Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBuy Marshalls as Britain builds for recovery

The rebound in specialist building products firm Marshalls (MSLH) share price from its March 2020 lows has stalled and it is currently underperforming the wider building materials space. We see that as an opportunity.

The lack of share price action may reflect the fact it has a higher valuation relative to peers, but we think a premium is more than warranted by the quality on offer. Buy ahead of full-year results on 11 March which should signal a strong recovery in 2021.

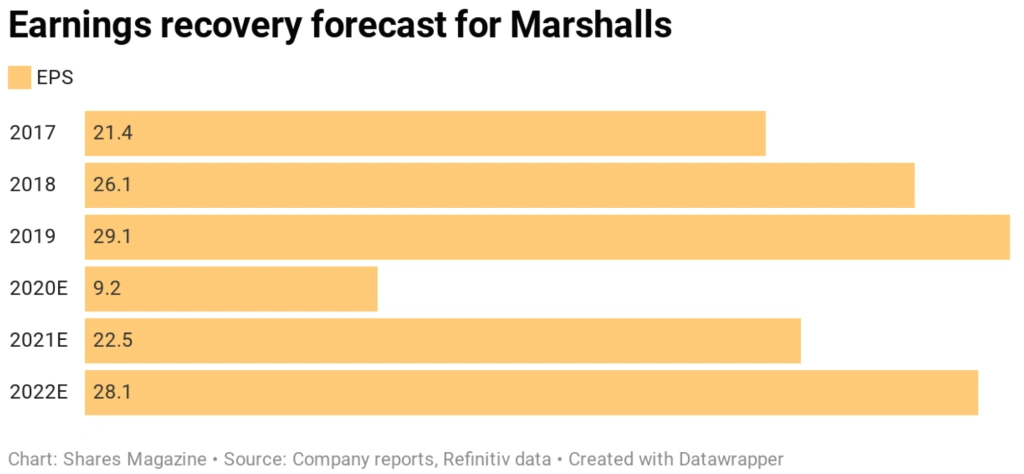

While a 2020 price to earnings ratio of 60-plus reflects the interruption to demand brought about by the pandemic, the shares should look increasingly good value as the recovery feeds through – with the 2022 PE dropping to 22.7 and the shares offering a 2.3% dividend yield for that same year.

We believe the consensus forecasts underpinning these metrics could end up looking quite conservative.

WHAT DOES MARSHALLS DO?

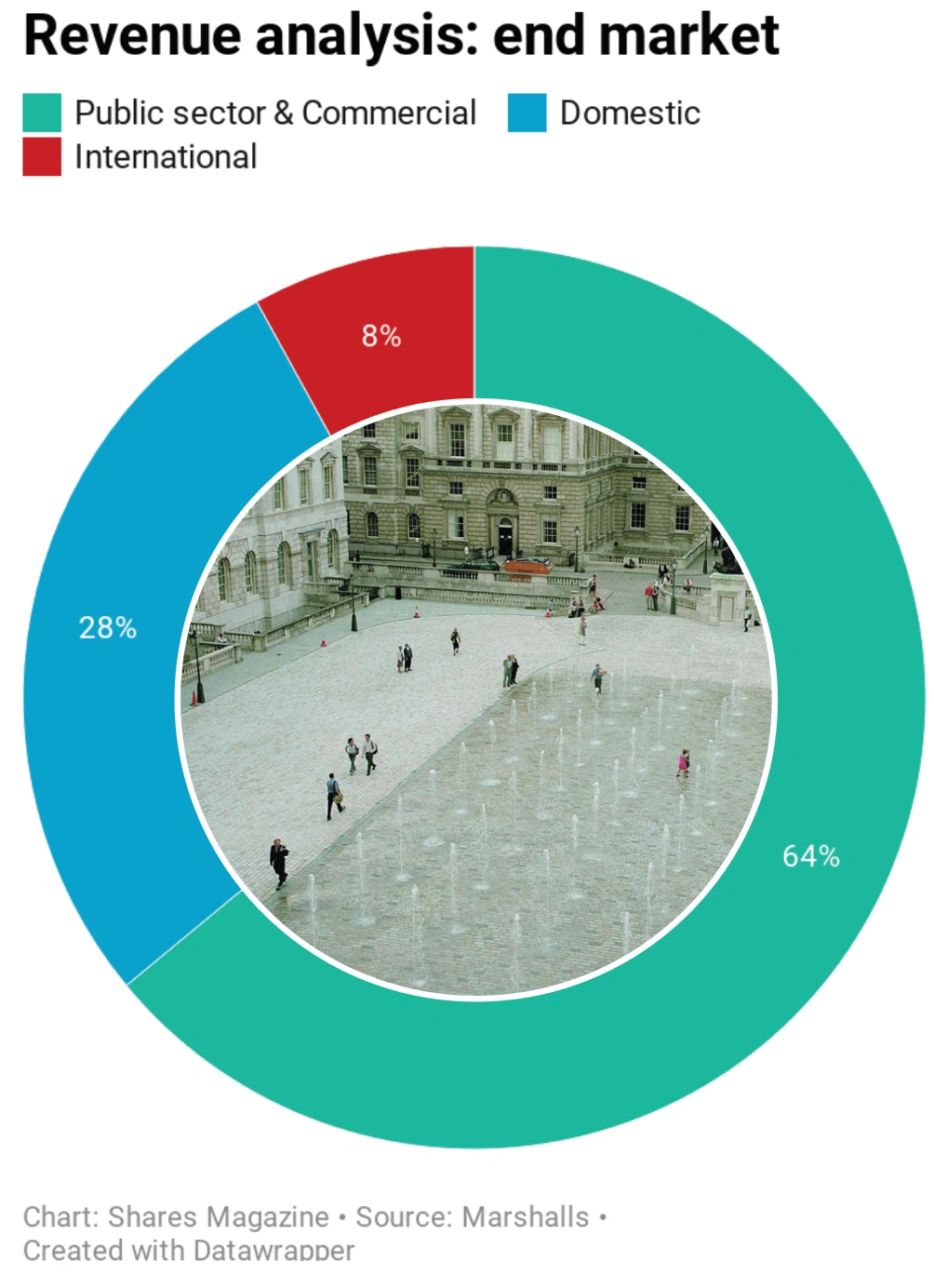

Marshalls makes and distributes external landscaping products like bollards and paving slabs and is the UK leader in this market – it also offers customers support with planning, engineering and design work on projects.

It serves a client base which runs from big governmental and corporate clients down to tradesmen putting in patios and driveways in people’s homes.

The company has an excellent track record of identifying and targeting areas which are likely to see growth and its most recent strategy update (running to 2023) focused on markets with obvious drivers like housebuilding, water management and transport infrastructure.

Like all good businesses it invests material sums internally to improve itself such as revamping its technology and logistics platform and allocating capital to product development.

The company’s technology enables it to offer guidance all the way back to when the architect is drawing up the plans on a project, by enabling them to get the specifications for Marshalls’ product range online and inserting them into the blueprints.

INVESTING IN THE BUSINESS

In product development, chief executive Martyn Coffey tells Shares the company is working on a better finish for some of its products and coming up with concrete products which look like granite, a material mainly sourced from China and therefore much more expensive.

The company is starting construction on a new dual block paving plant at its site in St Ives which represents an investment of £20 million over the next three years.

It complements organic growth with bolt-on acquisitions with Coffey revealing the company is currently interested in deals which would boost its footprint in the water management space.

This spending on organic and acquisitive growth is backed by a strong balance sheet. A year-end trading update (13 Jan) flagged net debt of just £27 million despite the repayment of furlough and VAT support from the Government. Numis analyst Chris Millington forecasts this will come down to £7 million by the end of 2021.

Over the long term, the company’s model has served shareholders well. In the last 10 years it has delivered an annualised total return of 20.3% according to SharePad – compared with 5.6% for the FTSE All-Share and 5% for the sector.

DEMAND DRIVERS

Coffey says Marshalls is seeing excellent demand in the domestic market as people look to scrub up their outdoor spaces in the wake of the pandemic, adding that Covid looks set to have more than just a short-term impact on people’s living habits.

‘People are using space differently and investing long-term to do so,’ he says. ‘This is not just a blip. We are seeing pedestrianisation in inner cities and attempts to make outdoor spaces more appealing by converting car parks, creating paved areas for tables and chairs. These are long-lasting effects.’

Government spending on infrastructure to help fire the recovery from coronavirus should also be supportive to Marshalls. While the pressure on less robust rivals should reinforce and bolster its market share.

The company also ticks ESG (environmental, social, governance) boxes, having committed to ethical sourcing of raw materials for the last 15 years as well as paying the living wage, targeting a reduction in emissions and being ‘Fair Tax’ certified for the last six years (effectively meaning it pays corporation tax responsibly).

Risks include a deterioration in the Covid-19 situation which leads to another pause in construction activity or a hit to consumer-led business due to a downturn in the economy. However, most of Marshall’s domestic customers are in the over-55 age group which has been least affected financially by the crisis.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.