Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe race to recovery

The market has come storming back since it bottomed out on 23 March from a coronavirus-inspired plunge. As we write the FTSE 100 is above the 5,700 mark and some 16% off its lows.

Suggestions that some countries are past the peak of infections, a cautious reopening of the Chinese economy and reports of progress on a coronavirus treatment have all helped sentiment.

In the FTSE 350, travel operators and gambling companies, two areas which sold off the most, appear to have rebounded the strongest, though they are still some way off their pre-coronavirus crisis levels.

While those continuing to flounder come from a more diverse set of sectors, including banks, building materials, general retail, industrials and utilities.

In this article we show you the FTSE 350 businesses which have performed best through this period, helping to power this rebound and those which have been left behind.

We identify two stocks which we think can maintain their current momentum and one which has the potential to play catch up in the months ahead.

Whether we’re in for a so-called ‘V-shaped’ recovery, where share prices recover quickly, remains to be seen, with the recent bumps in the road for the market perhaps suggesting this may not be the case.

It’s also worth considering that the recent market advance could turn out to be a ‘bear trap’, as seen most recently in 2007-09 during the global financial crisis.

In fact, history has shown bear markets are littered with sharp advances which cruelly turn out to be nothing more than traps for the unwary, with investors tempted into a ‘buy-on-the-dip’ strategy, only to quickly find themselves in trouble.

Despite this warning, we believe the best strategy is to stay invested, even if markets pull back again in the near-term.

Has big tech bounced too much too quickly?

Investors are nervous about big tech. Many think that leading stocks have rallied faster and jumped higher than the wider market, calling into question valuations that ‘do not reflect the risks that still lie ahead from coronavirus,’ according to a Financial Times opinion piece last week.

Yes, there are examples of soaring optimism, just like there was before the outbreak. Advanced Micro Devices and Netflix, for example, have jumped 47% since 23 March, far outstripping the S&P 500’s rough 25% rally. Video conferencing firm Zoom, an app used by millions to stay in touch with family and friends during lockdown, has more than doubled in 2020, surging from $68.72 to $150.26.

Shares in Apple, Microsoft and Amazon, all worth more than $1trn, have rallied 28%, 30% and 26.5% respectively since 23 March but that is not so out of kilter with wider markets, and nor are valuations for most. Apple trades on a current year PE of 24, Microsoft at 37, while Google parent Alphabet, up 19.5%, trades on a 26 PE, versus a 20 PE for the S&P 500 and 24.5 for Nasdaq.

Yes, Amazon’s PE of 114 remains eye-watering, but it has been so for years, reflecting the market’s optimistic view of long-run growth.

WHO HAS RACED AHEAD IN THE RALLY?

The best FTSE 350 performers since the market’s most recent bottom are in many cases those businesses which suffered the most in the early part of the coronavirus-inspired sell-off amid growing investor optimism that the number of infections could be reaching a peak and that a return to normal life (albeit gradually) could be on the horizon.

A good chunk of the top 20 best performing FTSE 350 stocks since 23 March come from the travel and leisure sector, comprising bus and rail companies, bookmakers and pub companies.

The bookies have done best during the period, with William Hill’s (WMH) share price soaring 135%. This reflects reports of a rise in online gambling during the lockdown. The ongoing postponement of nearly all sporting events remains a big problem though, with around 53% of William Hill’s revenue in 2019 coming from sport.

And while the airlines have still struggled, domestic travel companies like Go-Ahead (GOG) and National Express (NEX) have improved as talk of potentially easing lockdown restrictions gather pace.

When it comes to travel, if restrictions start to get lifted people are perhaps more likely in the near-term to travel to other towns and cities to see loved ones or for work than they are to take a plane and go abroad for a holiday.

Insurance firm Legal & General (LGEN) was a strong performer as it defied regulator pressure and confirmed it would pay its already declared final dividend.

Just under six months ago we studied three major stock market sell-offs of the last decade and the subsequent recoveries to see if there were any reliable patterns we could identify.

The three periods were mid-2011, mid-2015 and late 2018. All three sell-offs took the FTSE 350 index down more than 10%, and in each case the same sectors tended to come off worse.

On average the five worst sectors were Automobiles & Parts, Industrial Metals, Industrial Transportation, Mining and Oil Equipment & Services. Aside from Industrial Metals and Mining, these sectors also typically performed poorly in the six months following the market low.

In the six months following each sell-off, the best performing sectors also tended to be the same: Electronic Equipment, Industrial Engineering, Industrial Metals, Mining and Tech Hardware.

However, the latest sell-off has been very different as the nature of the crisis and the resulting lockdown has hammered Travel and Leisure and General Retail stocks far harder than previous sell-offs.

As a result these are the sectors rallying the most since the market low last month, which is atypical, but it’s worth flagging that we are less than one month on from the market low – if it was the low – and a lot can change over six months.

TWO STOCKS WHOSE RECOVERY HAS LEGS

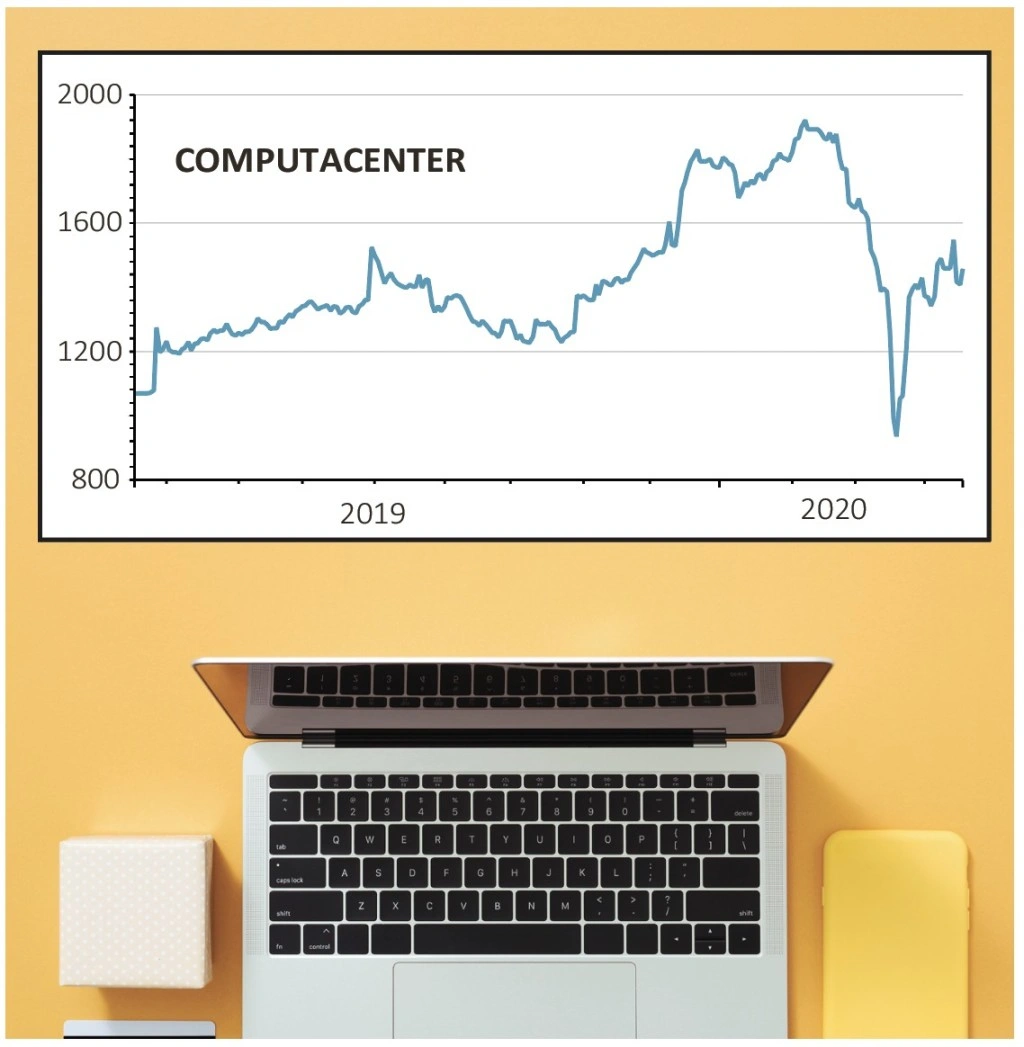

Computacenter (CCC) £14.52 *BUY*

As a digital enabler, one that is helping the staff of many businesses operate effectively from home during lockdown, it is perhaps unsurprising that Computacenter (CCC) has rallied so strongly in recent weeks.

Having nearly halved in the immediate aftermath of the pandemic outbreak, the stock has bounced more than 30% since the market hit 4,993.89 on 23 March, even if this performance isn’t quite enough to make the list of top 20 FTSE 350 performers since that low point.

Computacenter is a pan-European IT enterprise operator whose 14,000-odd staff annually ship more than 25m PCs, laptops, smartphones and much else to 4.2m end users, and provide valuable advice support and services in 30 different languages. It has been part of the FTSE 250 index for most of the last 10 years.

Even before the coronavirus, we were firmly in an era of unprecedented technological change, where thousands of organisations needed help with adaption and adoption. That might be to stay competitive, engage better with customers, improve access to information and services, bolster efficiency or simply trim costs. There are many reasons to embrace digital tools and services and Computacenter is a key trusted partner for thousands of organisations.

Providing the tech hardware and gadgets, supplying consultancy, advice and key software tools for clients from proper blue-chip vendors (think Microsoft, Oracle, Adobe, Cisco, Symantec, Sophos), it is a model that has worked for years thanks to steady growth and superb cash flows.

Computacenter has an unbroken track record extending more than 10 years for annual earnings increases, which feeds into reliable dividends.

Most recent commentary from the company in March was upbeat on the long-run digital shift, saying that supply chains were still running smoothly and purchasing decisions were being made. But the pandemic obviously raises questions on the near-term impacts, with key risks being possible supply constraints if large IT equipment manufacturers start to run low on stock. There is also the danger that some larger IT projects could get canned while business uncertainty persists.

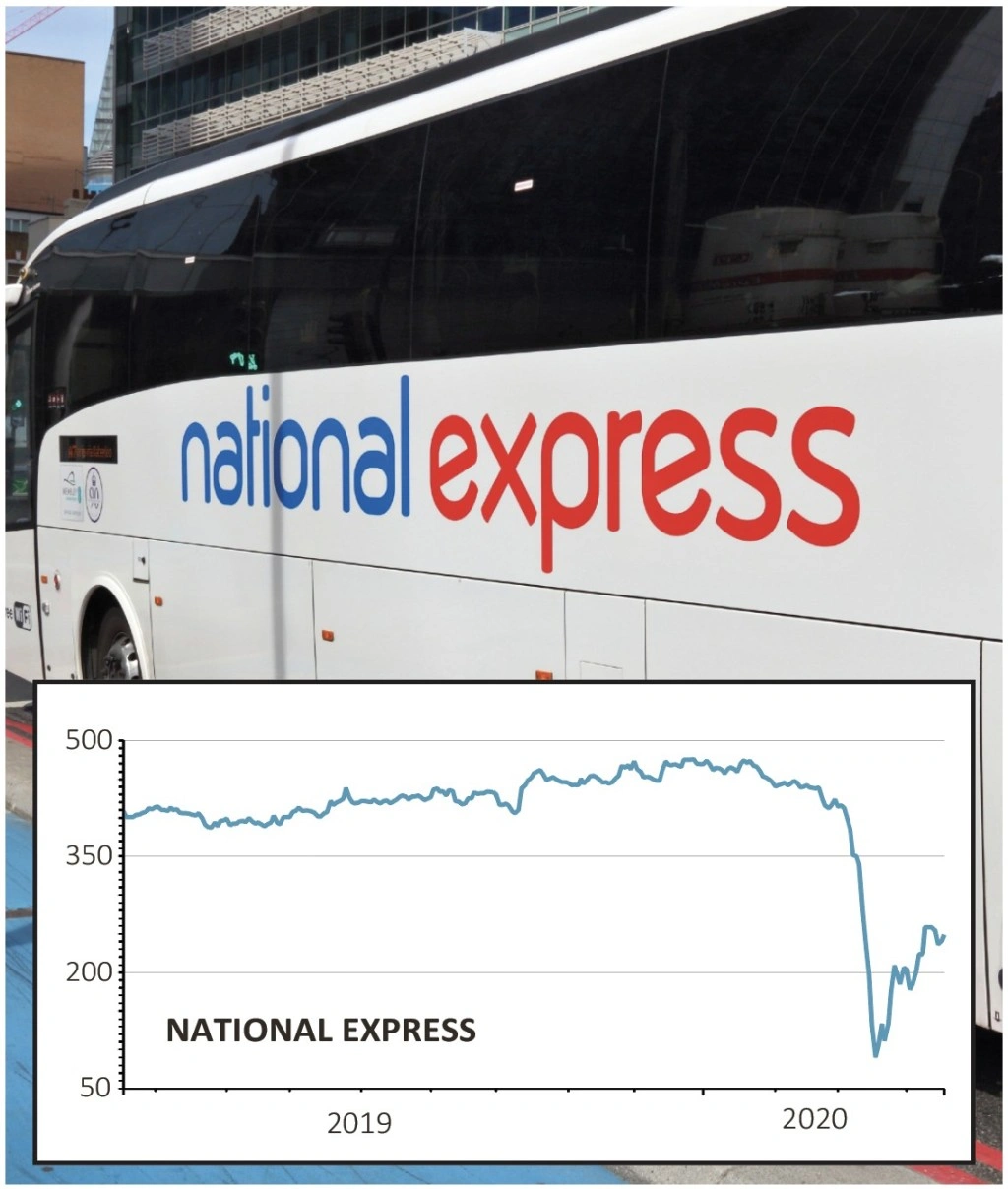

National Express (NEX) 241p *BUY*

While being heavily sold off along with all the other stocks in the same sector, coach operator National Express (NEX) has been one of the best performing stocks since the market started bouncing back.

Its share price has jumped significantly since 23 March, and we think there’s good reason for this increase.

A household name and one of the go-to companies when looking to book a coach journey, National Express had been growing strongly before the coronavirus crisis hit.

Its results for 2019 showed double-digit revenue and operating profit growth, while in an update released last week, the company said that in the first two months of 2020, it had grown revenue by 17% year-on-year.

According to Canaccord Genuity analyst Gert Zonneveld, National Express is ‘well positioned to weather the storm’ from the coronavirus outbreak.

He conceded the pandemic will have a ‘significant impact’ on near-term earnings, but added that the business remains a ‘best-in-class operator in virtually all of its businesses, capable of delivering sustained profit growth’.

The company also has no major liquidity concerns, with cash and undrawn facilities of around £500m.

Zonneveld forecasts a small earnings per share loss in 2020 before bouncing back strongly in 2021 and returning to normal in 2022.

WHO HAS LAGGED BEHIND THE MARKET?

The stocks which have struggled to keep up with the market’s rebound since late March include a collection of businesses with either strained balance sheets – like energy provider Centrica (CNA) – or exposure to industries and sectors where the impact of the coronavirus might not have been immediately obvious or there have been few grounds for any optimism in the interim.

Retailer Dixons Carphone (DC.) and shopping centre landlord Hammerson (HMSO) remain on the floor, while sporting goods specialist Frasers (FRAS) has also endured a difficult crisis so far as its attempts to stay open in the lockdown proved a PR disaster.

Fears over the impact of the current economic maelstrom on emerging markets and rock-bottom interest rates have kept banking outfits HSBC (HSBA) and Standard Chartered (STAN) on the back foot. UK-focused bank Royal Bank of Scotland (RBS) has also struggled.

Elsewhere Rolls-Royce (RR.), Melrose Industries (MRO) and Senior (SNR) suffered thanks to their position as suppliers of parts to the devastated aviation industry.

Insurer Hiscox (HSX) suffered amid the suspension of its dividend and news it could face a lawsuit after refusing to pay out on claims linked to the coronavirus lockdown.

It is perhaps surprising not to see more oil businesses among the list of laggards given prices remain firmly under pressure despite recently agreed OPEC+ production cuts. Oil services firm Petrofac (PFC) is the only relevant name on the list of the 20 worst performers.

A STOCK WITH RECOVERY POTENTIAL

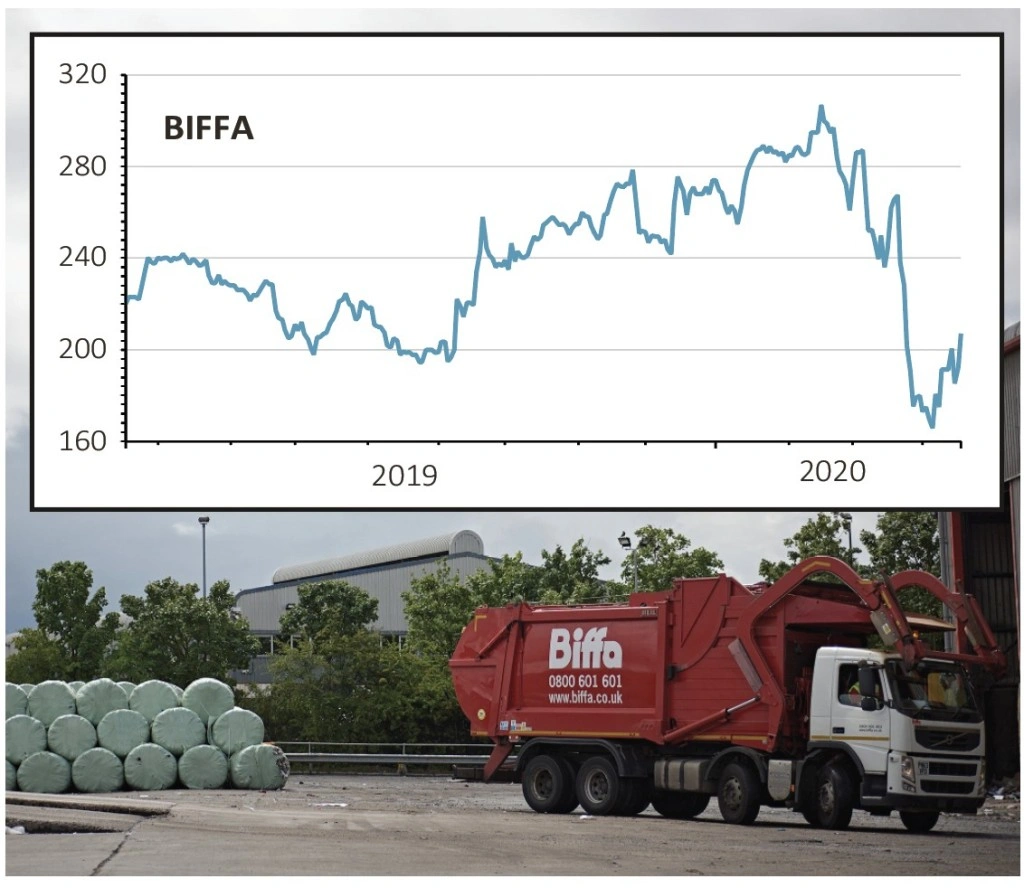

Biffa (BIFF) 200p *BUY*

An anticipated hit to its landfill services from paused construction activity, plus substantially reduced demand for industrial and commercial business has put waste management firm Biffa (BIFF) on the back foot.

A dispute with union Unite and its workers on the Wirral over safety concerns hasn’t helped and neither did the cancellation of its dividend (25 Mar).

In addition, the company has significant borrowings for investors to consider. However, it looks to have a robust enough balance sheet to weather the current reduction in business and it should prove a survivor in the sector, putting it in a strong market position when we emerge from the ongoing coronavirus crisis.

Numis comments: ‘Our base case cash burn scenario indicates that the group has around one year of liquidity given current headroom of c.£150m, consistent with what management outlined in its Covid-19 update.

‘We believe this is likely to be materially more headroom than many other waste sector peers.’

While certain parts of the economy may be irrevocably changed by the pandemic, someone is still going to have to take care of our waste and this is something Biffa is good at. It is also adapting to increasing pressure to factor in environmental concerns by looking to improve its recycling and recovery capability.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.