Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

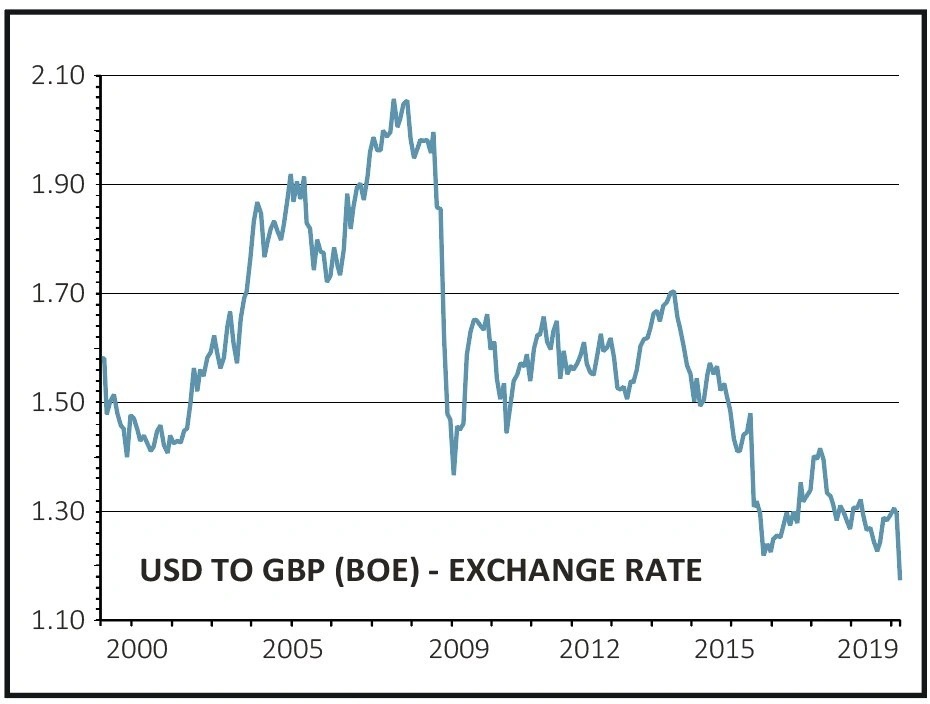

magazinePanic buying of US dollar sends sterling to 35-year low

In the past week the US dollar has soared against other currencies as investors have stampeded into what are considered safe-haven assets on fears that the coronavirus will send global economies into freefall.

At one point, sterling hit a 35-year low against the US currency at $1.15, partly on the dash for dollars and partly on fears that the UK Government was behind the curve in its treatment of the coronavirus pandemic.

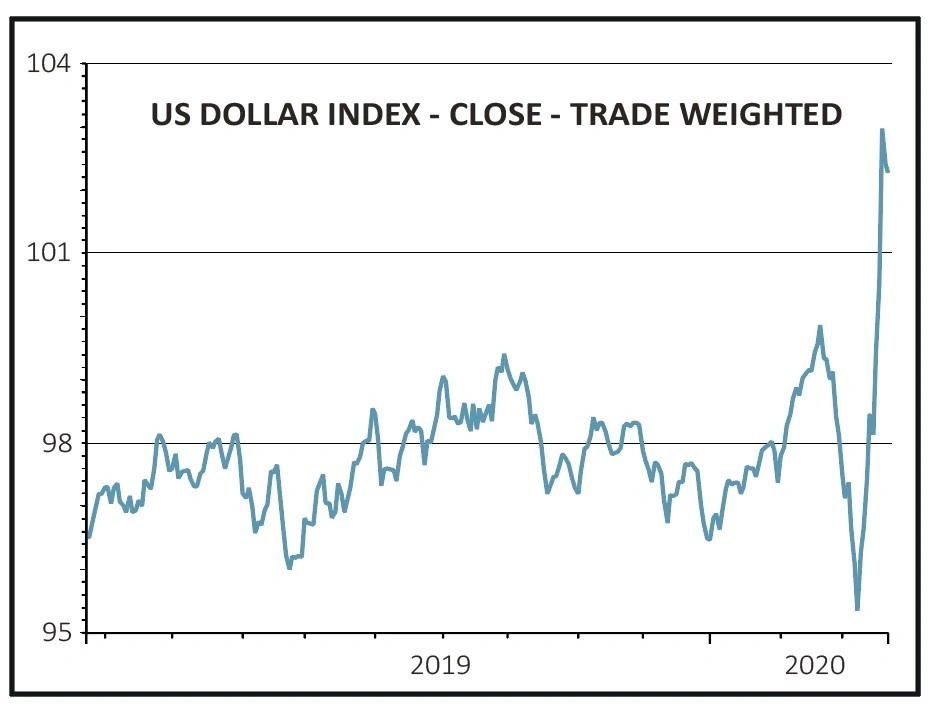

DOLLAR DEMAND SURGES

Demand for the dollar, the world’s number one reserve currency, has surged to record highs amid a rush for cash on concerns that the coronavirus pandemic could take longer than expected to bring under control.

As one multi-asset manager put it, ‘nobody wants duration risk, nobody wants equity, everybody wants cash and the reserve currency is the dollar’.

The scramble for liquidity is not expected to change in the short term, and central banks around the world are trying to find ways of getting dollars to those that need them.

The US Federal Reserve agreed to lend billions of dollars at near-zero interest rates to central banks in Australia, Japan, South Korea, Switzerland and half a dozen other countries who had seen sudden and unprecedented buying of the US currency.

Bloomberg quoted a foreign exchange strategist at an Asian bank as saying ‘the dollar is rallying on haven demand as markets are digesting the implication of job losses and a prolonged economic downturn’.

EMERGING MARKETS HAMMERED

As well as heavy losses in sterling there was huge pressure on emerging market currencies. Among the hardest hit were Asian currencies such as Indonesian rupiah, Malaysian ringgit and Thai

baht as more countries shut their borders and imposed restrictions on freedom of movement.

The Korean won, seen as particularly vulnerable to a global growth slowdown due to Korea’s large manufacturing industry, also came under selling pressure as investors fretted over capital outflows.

Rating agency Standard & Poors, which last

week warned that the pandemic could cost the Asia Pacific region $400bn in economic losses, this week raised its forecast of the potential loss of income to $620bn.

HISTORIC LOSSES ON CARRY TRADES

‘Carry trades’, where traders borrow low interest rate currencies like dollars or yen and use that money to buy higher interest rate currencies like those in emerging markets, have suffered historic reversals as demand for dollars has soared.

The synchronised rush to buy dollars sent carry trades involving emerging market currencies towards their biggest quarterly loss in more than 20 years.

According to data compiled by Bloomberg, the average return on carry trades in emerging market currencies is -13% so far this year. Moreover, traders believe that the selling of currencies such

as the rupiah and the won may have further to go.

Currencies in more developed markets such as Mexico, South Africa and Turkey have also been pressured with carry-trade losses mounting in these markets.

Another factor undermining these trades has been the sudden increase in volatility. Carry trades typically rely on a steady trend continuing into the future with little change in volatility.

One currency trader said: ‘This is not the time to play carry trades. The key for carry trades to thrive is volatility remaining low. The world has changed and it’s hard to see a revival in carry trades.’

RISKS IN CREDIT AND EQUITY

Along with the surge in demand for dollar liquidity there has been a huge flow of funds out of credit and equity investments. Credit quality has been deteriorating steadily since the financial crisis with the result that much of the corporate borrowing of the last decade is low grade.

Firms experiencing a sharp drop in revenues and profits risk seeing their debt downgraded, which increase the refinancing risk. This in turn puts pressure on credit spreads – the rate which firms have to pay above the rate on government debt – which in turn means a liquidity squeeze.

Mohamed El-Arian, chief economic adviser to Allianz Investors, believes that investors were living in a ‘dream world’ last year as three things happened which don’t normally occur together, lulling investors into a false sense of security.

‘Firstly, investors received massive returns on their risky assets including equity markets. Secondly, investors made money on risk-free assets such as bonds. And thirdly, this all happened in a context of virtually no volatility.’

Investors therefore took on more risk than they were typically comfortable with because there seemed to be no downside.

However there is now a genuine risk that equity shareholders could be wiped out if they own any financially weak companies which subsequently go bust, and bondholders aren’t necessarily guaranteed to get their money back. Hence the sudden, coordinated dash for cash.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.