Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

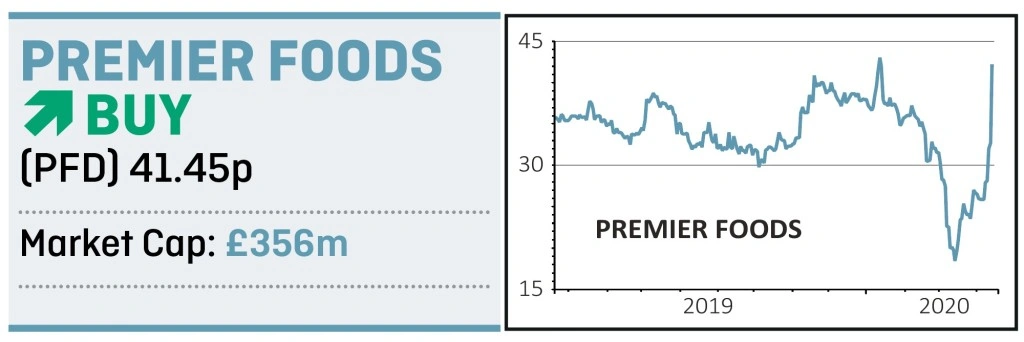

magazineWhy now is the time to snap up Premier Foods

Despite the popularity and ‘authenticity’ of brands such as Bisto, Cadbury’s – made under licence for US conglomerate Mondelez – and Mr Kipling, investors have given Premier Foods (PFD) a wide berth until now due to its widely-reported lack of free cash flow and pension ‘black hole’.

However, a plan to sort out its various pension scheme deficits should significantly reduces the amount of cash needed on an ongoing basis and goes a long way to de-risking the business.

Together with the pension update, Premier revealed that trading for the year to 28 March was at the top end of market expectations and that it had generated £90m of operating cash flow, bringing the ratio of net debt-to-EBITDA (earnings before interest, tax, depreciation and amortisation) ‘comfortably’ lower than the previous target of three times.

The combination of the pension deal and better than expected results makes Premier considerably more investable than in the past.

The transformational pension deal involves merging three of its retirement schemes and then paying an insurer to take over the liabilities of the largest plan (called a ‘buyout’). Any surplus from the buyout will help to fund deficits in the two remaining schemes.

The firm ended the year to March with £90m, to which it added £85m from its credit facility to give it £175m of available firepower.

These funds will be used to push on with its successful ‘branded growth model strategy’, building on the success of its market-leading brands.

Having seen steady like-for-like growth in the nine months to December, demand for the group’s products soared in the last quarter as shoppers cleared supermarket shelves.

UK sales were up 7.3% over the final three months and up 15.1% in March alone, putting full year trading profits at the top end of expectations.

With demand continuing at above-average levels as the lockdown continues, Peel Hunt has raised its earnings forecast for the current year and raised its target price from 50p to 80p.

As the firm continues to roll-out self-help solutions, we believe there is potential for sales and earnings to further exceed market forecasts.

At their current price, the shares trade on less than five times expected 2021 earnings and a free cash flow yield of over 15%. That’s far too cheap given that Premier Foods has a plan to resolve pension issues, trading is good, and it should soon have more cash to reinvest in its business.

Fundamentally this company is at a major turning point and there is plenty to suggest its shares deserve a massive re-rating.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.