Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSortino ratio: a smart way to measure fund performance

A little known but potentially very useful way to measure the return on an investment received its moment in the spotlight in January 2020 after getting name checked by star fund manager Terry Smith.

In his his annual letter to shareholders in Fundsmith Equity (B41YBW7), Smith included something called the ‘Sortino ratio’ for the first time when looking at the fund’s performance.

It is an adaption of the commonly used Sharpe ratio, a measure developed by Nobel laureate William F. Sharpe to help investors understand the return of their investment compared to its risk.

The Sharpe ratio measures the performance of an investment compared to a so-called ‘risk-free asset’ like a government bond, and the ratio is the average return earned in excess of the risk-free rate.

While the Sharpe ratio looks at all volatility, i.e. both on the way up and on the way down, the Sortino ratio – developed by investment academic Frank Sortino – excludes upside volatility (because why would you be concerned when your investment goes up) and only looks at downside volatility.

JUST FOCUSED ON DOWNSIDE VOLATILITY

As a general rule, a Sharpe ratio with a score of one or above is considered good, while for the Sortino ratio a score of two or above is what fund pickers look for though one or higher is still acceptable.

In his annual letter, Smith calls the Sortino ratio an ‘improvement’ on the Sharpe ratio.

He says: ‘Whereas the Sharpe ratio estimates risk by the variability of returns, the Sortino ratio takes into account only downside variability as it is not clear why we should be concerned about upside volatility (i.e. when our fund goes up a lot) which mostly seems to be a cause for celebration.’

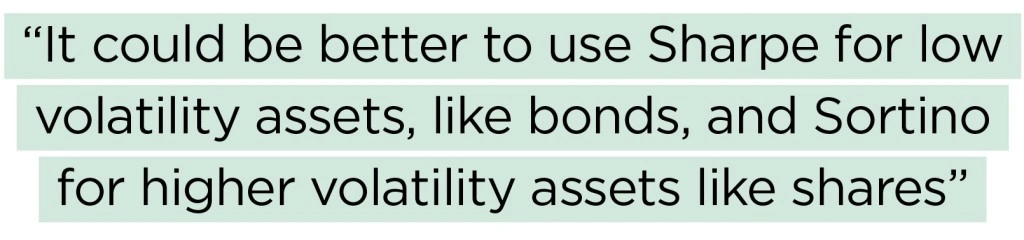

AJ Bell head of active portfolios Ryan Hughes says that while the Sharpe ratio remains the more common measure, it could be better to use Sharpe for low volatility assets, like bonds, and Sortino for higher volatility assets like shares, also known as equities.

Hughes explains, ‘The rational for Sortino is that upside volatility is considered good for equities and therefore equities shouldn’t be penalised for having high upside volatility.’

TECHNICAL TERMS EXPLAINED

UPSIDE – the potential increase in value of an investment, measured in monetary or percentage terms.

DOWNSIDE – the negative movement in the price of an investment, sector or market.

STANDARD DEVIATION – a commonly used way to quantify risk, measuring how much the value of your portfolio moves around.

RISK-FREE RATE – the rate of return on a hypothetical investment, over a given time period, with no risk of financial loss. Terry Smith defines this as ‘basically the return on government bonds’.

EXCESS RETURN – a measure of how much an investment has returned compared to a benchmark or index (e.g. an active UK equity fund compared to the FTSE 100), also known as alpha.

FUND SELECTION TOOL

The Sortino ratio could also help you pick a fund to invest in, as after all investment fund managers are judged on how good they are at turning risk, measured by volatility, into return.

The majority of people who pick funds for a living look at the Sharpe ratio when assessing the above, but Patrick Thomas, an investment director at Canaccord Genuity Wealth Management, thinks it is better to look at both the Sortino and Sharpe ratios.

Thomas explains, ‘A fund manager who does a consistent excess return of 2% with 2% standard deviation is as good as a fund manager who delivers a consistent excess return of 12% with 12% standard deviation, i.e. despite the different risk and return of the two funds, both fund managers have delivered the same Sharpe ratio.

‘But they are not the same obviously. So clearly, the main issue is that the Sharpe ratio fails to distinguish between downside volatility (generally considered bad) and upside volatility (which no investor ever moans about).

‘So that’s why they modified the Sharpe ratio to take into account only downside volatility by developing the Sortino ratio.

‘Again, the higher the ratio the more attractive the risk-adjusted return. So it’s essentially a sign of a fund that is going to perform well in negative markets.’

But he adds Smith talking about the Sortino ratio in his letter is ‘a bit strange’, given that fund managers typically have to use a long/short strategy or some other type of hedging in order to demonstrate a ‘genuinely attractive’ Sortino ratio.

A SELECT FEW HIT THE MARK

Fundsmith Equity has a Sortino ratio of 1.22 since inception, which is well above the 0.59 for its MSCI World Index benchmark but still below the two mark that is considered the gold standard.

However, most funds on the market fail to reach a Sortino ratio of one for any meaningful period of time, even when using the most commonly used risk-free rate at the moment – the yield on 10-year UK gilts, which due to the low interest rate environment currently stands at 0.6%.

According to data from FE Analytics, only Fundsmith, Investec Global Franchise (B7VHRM9) and Morgan Stanley Global Brands (3248249) have a Sortino ratio above one over five years.

The funds that do have a Sortino above two are mostly property or commodity funds, which tend to be less volatile as they often have illiquid assets that are only priced once or twice a year.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.