Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat do I need to know about the Scottish budget?

I know everyone is focused on the main UK Budget next month, but is there anything I need to be aware of from the Scottish Budget? I live in Ayrshire and have taxable income of £45,000 a year and pay around £5,000 a year into my ISA. I also receive about £3,000 in dividends via my general investment account.

Hamish

Tom Selby, AJ Bell Senior Analyst says:

The Scottish Budget was published on 6 February, setting out the key spending and tax priorities north of the border for 2020/21.

For savers and investors in Scotland, the event has taken on extra significance since 2017, when former finance minister Derek Mackay – who resigned just before this year’s Budget – announced sweeping reforms to income tax bands.

The move was an attempt to make the tax system fairer by placing a greater burden on higher earners and represented the first separation of income tax rates between Scotland and the rest of the UK.

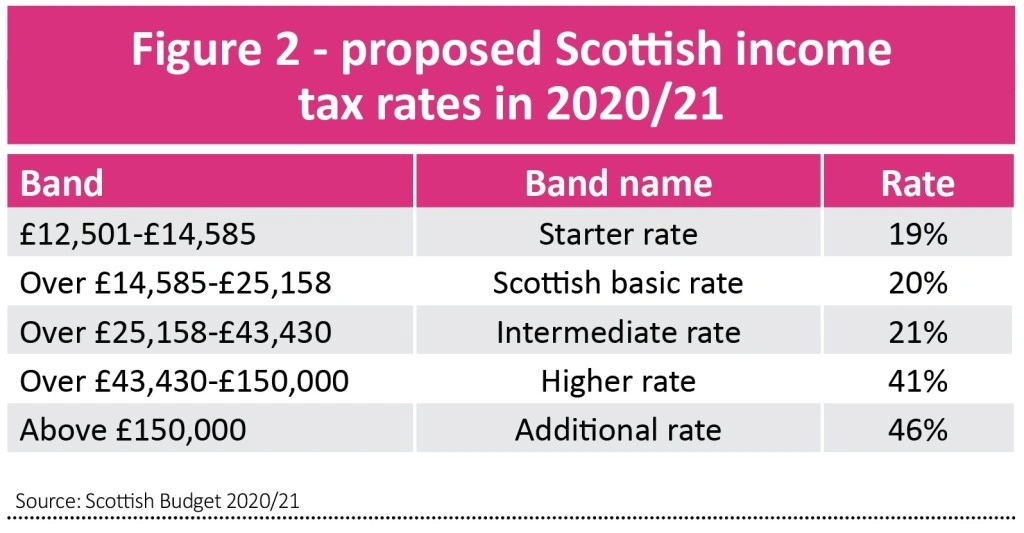

There are now five different tax bands in Scotland – starter-rate (19%), basic-rate (20%), intermediate-rate (21%), higher-rate (41%) and additional-rate (46%).

This compares to the rest of the UK where there are just three tax bands – basic-rate (20%), higher-rate (40%) and additional-rate (45%).

Figure 1 shows the income tax bands rates in Scotland for the current tax year (2019/20), and figure 2 the proposed changes in 2020/21.

So no major shifts, although note the starter and basic-rate bands have increased in line with inflation, while the higher and additional-rate bands have been frozen.

In your case this shouldn’t make a material difference, but for those who were close to one of the higher-rate bands who enjoy a pay rise it will push them into paying a bit more tax.

While the product you choose to save in will depend on your goals and personal circumstances, it’s worth noting that higher and additional-rate taxpayers in Scotland can get an extra one percentage point in tax relief boost by saving in a pension versus those in the rest of the UK.

Intermediate-rate taxpayers are also eligible for a bit of extra tax relief, although those in a relief at source scheme such as a SIPP need to claim this back from HMRC.

You should also consider whether your dividend paying investments could be held more tax efficiently in a SIPP or ISA. Both allow you to receive dividends tax-free, whereas outside a tax wrapper any dividends above £2,000 will face a tax charge of either 7.5% (starter, basic or intermediate-rate taxpayers), 32.5% (higher-rate taxpayers) or 38.1% (additional-rate taxpayers).

DO YOU HAVE A QUESTION ON RETIREMENT ISSUES?

Send an email to editorial@sharesmagazine.co.uk with the words ‘Retirement question’ in the subject line. We’ll do our best to respond in a future edition of Shares.

Please note, we only provide guidance and we do not provide financial advice. If you’re unsure please consult a suitably qualified financial adviser. We cannot comment on individual investment portfolios.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.