Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineReasons to keep buying shares in Tesco

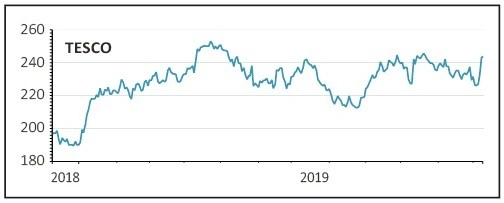

TESCO (TSCO) 243.2p

Gain to date: 2.7%

Original entry point: Buy at 236.9p, 23 May 2019

In anticipation of a tough summer compared with last year’s abnormally strong sales, in the spring Tesco (TSCO) reduced its number of product lines and put more resources into its own-brand offerings, but growth has remained elusive. UK like-for-like grocery sales were down 0.3% in the first half, although this was partly offset by strong growth at its wholesale business Booker.

Since the summer the priority for chief executive Dave Lewis has been to streamline the business before handing the reins to Ken Murphy who joins from Walgreen Boots Alliance next year.

In September, the mortgage business was sold to Lloyds (LLOY) for £3.8bn, a slight premium to its £3.7bn book value. The sale not only generated a healthy cash inflow, allowing Tesco to reinvest in prices to maintain market share, it also meant it no longer had to put capital behind a business with minimal profits.

This week Tesco confirmed it is considering the sale of its Malaysian and Thai businesses after receiving an unsolicited approach. The Asian businesses should fetch a good price, allowing the grocer to continue focusing on its home market.

With consumer confidence subdued due to election uncertainty, Britain’s biggest retailer is in pole position to benefit once spending picks up again.

SHARES SAYS: We continue to back Tesco in the battle for shoppers’ wallets. Buy.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.