Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAnalysing Gym Group's investment credentials

We are approaching the culmination of our long-running First Time Investor series.

While we have used practical examples throughout to help illustrate our guide to investing and the markets, in these final parts we go a step further and apply everything we’ve discussed to the analysis of an individual stock which we believe is also a highly attractive investment for the long run.

We have chosen to look at low-cost gym operator The Gym Group (GYM:AIM). As of February 2021 its shares have been clobbered by the lockdowns necessitated by the coronavirus pandemic and still trade around 35% below their 2018 peak.

As we have stressed through-out the series investing is a long- term endeavour and we adopt that mindset in the following analysis. We simply want to find out why Gym could be a potentially rewarding long-term investment.

We use a familiar framework and start by posing three fundamental questions; does Gym have a durable business; can its earnings and cash flow grow faster than the market; how likely is it that the share price will grow in line with profits?

In other words, how much could an investor make if profits rise as expected.

DOES GYM GROUP HAVE A DURABLE BUSINESS?

Increased wealth and a desire to be more active in old age has been a key driver for the health and fitness sector, leading to structural growth over many years.

It is unlikely the pandemic has changed this basic human activity in a fundamental way. In fact, the pandemic may have helped to cement the relationship between exercise and mental wellbeing.

After all, during lockdown daily exercise has become one of the few legitimate reasons for leaving the house.

When Gym reopened sites after the first lockdown in July 2020, it reported good levels of demand from existing and new customers.

The economic damage caused by the pandemic has increased the number of available sites in attractive locations, fostering growth and improving the future quality of Gym’s estate.

INCREASING PENETRATION OF LOW-COST GYMS

UK health club membership has grown by a third over the last 12 years and now represents around 16% of the UK population supporting revenue just under £5 billion.

Gym Group operates in the low-cost segment which has seen the fastest growth within the wider health and fitness market.

According to a study by consultancy PwC, commissioned by Gym Group, low-cost gyms have become a clear category winner over the last decade, taking market share from around 3% in 2012 to more than 12%.

In terms of memberships, the share is greater with low cost membership growing from 2% of the total market to over 25%, demonstrating their disruptive impact on the gym market.

Further penetration in the UK has plenty of headroom, argues PwC, noting the 10 largest brands only represent 16% of the market compared with 68% in Germany.

The report estimates that the number of low-cost gyms could double over the next five years.

Gym had a market share of 24.6% as reported at 30 June 2020 and has consistently grown its share of the pie.

IS GROWTH PROFITABLE/HOW DOES GYM GROUP COMPETE?

As we have said before, the only growth investors should be interested in is profitable growth. So, the first question that comes to mind is how do low-cost gyms manage to make an economic return for their investors when they offer such low prices?

Low cost is defined as under £25 outside London and £30 inside the capital. On average Gym generates £18.5 of revenue per month per customer across the estate with no contracts. Traditional gyms can cost anything from £40 per month upwards.

Gym’s major advantage is its low labour intensity and high asset efficiency. For example, the company operates with just one or two staff for each of its 184 sites and has built strong technology solutions to make a visit to the gym easier and more fun.

Gym doesn’t provide any wet facilities, which means, no swimming pools, saunas or steam rooms. There aren’t social areas or coffee machines which means that the company achieves higher revenue density and improved efficiencies.

Adding further to efficiencies compared with traditional gyms, its customers can use the facilities 24/7 which opens the gyms to a wider segment of society. For example, shift workers, taxi drivers and general participants in the ‘gig’ economy.

The company is very innovative in finding ways to improve the customer experience. During summer 2020 it launched an app which showed how busy their gyms were at any time of the day or night which allowed its customers to use their time more effectively.

This innovation increased App usage by 114% compared with pre-pandemic levels.

It seems reasonable to conclude that the factors driving the company’s growth and market share gains are sustainable. Gym is the lowest price operator within the sector.

As the business grows and scales up further there is scope to increase it price advantage without impacting profitability, creating a virtuous circle.

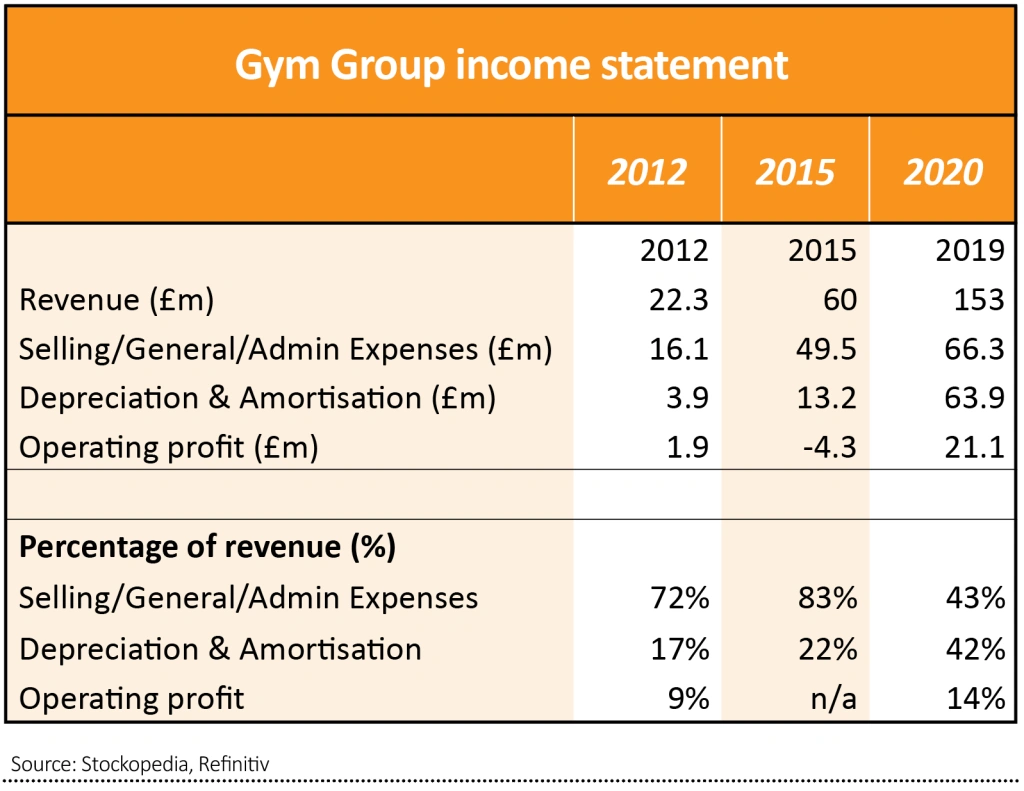

GYM’S INCOME STATEMENT

The reported numbers don’t reflect the underlying profitability of the business because all the largely fixed costs associated with building and fitting out sites have been recognised before they have reached sales maturity.

As the table illustrates revenue has grown quickly, from £22 million in 2012 to £153 million in 2019 which is a compound annual growth rate (CAGR) of 32% a year.

The distortion to reported profit is illustrated by the depreciation and amortisation charges which have increased to 64% of revenues from 4% in 2012. These charges reflect wear and tear on gym equipment and fixtures and fittings as well as two acquisitions.

To get a clearer picture of underlying profits, an adjustment needs to be made to depreciation charges so that only maintenance costs are used rather than the full charge.

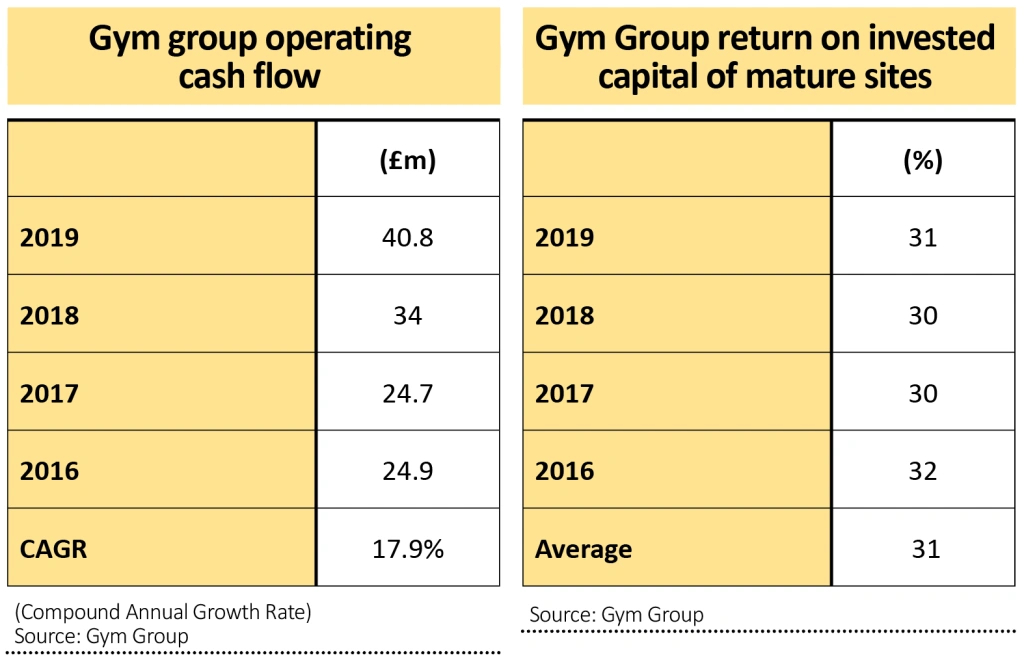

In the key performance indicators (KPI) section of the website, Gym lays out the calculation for investors. It refers to this metric as group operating cash flow (OCF).

It represents EBITDA (earnings before interest, taxes, depreciation and amortisation) minus maintenance depreciation and working capital expenses.

The company has grown OCF by 64% over the last three years equivalent to a CAGR of 17.8% a year. The ‘steady state’ profit represents a healthy profit margin of 26.7% of revenue, compared with the 14% reported operating margin.

As utilisation of sites increases revenue will grow without the associated costs and reported margins should rise.

Gym Group provides return on capital measures for mature sites which show they have consistently achieved 30%-to-32% returns over the last four years. The measurement is adjusted EBITDA divided by the total capital initially invested in the sites.

This is a very high return and supports the company’s strategy to prioritise investing in its estate and further grow its share of the market. Gym doesn’t pay dividends.

As we have pointed out before management’s capital allocation decisions are an important factor in driving shareholder value.

Next week will uncover how Gym finances its business by examining the balance sheet. We will also look at the valuation, analysts’ growth expectations, who owns the company and some plausible scenarios for future shareholder returns.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.