Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSpotting how companies might move the goal posts during the crisis

Accounting scandals have a tendency to crop-up late into a business cycle, perhaps aided and abetted by looser governance standards and a lack of attention to detail by investors who get lulled into a sense of false security after years of stock market gains.

With a long bull market at an end amid the coronavirus crisis it’s arguably more important than ever to for investors to scrutinise their portfolio holdings.

This is something fund managers are very used to doing and looking to tap into some professional expertise, Shares spoke with Tim Steer, a qualified accountant and veteran manager at Artemis and New Star Asset management, as well as author of the book, The Signs Were There. Here are some pointers that he divulged in relation to the current virus pandemic.

It should be made clear that none of the following accounting practices are illegal. However, the accounting rules permit interpretation and how managements use this flexibility can sometimes be illuminating.

1. OVER-PROVISIONING

There is an old adage that says you should never let a good crisis go to waste and some finance directors will be tempted to exaggerate the impact of the lockdown on their businesses in order to make the future look better than it otherwise would.

One way of doing this is to ‘kitchen sink’ the numbers. This refers to the practice of including all possible bad news in a press release for the purpose of ‘lowering the bar’ and making it easier to beat future expectations.

For the retailers, writing down the value of inventory in the current year will reduce profit or add to losses. But this doesn’t prevent management changing their minds later.

A good example of this happened when Mike Ashley floated Sports Direct, now called Frasers (FRAS) in 2007.

Only eagle-eyed investors like Steer noticed that in the year before the initial public offering (IPO) the firm wrote down its inventory by around £30m only to ‘mark it up’ again a year later, boosting profits and potentially helping to achieve a higher price when it came to market.

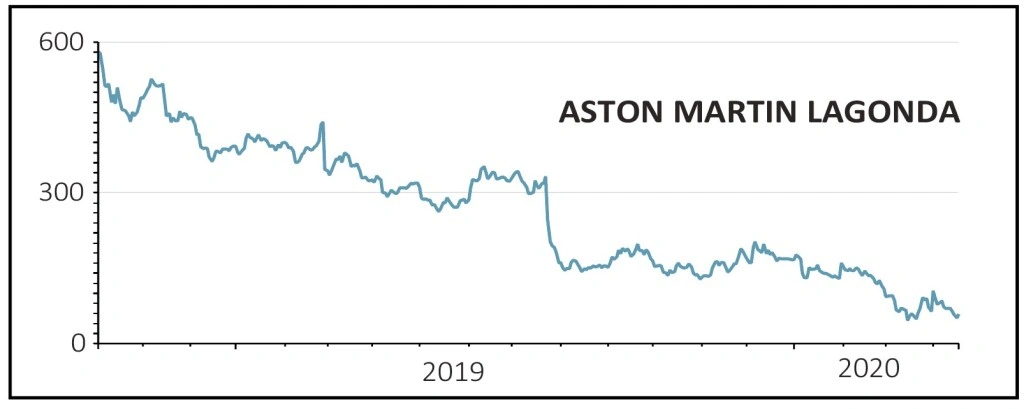

There is a more general point here, and that is, IPOs tend to be overpriced, with most companies coming to market when it suits them and when the numbers flatter the underlying strength of the business. One only needs to look at Aston Martin Lagonda (AML) for a good example of a recently overpriced IPO.

For the banking sector, the same trick can be achieved by writing down a company’s estimate of future bad debts, which in good times, can easily be ‘written back’ to give an extra boost to next year’s profits, without any real change to cash flow.

2. CUSTOMER FINANCE

Steer likes to say that every number companies throw at investors is a ‘matter of opinion’, and the only true number is cash.

It’s possible to book revenue without receiving the cash inflows that one might expect, in fact in some cases cash actually leaves the company’s coffers.

How is this possible? Some companies provided finance to their customers. This shows up in the accounts via a mis-match between reported profits and cash generated from operations, as displayed in the cash flow statements.

For example, internet network equipment firm Cisco Systems recently launched a $2.5bn finance programme (April 14) that allows customers defer 96% of payments until 2021. It seems the company is willing to risk future bad debts in return for booking revenue today.

The advantage is that the results of this gambit won’t materialise for a few years down the road, when investors have likely forgotten.

3. CONTRACT WINS

Some firms might be tempted to defer announcing contract wins so that they appear in the following financial year. This would work well for firms with year ends between March and June 2020.

Software companies often try to book new contacts before the year end in order to meet or beat market expectations for revenue. This might go into reverse during the crisis with companies delaying new contract announcements.

4. BRINGING EXPENSES FORWARD

One of the key principles behind accounting rules is to match income and expenses that relate to the same accounting period.

However it’s up to senior management to elect which period the costs relate to and Steer believes there may be a temptation to bring forward as much of the cost burden as possible into the current period.

A related issue is the government furlough scheme where companies can apply to receive 80% of employee’s pay up to a maximum £25,000. This scheme could potentially be used to flatter results as companies overestimate future payments.

5. OFF-BALANCE SHEET DEBTS AND SUPPLIER FINANCING

When short-seller Muddy Waters released its sell case against Gulf-based NMC Health (NMC) one of its many concerns was that the company engaged in off-balance sheet borrowing in order to understate its debts.

Off-balance sheet debt relates to financing which doesn’t affect official calculations of indebtedness used by banks and credit rating agencies.

NMC, whose shares are now suspended, borrowed money against supplier payments which accountants don’t classify as debt. The same technique was used by the doomed outsourcer Carillion.

The message is clear, be wary of companies that engage in off-balance sheet financing, as they underestimate debt and put investors’ interests at risk.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.