Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhich trusts can weather the dividend cuts storm?

With UK companies suspending dividends left, right and centre, times are tough for income investors.

One possible solution is to look to investment trusts. Many are sitting on significant revenue reserves which they can draw on during ‘rainy days’ to supplement their revenue and maintain dividends during ‘Black Swan’ events such as the coronavirus shutdown.

Most income trusts have accumulated close to or more than one year’s dividend worth of reserves and those funds with bigger revenue reserves dividend coverage are best positioned to weather the storm.

PLENTY IN RESERVE

Supposing the global recession isn’t prolonged, most high-yielding trusts with revenue reserves of one year or more should be able to at least maintain their dividends at the current level during 2020. That’s according to Panmure Gordon which has pored over the investment trust sector’s reserves data.

Despite pandemic-induced uncertainty, the majority of investment trusts are rich in reserves and positioned well to weather the storm, argues the broker, also expecting boards to pay dividends out of capital if they run out of revenue reserves.

As Annabel Brodie-Smith, communications director of the Association of Investment Companies (AIC), explains: ‘Investment companies can squirrel away up to 15% of the income they receive each year and tuck it into a revenue reserve. This rainy-day pot means investment companies often have income to draw on to boost dividends during more difficult times like those we are seeing now.

‘If we look at the UK Equity Income sector for example, 18 of the 25 investment companies have enough income tucked away in reserve to pay out their last full year of dividends, even if they don’t receive any income from their portfolios.’

According to Panmure Gordon’s analysis, the higher yielding AIC sectors with healthy revenue reserves are UK Equity Income, Asia Pacific, Global Equity Income and Europe. Panmure also highlights the UK All Companies, North America and Debt – Loans & Bonds sectors, which have funds yielding over 3%, 3% and 4.5% respectively.

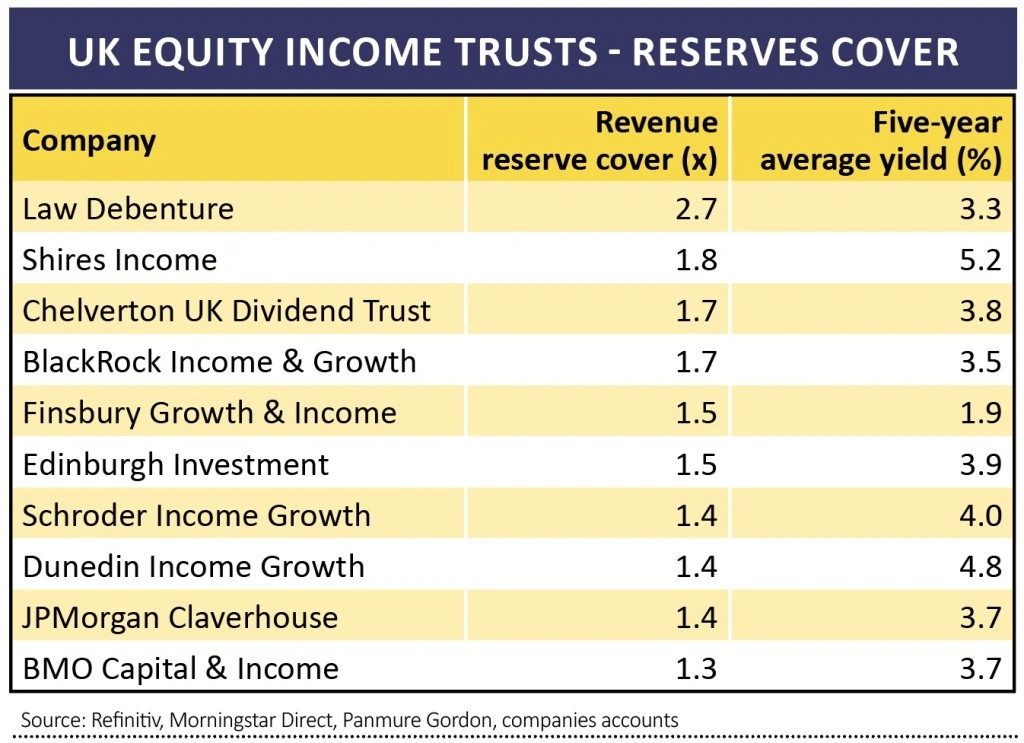

And although a blizzard of dividend cuts or deferrals from UK companies has created nervousness around the UK Equity Income sector’s ability to sustain dividends, Panmure’s analysis reveals that 25 of the sector’s 26 trusts have high revenue reserves.

The top four by highest revenue reserves cover are Law Debenture (LWDB), Shires Income (SHRS), Chelverton UK Dividend (SDV) and BlackRock Income & Growth (BRIG).

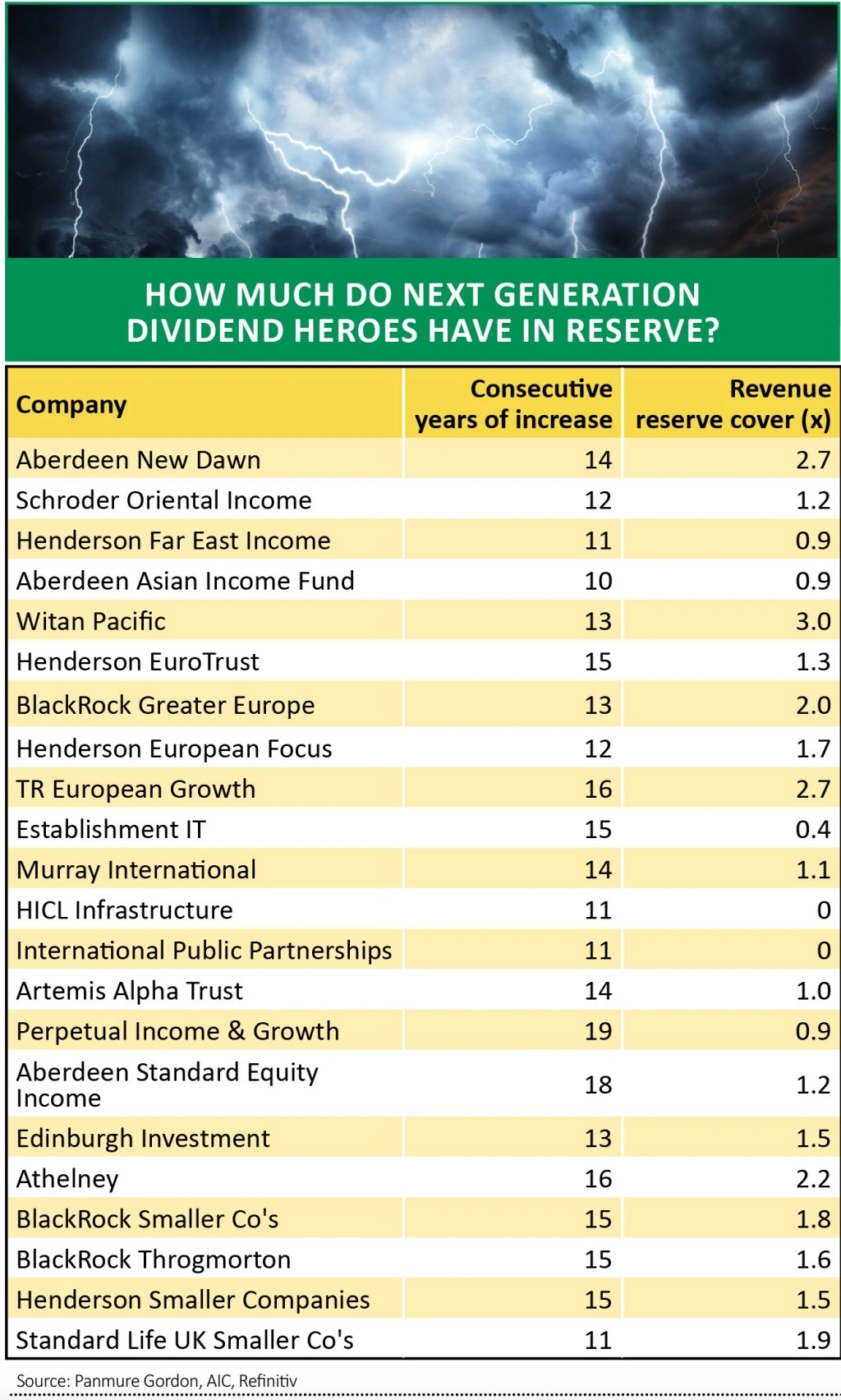

HOLDING OUT FOR A HERO

According to Panmure Gordon, both the AIC’s 20-strong band of present ‘Dividend Heroes’ – which have grown the payout for 20-plus consecutive years – and its 22 next generation dividend heroes – doing it for over 10 but less than 20 years – are likely to retain their status for the year ahead.

They have an incentive to do so as their track records are a key selling point. Their revenue reserves are sufficient to pay at least one, or close to, one year of dividends, although the broker unearthed one vulnerable fund in the form of Value and Income (VIN), a current hero with a 31 year dividend growth record which has no reserves to support its future dividend.

TIME TO GO GLOBAL?

Much of the focus has been on the risk of dividend cuts within the UK Equity Income sector, yet Stifel has helpfully crunched the numbers across the Global and Global Equity Income sectors too. ‘Historically, the UK has been a relatively high dividend paying stock market and the largest shortfalls in revenues are likely to be across the UK Equity Income Trust sector,’ explains Stifel.

‘We think the Global and the Global Equity Income sectors may be less exposed to dividend cuts, given that dividend payments for many of the overseas companies they own may account for a lower proportion of these companies earnings than for UK businesses.’

Of the 18 trusts reviewed, Stifel found that half of them have delivered dividend growth for at least 15 years on the spin and many for much longer. Bankers (BNKR) and Alliance Trust (ATST) boast 53 years of consecutive dividend growth, while others with long dividend growth records are F&C Investment Trust (FCIT) with 49 years growth and Brunner (BUT) with 48 years.

‘We take some comfort from the fact that eight out of these nine trusts had in excess of the total cost of one year’s dividend in their reserves at their last year-end,’ enthuses Stifel, which ‘bodes well for the future’.

The one exception to this group is the capital growth-focused Scottish Mortgage (SMT), which only has a dividend yield of 0.5%.

Bruce Stout-steered Murray International (MYI), with a 5.6% dividend yield, is the highest-yielding trust. ‘It has substantial revenue reserves, equivalent to 1.1 times the cost of the annual dividend and appears well positioned’, says Stifel of Murray, which has a bias to overseas equities and offers exposure to bonds too.

Its Global Equity Income peer Scottish American (SAIN), which has racked up 40 consecutive years of dividend growth, has revenue reserves of £17.3m and cover of one times, according to Stifel.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.