Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine2020 outlook: 10 big questions for the year ahead

It feels like we are at a major turning point for markets. This year has been dominated by concerns about the US/China trade war, a slowdown in the global economy, Brexit and whether equity markets have peaked.

Next year it feels like we could get more clarity over the trade war and Brexit which in turn might help to provide some answers over the direction of the global economy and how investors could best make positive returns.

In this article we’ve pulled together some of the most important questions on investors’ minds concerning these topics and added a few more questions which we think people will be asking in 2020.

WILL THE US STOCK MARKET DELIVER ANOTHER YEAR OF STELLAR RETURNS?

US stock markets have posted unusually strong returns so far this year. The S&P 500 Composite index is up 26% compared to an average annual return of 8% since the index started in 1957 up to the end of last year.

The biggest driver has been the change in attitude of the Federal Reserve, which switched from raising rates in the first quarter to cutting rates and since then has been perceived as ‘having the market’s back’. Investors know that at the first sign of market stress the Fed will cut rates.

That situation is likely to persist into 2020, but there are growing headwinds meaning gains next year are likely to be less spectacular.

A key event in 2020 is the US presidential election. Even if Donald Trump wins a second term, the Democrats are still likely to control the Senate and will seek to raise corporate taxes, denting profits. Rising labour costs are also likely to eat into earnings.

Progress on a trade deal with China is another potential stumbling block. Economists at Goldman Sachs estimate that the impact of the trade war this year has been to knock 0.4% off US growth.

While US voters support Trump taking on China over its ‘unfair’ trade practices, there is a fundamental difference at stake. As JP Morgan’s chief strategist Karen Ward says, China believes in industrial policy, the US doesn’t.

The US consumer is also likely to be in focus next year. Consumer spending is crucial to the health of the US economy. Happily the household savings rate of 8% is comfortably above the 20-year average of 6%, while the fall in mortgage rates thanks to Fed rate cuts has reinvigorated the housing market.

However consumer confidence has slipped in the past few months and a weak stock market risks creating a ‘doom loop’ of falling confidence and falling share prices.

The final headwind is valuation. On a cyclically-adjusted price-to-earnings (CAPE) basis, the US market has only been more expensive than it is currently on two occasions: before the 1929 Wall Street crash and before the 2000 tech bubble burst.

WILL CORPORATE EARNINGS CATCH UP WITH EQUITY MARKETS IN 2020?

The US tends to set the tone when it comes to equity markets, and so far 2019 earnings are setting a low bar to beat in 2020. The chart shows that reported earnings growth has been slowing since January 2017 if you ignore the one-off tax break that boosted 2018 earnings.

Investors are clearly eying the lush-green pastures of 2020 and resumption in global growth once the US-China trade war abates.

We don’t know yet how the rest of 2019 will pan out, but the weakening trends are in stark contrast to the optimism built into prices.

Current consensus estimates have earnings per share growing around 10% for next year down from around 13% earlier in the year. Goldman Sachs thinks it will come down further to 6%, but doesn’t see it as a problem for stocks.

However, one sign that should make investors ponder such rosy forecasts is the rough 30% reduction in share buybacks this year. In the first quarter of the year companies purchased around $900bn worth of shares, double the amount of dividends paid out to investors. That has since fallen to $657bn.

Historically, falling buybacks have been accompanied by falling stock prices as the chart illustrates.

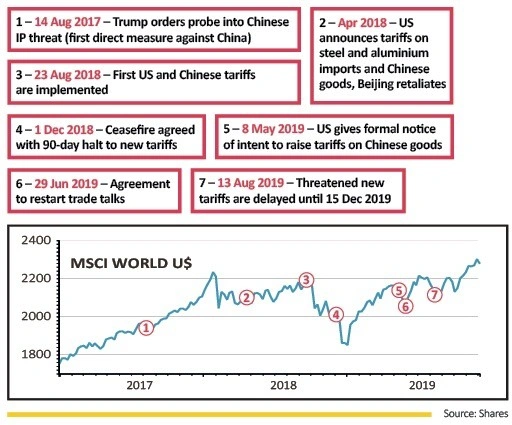

WILL THE TRADE WAR EVER GET RESOLVED?

The answer likely hinges on the unpredictable actions of Donald Trump. He said in early December 2019 that a trade agreement with China could wait until after November 2020’s presidential elections.

This undermined hopes that the trade war which has dominated the market mood since early 2018 would be resolved soon. Investors, who had already seen the markets price in a so-called ‘phase one’ agreement between Washington and Beijing, will hope it is merely a negotiating tactic to squeeze more concessions out of China.

Tariffs scheduled to be implemented on Chinese goods from 15 December will offer an early test of Trump’s intentions. But if the US leader means what he says when he describes his country as doing ‘very well’ from the trade war, then there is a clear risk of an escalation.

This could include the $7.5bn worth of tariffs being readied on imports from Europe in response to illegal subsidies for European aircraft maker Airbus, as well as threatened retaliation to French taxes on US tech companies.

On the flip-side, the incentive for Trump in dialling down tensions is to keep the economy on course, thereby boosting his re-election hopes at the end of the year.

CAN GOVERNMENTS PICK UP THE SLACK FROM CENTRAL BANKS?

In the wake of the financial crisis the world’s central bankers have looked to keep growth on track through the availability of cheap cash, pursuing loose monetary policies.

They have busily lowered interest rates and introduced so-called quantitative easing, increasing money supply by buying bonds. Now they want governments to do their part through fiscal interventions. This means increasing state spending in areas like infrastructure to help give the economy a boost.

Christine Lagarde, the newly installed chief of the European Central Bank, recently called for Eurozone countries with the necessary capacity, such as Germany and the Netherlands, to invest more in infrastructure, education and innovation.

In some respects central bank policy has set the stage for this increase in spending. Investment bank JPMorgan observes: ‘Low interest rates are an enormous cash windfall for governments, and could encourage governments to turn on the fiscal taps.’

If this happens there is the potential for a double dividend as jobs are created and productivity is improved through the extra investment.

Increased borrowing would be likely to play a big part but higher government spending raises the possibility of increased corporate taxation down the line to help foot the bill. This could undermine business confidence and act as a constraint on growth longer term.

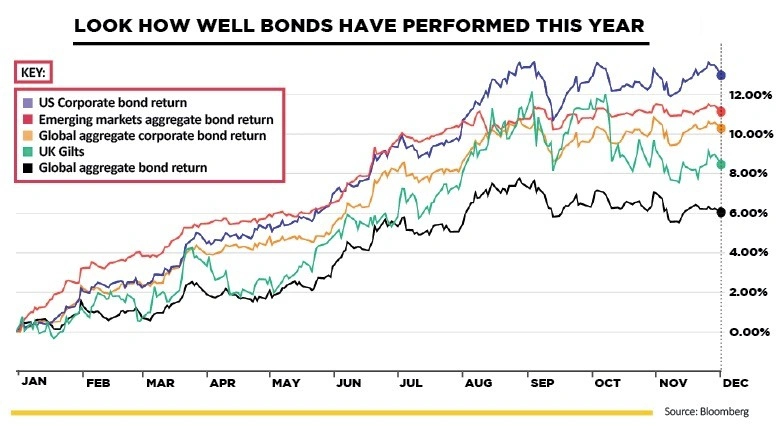

CAN BOND PRICES CONTINUE TO RISE AFTER SUCH A GREAT 2019?

Bonds normally act as a safety zone for investors and tend to do well when equities enter a down phase. However bond strength in response to an equity market wobble last autumn continued into the beginning of this year resulting in strong returns across the fixed income spectrum, from government bonds to corporate and high yield.

Continuing US-China trade tensions and Brexit wrangling has had a dampening effect on global trade and consequently most economists are now predicting slower growth. Meanwhile inflation expectations remain subdued, resulting in little or no pressure on bond yields.

Some investors see a constructive resolution of these risks as a catalyst for the resumption of global growth which would see bond yields rise and prices fall. But some bond fund managers are less optimistic about growth.

Mike Riddell of Allianz Global Investors thinks the risks are rising. He tells Shares: ‘we continue to believe that we are at, or approaching, the end of the economic cycle and the risk of a US/global recession next year is still very real.’

In terms of what to avoid, it’s all about what’s priced in and for Riddell the extra yield on a corporate bond over a government bond is now very close to the historically tight levels seen in June 2007, immediately before the last crisis began.

‘In light of this, near record low levels of credit spreads makes no sense and we’re avoiding corporate debt at the moment,’ he says.

Chris Bowie, a bond fund manager at TwentyFour Asset Management, concurs and says now is not the time to reach for risk in high yield, emerging markets, nor private credit fixed income. He adds: ‘Roughly one-fifth of our portfolios are in government bonds to protect capital and lower volatility.’

Clearly it will be more important for bond fund managers to be selective in 2020, with government bonds again reverting to their traditional ‘haven’ status, while corporate and high yield will face more challenging conditions.

WILL IT BE HARDER TO FIND DECENT SOURCES OF INCOME IN 2020?

Yield scarcity will be one major challenge facing investors in 2020. The sustainability of UK equity income streams has been called into question, with underlying dividends across the market falling by almost 3% on a constant currency basis during the third quarter of 2019 – the worst quarterly performance for three years.

While the latest Link Group UK Dividend Monitor revealed overall UK dividend growth of 6.9% over the third quarter, this was driven by special dividends and exchange rate gains due to the depreciation of sterling.

Brendan Gulston, co-manager of the Gresham House UK Multi Cap Income Fund (BYXVGS7), points out that with more than half the FTSE 100’s dividends coming from just 10 companies, ‘most UK equity income strategies are disproportionately invested in a relatively small number of mega-cap stocks’.

Don’t assume that very large companies are dependable dividend payers. Their dividends can still be volatile, as highlighted by the 40% dividend cut for Vodafone (VOD) earlier this year.

Investors seeking dividend diversification may want to look to the small and mid-cap market, where Gulston says he is witnessing ‘numerous under-researched and under-the-radar companies displaying considerable dividend generation potential over the coming years’.

Calum Bruce, investment manager at Ediston Property Investment Company (EPIC), believes real estate should remain appealing to investors as a way to access strong, sustainable income.

‘With many property investment trusts trading at discounts in the region of 10% to 20%, and with yields in the region of 5% to 7%, one has to question at what point sentiment towards Brexit and retail has been more than fully reflected in the share price of select investment trusts.’

HOW BIG COULD ESG INVESTING GET?

The answer is very big. The growing consensus in investment fund circles is that environmental, social and governance (ESG) investing will be the norm within five years, that is to say part of mainstream investing.

The drivers are regulatory changes from governments around the world and, far more crucially, rapidly increasing demand particularly from women, millennials and high net worth individuals.

A Bank of America report predicts a ‘tsunami of assets’ is poised to flow into ESG investments, with over $20trn of growth in ESG funds in the US alone over the next two decades, equivalent to the size of the S&P 500 today.

Exchange-traded funds (ETFs) are expected to flourish as more ESG-specific indices are created.

Rebecca Healy, head of market structure at brokerage Liquidnet, says ESG can no longer be seen as an investment ‘fad’ and is now the way investors determine if a company’s business model is sustainable.

She explains: ‘Whether that is the automotive company that is investing in the latest active safety technology or a technology company that offers the largest database of academic research at free or low cost to developing nations, or companies investing in electric charging infrastructure to make cities more efficient.

‘This isn’t about hugging trees. It’s about identifying the economic success stories of the future.’

SHOULD OILS, BANKS AND INSURERS TRADE ON PERMANENTLY LOW MULTIPLES?

In recent weeks we have discussed the possibility of ‘value’ stocks re-rating at the expense of ‘growth’ stocks, and market trends would suggest there is life in the value strategy yet.

However, some sectors look to be so structurally challenged that despite their lowly price-to-earnings (PE) multiples, the chances of them reverting to their former ratings are slim to put it mildly.

Two sectors which have undergone a major de-rating in the past decade are oils and banks. Just as the days of Brent crude trading at $100 a barrel look unlikely to return, significantly higher interest rates seem improbable for now.

For oil companies there is the added problem that their reserves may no longer be worth what they were previously. Spanish producer Repsol recently wrote down the value of its assets in line with a ‘lower oil and gas price scenario consistent with the Paris Agreement’s climate goals’. Pressure for others to do the same will surely grow.

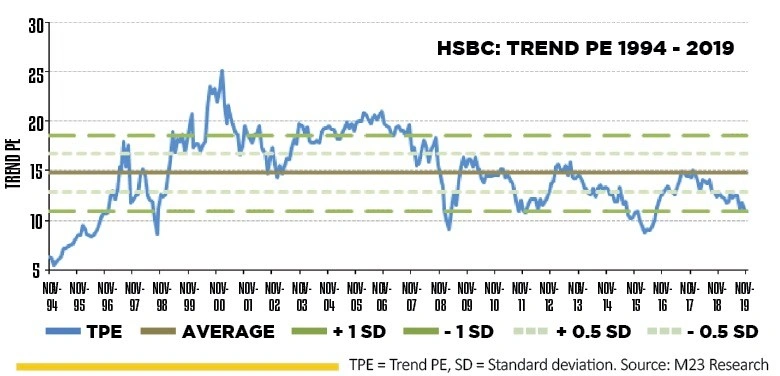

On a cyclically-adjusted price-to-earnings (CAPE) basis, shares in FTSE 100 heavyweight BP (BP.) have traded between 10 and 15 times earnings at best over the past 10 years and look like staying there compared with 20 to 25 times or more a decade earlier.

It’s a similar story for HSBC (HSBA), another major FTSE stock, which has spent most of the past decade trading just above 10 times cyclically-adjusted earnings with rare forays to 15 times compared with previous highs of 25 times earnings.

Given the growing frequency of climate-related disasters and bigger than expected catastrophe claims, it is worth asking whether insurers such as Beazley (BEZ) and Hiscox (HSX) will be able to sustain their former rating of 15 to 20 times cyclically-adjusted earnings in the years to come or whether theirs too is now a structurally-challenged business.

Where's the comment on Brexit?

We haven’t forgotten about Brexit in our 2020 outlook. We’re simply waiting for the UK general election result in order to have a better handle on how Brexit might play out. We will provide commentary in next week’s issue of Shares (19 Dec) alongside information on how the party or parties which prevail in the election could impact markets over the coming months.

WILL VALUE INVESTING MOUNT A BIG COMEBACK IN 2020?

For a long time value investing – looking to buy shares in companies which trade on lowly valuations – has been out of fashion as investors have focused instead on buying companies which can deliver growth, no matter how expensive they are.

There are signs that could change in 2020, with the performance of value stocks picking up in recent months.

The chief executive of value investment specialist Oldfield Partners, Jamie Carter, sums up the situation: ‘The recent decade-long underperformance by value has been the worst since the Great Depression, but value outperformed superbly in the years that followed that period.’

There have been false dawns before in 2016 and late 2018 when value held sway for a short period before growth stocks recovered their dominance.

Contrarian fund manager Alastair Mundy, who steers Investec UK Special Situations (B61JXN1), says: ‘The biggest boost for long-term value recovery will be bond yields going up and bond yields are clearly at very low levels so I think the odds are on my side there.’ He believes rising inflation and the flood of government debt in the fixed income market could be a catalyst for yields going up.

WILL THIS BE THE YEAR WHEN MULTIPLE INVESTMENT TRUST BOARDS LOSE PATIENCE AND SACK UNDERPERFORMING MANAGERS?

The setbacks involving Neil Woodford’s various funds in 2019 have been an eye-opener for the funds world and have also been a reminder that investment trusts have the power to sack the fund manager if they are not meeting expectations.

Active funds are already facing competitive pressure from passive exchange-traded funds and now they’ve also got reputational issues to address. It seems highly likely that a large number of investment trust boards will no longer put up with underperforming managers and so we could see quite a few changes in 2020.

Ones to watch include Mark Barnett-managed Perpetual Income & Growth (PLI) whose chairman Richard Laing last month said the board was ‘very sensitive to shareholder concerns about continued weak results’ and that it was closely monitoring efforts by Invesco to improve performance.

Aberdeen Standard Equity Income Trust (ASEI) has described its 2019 performance as ‘a considerable disappointment’.

Despite saying a -15.1% share price total return versus 2.7% gain from the FTSE All-Share ‘a very poor result and there is no point in pretending otherwise’, the board is giving manager Thomas Moore another go at getting the fund back on track. He’s probably got one chance to improve performance before more serious thoughts are given to the future management of the trust.

Where could you make money in the coming years?

Financial data specialist Morningstar believes the best place to make money in the coming years could be UK, Korean, German and Japanese stocks. In contrast it believes the US market has already had its strong run and could deliver much lower returns going forward.

Looking at the valuation-implied returns for the next 10 years, Morningstar believes you could get approximately 7% a year from UK equities, 6% a year from German equities and less than 1% from US equities.

‘The German stock market has been hurt by auto tariffs and Brexit, but we’ve seen good changes with cost savings and think some of the price action has been overdone,’ says Emma Morgan, a portfolio manager at Morningstar.

‘You would normally expect to make 6% to 8% from the US market but it looks so overvalued at the moment that you are unlikely to get that return going forward. UK equities are supported by a large dividend yield and you’re getting some growth and inflation as well.’

Lyxor Asset Management favours European equities for 2020, saying there is an improved economic backdrop and valuations are lower than the US.

Investors can get exposure to the aforementioned regions through exchange-traded funds or actively-managed funds.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.