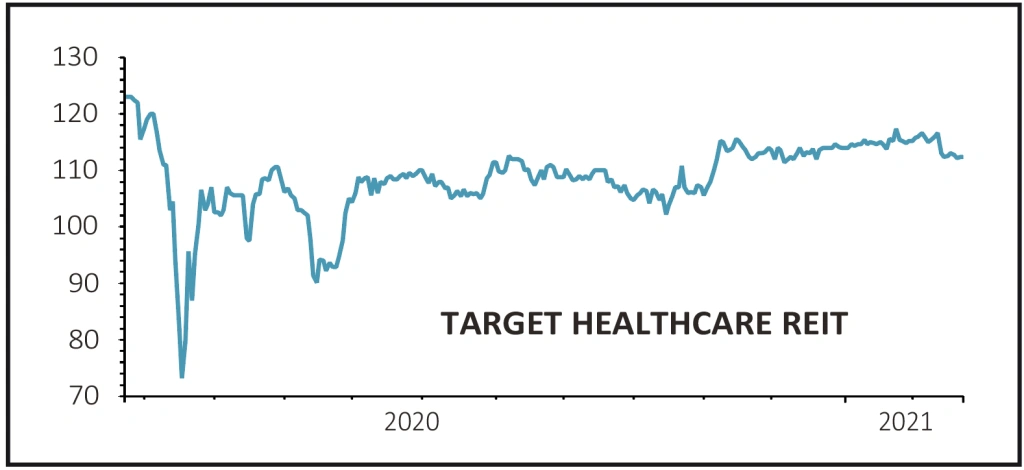

Target Healthcare REIT (THRL) 112.4p

Gain to date: 5.2%

Original entry point: Buy at 106.8p, 16 July 2020

Care home investor Target Healthcare REIT (THRL) may not have knocked the lights out in terms of share price performance since we flagged it in July 2020 but the steady gains in the interim look a decent outcome given the pressures on the sector from Covid-19.

The REIT has remained a reliable source of income through the period, maintaining its progressive dividend policy.

As chief executive Kenneth MacKenzie tells Shares, the pandemic has made the case for its focus on purpose-built facilities with en-suite wet rooms given the increasing importance of infection control.

With vaccinations happening across care homes the level of enquiries across its portfolio is ramping up, which should help rebuild occupancy levels.

In this context Target recently announced plans to raise £50 million to invest in a pipeline of £224 million worth of existing assets and development opportunities.

MacKenzie says the expansion plans will help boost the number of tenants and thereby diversify the risk on its income stream.

SHARES SAYS: The shares continue to offer a highly attractive 6% yield and are well placed in a space which benefits from structural growth drivers.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.