Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRestore can keep increasing market share and margins

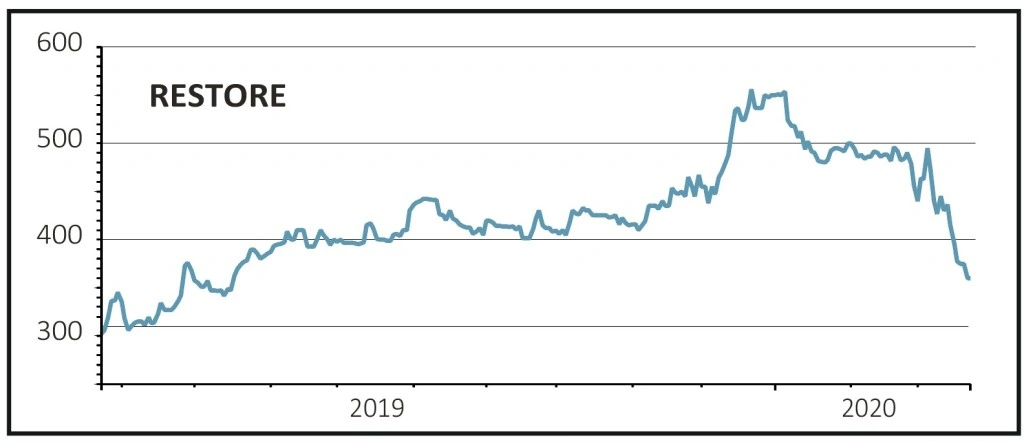

Restore (RST:AIM) 360p

Loss to date: 14.2%

Buy at 420p, 18 July 2019

The latest results from document management firm Restore (RST:AIM) show that the business continues to fire on all cylinders, gaining market share while at the same increasing profit.

Revenue for the year to 31 December was 10% higher, driven by a combination of high recurring revenues in lower-growth markets like records management and shredding, where increased regulation helps to drive sales, and above-market growth in faster-growing segments like digital scanning and IT recycling and relocation.

As well as generating steady organic growth thanks to top-tier positions in each of its businesses, the management team is always looking to increase market share and cross-selling opportunities through attractive bolt-on acquisitions.

Due to the fragmented nature of many of its markets, there is significant room to continue growing while at the same time a focus on technology and operating efficiency means that margins and earnings can expand faster than revenues. Profit last year was up 13%.

Chief executive Charles Bligh is wholly-focused on growing Restore’s cash generation, which together with the firm’s strong financial base ensures it is well-placed to ride out the current crisis and will be ‘the first out of the blocks’ when the economy normalises.

SHARES SAYS: We remain positive on the shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.