Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBanks signal return to dividends but outlook remains cloudy

The UK’s four major high-street lenders posted results for the year to December which beat forecasts one way or another, and all flagged a return to dividends in line with regulatory guidance, but there was little to cheer regarding the longer term.

After barring the banks from paying dividends last March in order to ensure they remained well capitalized, the Prudential Regulatory Authority (PRA) eased the rules on shareholder pay-outs and share buybacks in December and the banks went about as far on capital returns as they could within the constraints set out by the PRA.

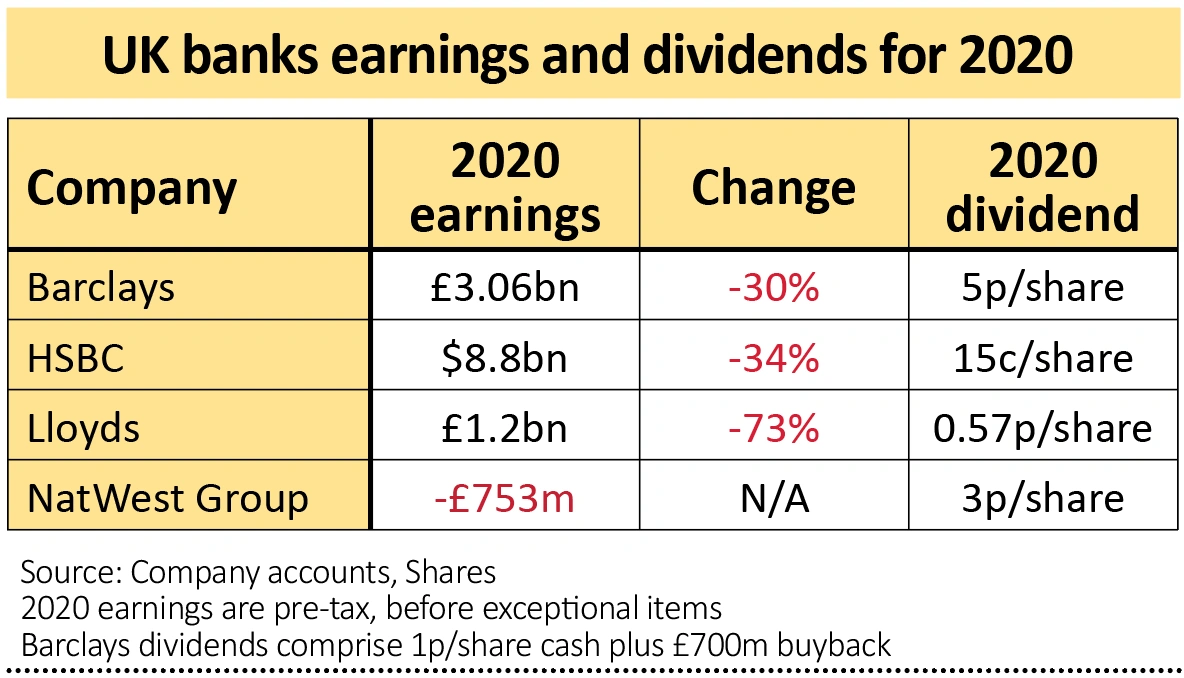

Lloyds (LLOY), the UK’s biggest mortgage lender, posted a 73% drop in full year pre-tax profits, slightly better than market forecasts, and said it would pay a dividend of 0.57p per share, the maximum allowed by the regulator given its capital ratios.

The bank set itself new targets for costs and returns on tangible equity, while also saying it aimed to resume a ‘progressive and sustainable’ dividend policy.

However, it admitted that its financial performance is ‘inextricably linked to the health of the UK economy’ and that ‘significant uncertainties remain’ over the spread of the virus, the speed and efficacy of the vaccination programme and the pace of economic recovery.

Barclays (BARC) delivered pre-tax profit 50% ahead of market forecasts thanks to a record contribution from its investment banking business, which continues to gain market share even against its Wall Street rivals.

With a capital ratio of 15.1%, the bank announced a 1p per share dividend and a £700 million share buyback, meaning a total shareholder return of 5p per share. However, talk of ‘headwinds’ persisting in the medium term sent the shares lower.

NatWest (NWG) fared better, its shares rising despite the group posting a hefty loss for 2020 due to the lack of investment banking income to offset the squeeze on lending margins.

Instead, lower provisions for bad loans and a rise in mortgage lending meant it finished the year with a capital ratio of 18.5%, higher than most of its UK and European peers. The company also announced plans to exit its Irish operations.

Recently appointed chief executive Alison Rose vowed to distribute a minimum of £800 million of surplus capital per year from 2021 to 2023 through a mix of ordinary and special dividends, but again references to ‘uncertainty’ in the short and medium term saw the share price ultimately drift lower in the wake of the numbers.

The UK’s largest bank by market value, HSBC (HSBA), recorded a 34% drop in full year profit due to lower revenue and a substantial hike in provisions for potential credit losses as it firmed up plans to focus on Asia for future growth.

The firm committed itself to a 15c interim dividend, substantially below 2019’s payment of 50c per share, and cancelled the option of

scrip dividends.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.