Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat’s the catch with investment trusts yielding above 5%?

Little is more satisfying in investing than receiving a dividend payment from one of your holdings and investment trusts have an excellent track record of delivering a regular stream of income.

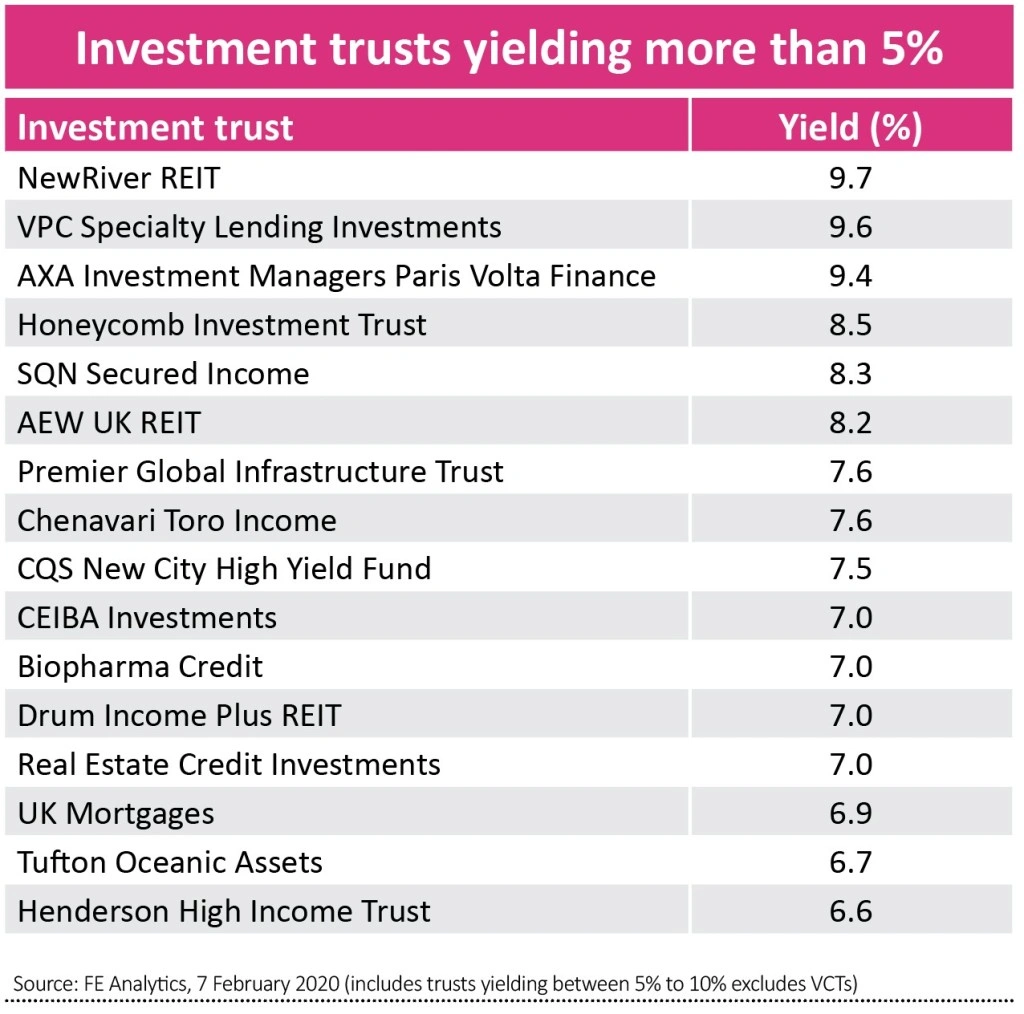

Some trusts offer very attractive yields too. According to industry body the Association of Investment Companies, the average for all trusts is 3.2% but there are a significant number of trusts which offer dividend yields in excess of 5%.

In this article we will concentrate on the trusts with yields of between 5% and 10%, above which the yield is likely to be an anomaly, quirk of the data or situation where the dividend is almost certain to be on the chopping block.

We will examine the merits of higher yielding trusts in general and identify two which investors should buy today.

A RED FLAG?

A high yield can attract investors seeking the generous income on offer, but it should also be considered as a red flag as it often means a dividend is considered by the market to be unsustainable and can reflect a falling share price.

Hadrian’s Wall Secured Investments (HWSL) is a classic example of an investment offering an exceptionally high yield because it has fallen dramatically in value.

The trust launched in June 2016 with a proposition which involved offering secured loans to small businesses at relatively high interest rates. A good chunk of this income was then returned to shareholders, once the trust’s bills had been paid and some money had been held as a buffer against hard times.

However, the company ran into trouble after loaning money to biomass projects where as broker Winterflood noted ‘the security on the (biomass) investments appeared to be worthless’.

In January the company increased its loss provision from £3.27m to £18.1m on these loans and its yield of 12.1% reflects the fact its share price has halved in the last year. A fall in the share price will push the dividend yield up, based on the most recent full year dividend payment.

Looking at some of the other higher yielding collectives in the investment trust universe, several are actually venture capital trusts (VCTs). These are funds that allow investors to claim up to 30% income tax relief on an investment of up to £200,000 a year.

You need to hold the investment for at least five years, but any dividends will be tax free and you will have a capital gains exemption on disposal.

However, VCTs are only suitable for certain investors as they involve high charges and invest in small, often unquoted companies.

Putting these products to one side, there are also some more high-yielding esoteric vehicles which either have complex structures or operate in niche areas like aircraft leasing or asset finance where the risks may not be easy to recognise and understand.

RUNNING HARD

The FTSE All-Share is often used as the benchmark for the UK stock market. It is currently yielding 4.2%.

QuotedData analyst James Carthew says: ‘For an equity fund to achieve a yield a quarter higher than the market yield it would have to be running quite hard.

‘A trust probably has two ways to achieve that; it can invest in high yielding, value type situations, potentially at the expense of some capital growth, or it can use some engineering to avoid buying really high yielding stuff.

‘You need to think about diversity of income. If a trust is relying on just a handful of holdings to generate income then that can easily go wrong.’

The ‘engineering’ referenced by Carthew can include the use of options or purchasing different classes of share which offer higher income. He adds this is ‘not necessarily a bad thing’.

He cites the example of Shires Income (SHRS) which uses lower cost debt to buy a portfolio of higher yielding preference shares. It trades on an historic yield of 4.6%. Another popular income-focused trust offering a yield just below the 5% threshold is Merchants (MRCH), on a yield of 4.9%.

RENEWABLES TRUSTS ‘EXPENSIVE’

Several infrastructure-focused trusts, including some in the renewables sector, offer generous yields. As Stifel points out, the high valuations of these increasingly fashionable trusts is a risk to note.

‘Renewable sector valuations are at all-time highs, reflecting investor enthusiasm and flows into the asset class. However, headwinds continue to increase with: 1) weak power prices, 2) a corporation tax ‘increase’ and 3) UK inflation being below assumptions.’

Ultimately investors should understand that, in general, higher yields come with higher risks. Don’t simply chase the generous income without understanding how the trust can pay that money to you.

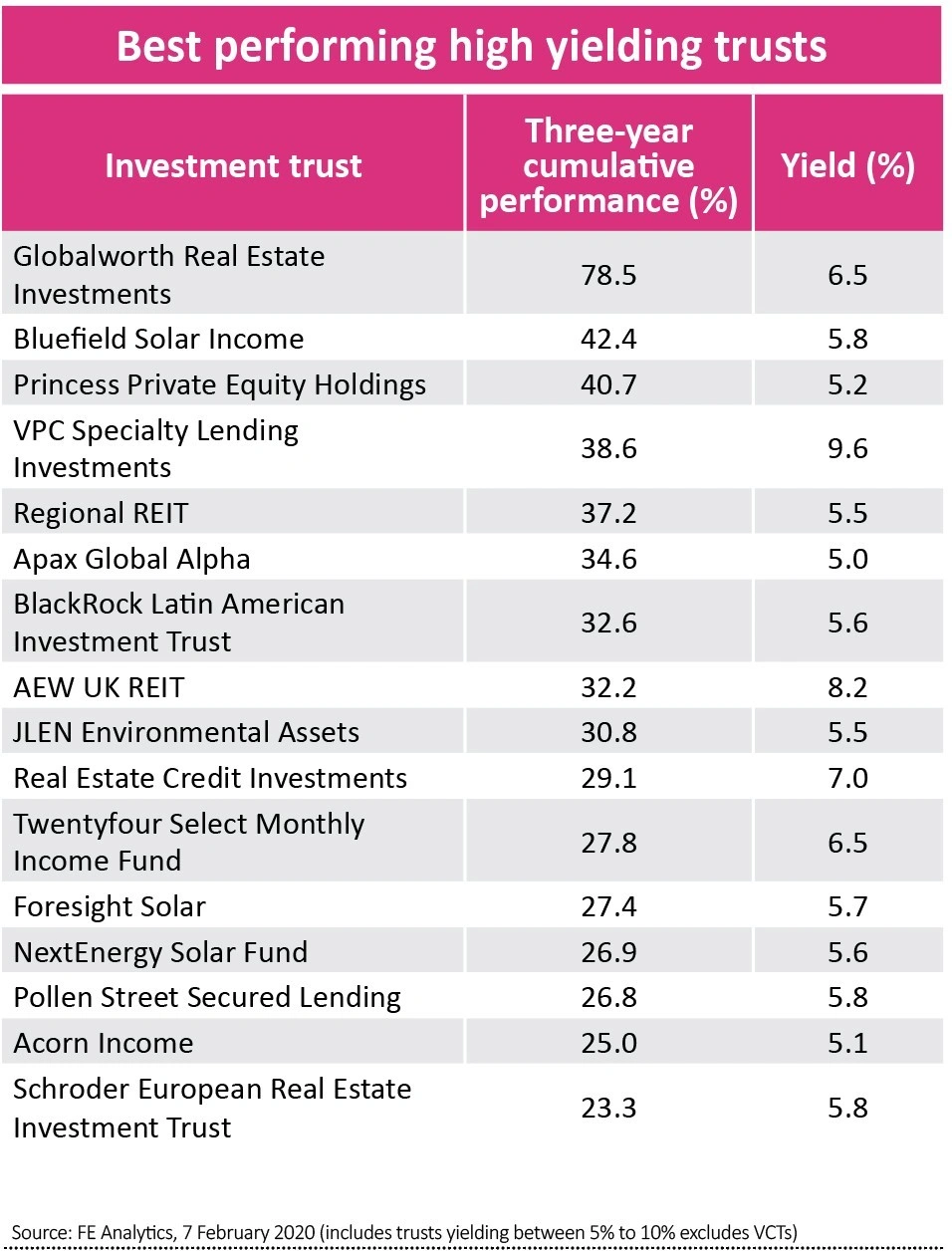

Two high-yielding trusts to buy

AEW UK REIT (AEWU) 99p

Dividend yield: 8.2%

Frequency of dividends: Quarterly

Premium to net asset value: 6.2%

(Source: FE Analytics, AIC)

Steered by Alex Short, the trust aims to pay a covered dividend of 8%, with income generated from a portfolio of UK regional property assets.

It has a 50% weighting to the industrial sector, targeting good quality, second hand, well-located assets – distinct from prime logistics units which are more expensive and therefore offer lower yields.

It works hard on asset management to grow rent and capital values. The trust is targeting a pipeline of assets valued at £100m, including some select retail assets, so may be raising new cash soon.

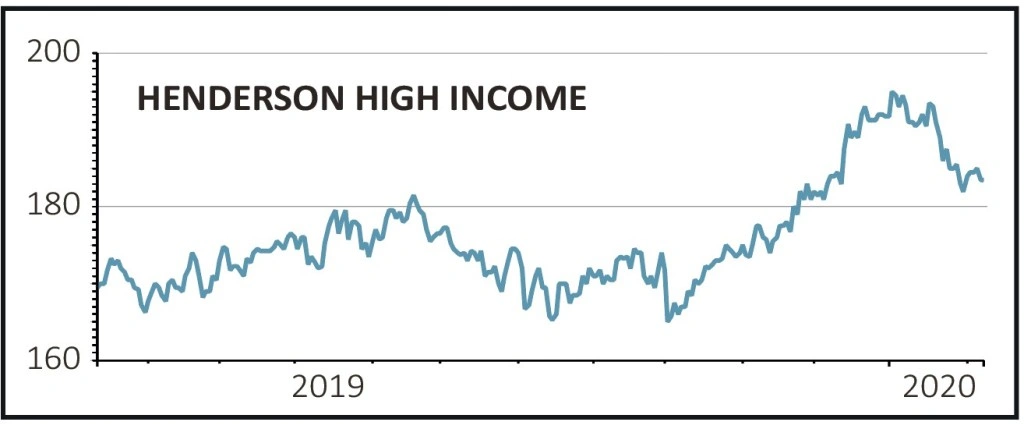

Henderson High Income (HHI)

Dividend yield: 6.6%

Frequency of dividends: Quarterly

Discount to net asset value: 2.2%

(Source: FE Analytics, AIC)

Launched in November 1989, according to QuotedData since inception it has achieved a total return of 14 times the value of an initial investment, compared with 9.4 times for the MSCI UK benchmark.

Like many trusts the company uses gearing which involves borrowing money to access a greater pool of cash for investments. This enables it to enhance and underpin income with some of this money used to buy fixed-interest securities, typically split 20% to 80% between bonds and equities respectively.

There is a focus on quality and manager David Smith sees a sweet spot investing in stocks which yield between 2% and 6%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.