Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Tesla shares can’t continue to motor

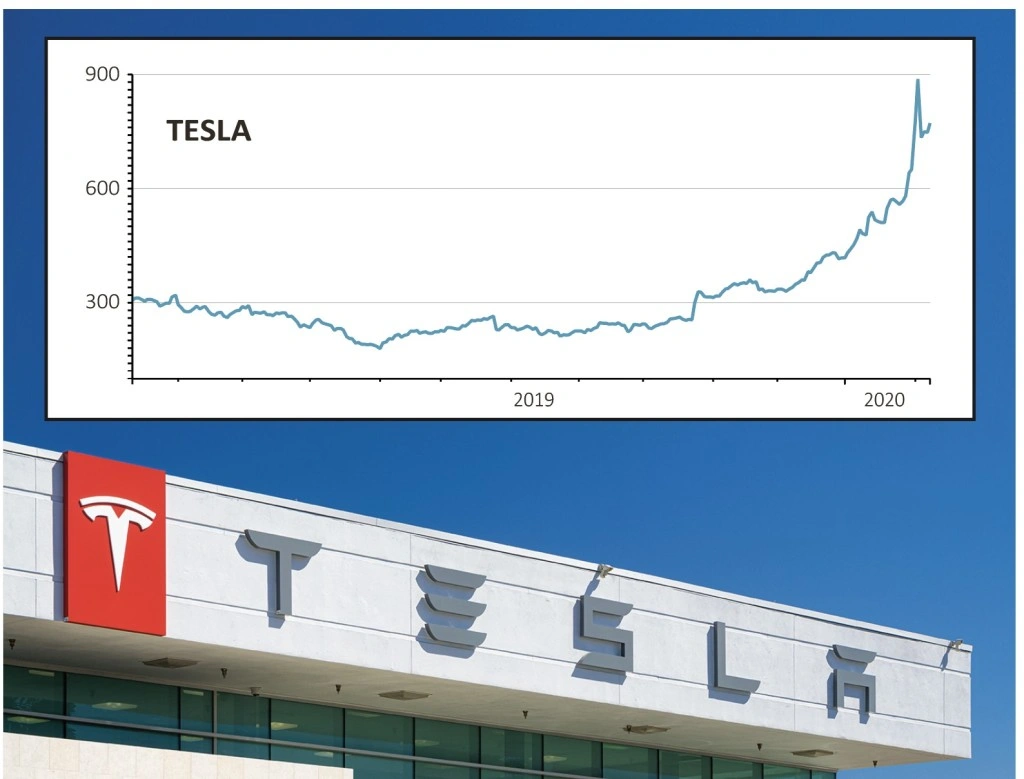

There’s been only one share on the lips of investors over the past week or two; Tesla. The electric car maker seemed to turn a corner with its latest fourth quarter trading update, opening the floodgates on an almighty short squeeze that sent the stock soaring.

Just eight months ago Tesla’s shares were trading below $180, with analysts and investors gripped by serious doubts about the car maker’s future. The most sceptical suggested that it might run out of money altogether and go bust. But Tesla has never been short of supporters and, for many shareholder fans, being part of the Tesla story is more of a cult than a cold-eyed investment.

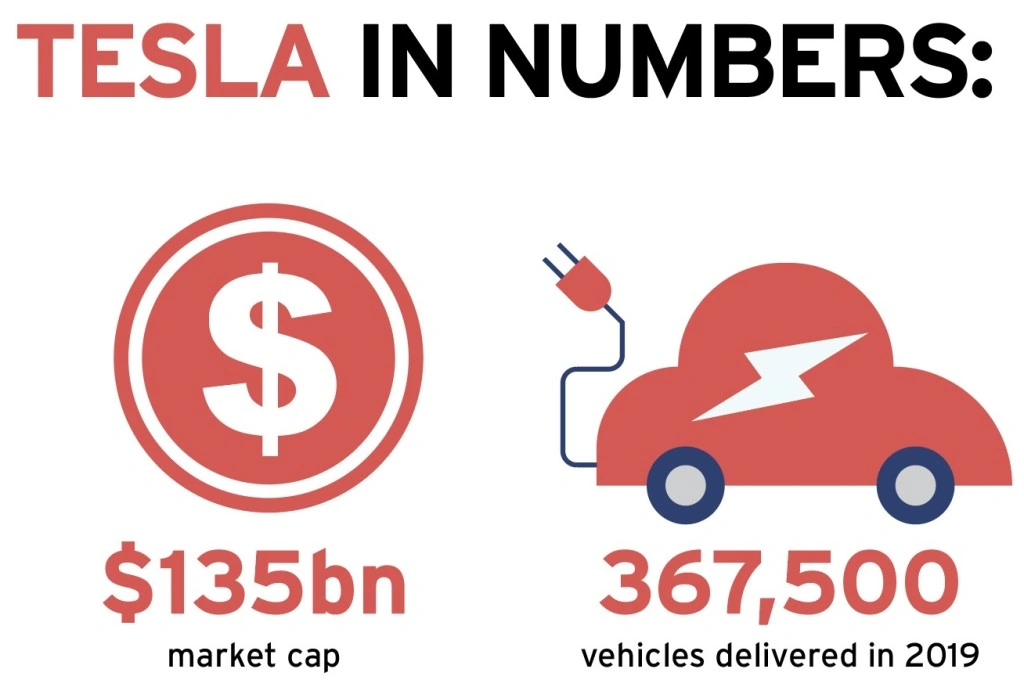

Now on a staggering market value of $135bn, and a 2020 price to earnings (PE) valuation of 185, we believe investors should resist the temptation to follow the crowd and invest in company.

To put that market valuation into perspective, Tesla is now valued at $20bn more than the market caps of Ford, General Motors and BMW put together.

WHAT HAS CHANGED?

A year ago chief executive Elon Musk predicted Tesla would deliver between 360,000 and 400,000 electric vehicles to customers in 2019. Ultimately, according to the company, it delivered around 367,500 vehicles, an impressive 50% jump from 2018. (Though for perspective Toyota produced almost 9m motor vehicles in the year to 31 March 2019.)

Tesla also delivered a record 112,000 vehicles globally during the fourth quarter, significantly topping Wall Street estimates.

What this meant was back-to-back quarters of profit and positive cash flow.

Fourth quarter to end December revenue were $7.38bn from which it made a $105m profit. Adjusted earnings per share of $0.58 beat expectations, although that strips out stock based compensation, not always popular with analysts or investors.

‘While the valuation remains unjustifiable, I think my very long-term view that Tesla won’t survive needs a revisit,’ admitted analyst Richard Windsor in an update on his Radio Free Mobile website.

‘Tesla genuinely fared better than expected on the top line and crucially, continued to generate cash.’

The soaring share price marks something of a victory in Elon Musk’s ongoing battle with short sellers and sceptical analysts who have always fretted over Tesla financial health.

The company is among the most shorted on Wall Street and even if many cynics have been forced to close short positions in recent days to cover themselves, there is still nearly 14% of the firm’s 180.25m shares issued in the hands of short sellers.

Toby Clothier of Mirabaud Securities is among the sceptics. His continues to base his expectations on hard financial data, and it is difficult to objectively disagree that Tesla share price has detached from reality.

He points to weakening market share in Europe and concerns that fourth quarter profit will drift into 2020.

Patrick Hummel of UBS shares Clothier’s view on valuation, but sees little to cap enormous growth for Tesla in the years ahead.

MOST PROFITABLE CAR MAKER

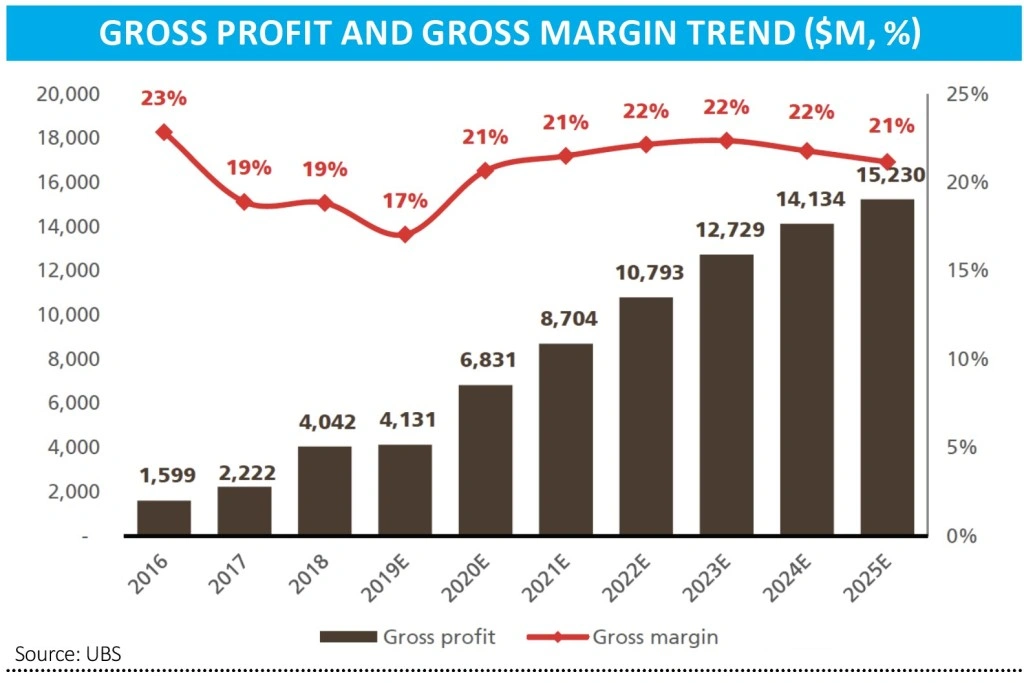

With volumes expected to double by 2022, Tesla can become the most profitable car maker in the world, reckons the UBS analyst.

‘We expect approximately 300 basis points auto gross margin accretion from the localized Model 3 in China and Model Y on likely strong commercial success,’ he said. Part of the reasoning is Tesla’s sustained technological lead. Tesla cars are stuffed full of software and hardware ad it leads the electric car industry in batteries and power train engineering.

Volkswagen has committed to a €40bn investment into its new electric fleet over the next five years and most established car manufacturers acknowledge the enormous cost to get close to Tesla. Perhaps some of these will catch up eventually, but it looks likely to take years.

‘Tesla’s sustained technology lead and mix boost from Model Y and the Cybertruck enable a stable $54,000 ASP trend at the top end of the premium segment,’ said Hummel. ASP stands for average selling price, the per unit price tag of a Tesla car averaged across the range.

Interestingly, Tesla’s key performance indicators, or KPIs, show much higher efficiency than incumbent car makers as there is no drag from any legacy business. ‘Tesla should meet and exceed margins and cash generation the premium manufacturers enjoyed in their best days,’ said Hummel.

He calculates that at between $3bn and $5bn of annual free cash flow on an 8% to 10% operating profit margin, yet Hummel believes that all of the above and more are taken for granted at the current share price.

Tesla shares now discount 1.6m vehicles being sold in 2025 versus the 367,500 in 2019, on an 11% operating margin, calculates the UBS analyst.

VALUING TESLA AS A CAR MANUFACTURER, OR NOT

The biggest challenge for more sober investors is coming to terms with the idea that Tesla should not be valued as a car company at all, but a manufacturer of highly advanced bits of mobile technology.

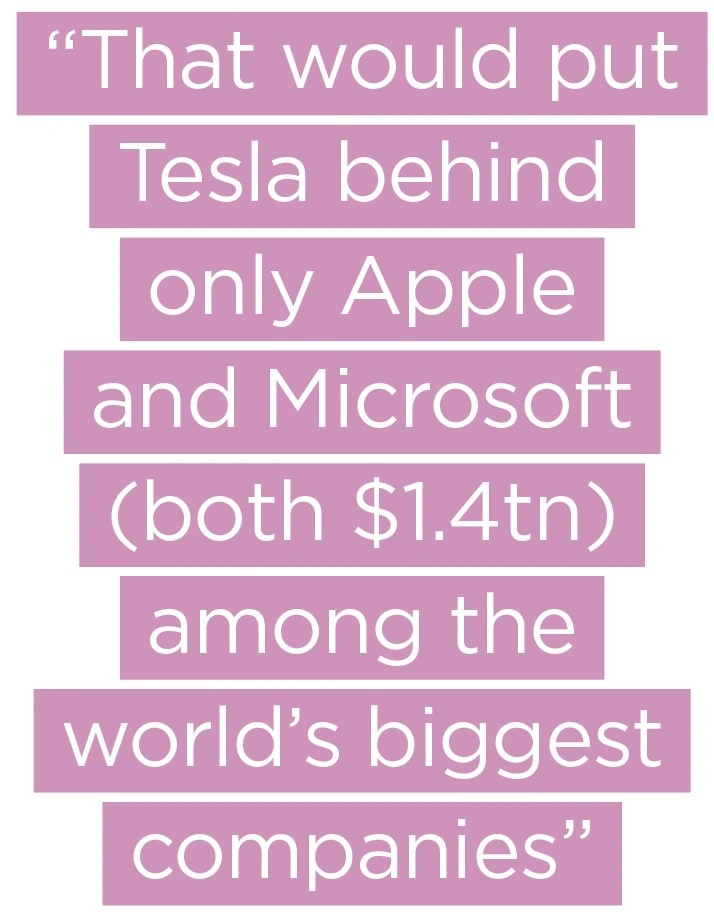

This is how New York-based researcher Ark Invest sees the story, one of Tesla’s biggest and most bullish fans. In a note to clients on 31 January 2020 Ark put forward its case for the share price to hit a staggering $7,000 by 2024, which would give the firm a market value of $1.3trn.

That would put Tesla behind only Apple and Microsoft (both $1.4trn) among the world’s biggest companies.

That’s Ark’s base case valuation forecast. The analyst’s bear scenario still sees Tesla stock roughly doubling to $1,500 by 2024, with $15,000 its bull case play.

Those sort of wild predictions make great headlines but sensible investors should not invest in Tesla because of them. This is a company that has endured many production and delivery problems in the past and missed forecast targets because of them.

With the coronavirus creating plenty of global supply chain uncertainty, there is a very good chance that a hefty chunk of the Tesla fluff will get blown off the shares over the coming months. Reassessing the valuation story then would be more sensible.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.