Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFund managers’ best and worst stock calls in 2019

It is always fascinating to get insight into fund managers’ views on their stock picking decisions and so we’ve spoken to range of managers about their best and worst calls in 2019.

The managers in this article discuss a range of stocks on both the UK market and ones listed overseas.

WILL JAMES

Deputy head of European Equities at Aberdeen Standard Investments

MEDIOBANCA – GOOD CALL

‘European banks in aggregate have not had a good time in 2019 given the uncertain growth outlook and continued pressure on interest rates. Our view has been that the odd phoenix should be able to rise from the ashes of an industry that suffers from overcapacity, regulatory headwinds and lack of revenue growth.

‘Mediobanca is one such ‘scarce’ asset. It is ironic and some would say remarkable that an Italian bank has managed to make it into the top performers’ list. However, excess capital, relative interest rate insensitivity, ability to reposition the bank and drive growth, and pay a high, sustainable and growing dividend, allowed Mediobanca to fly high in 2019.’

UMICORE – BAD CALL

‘We were caught out by the profit warning from chemicals group Umicore earlier in 2019.

‘Having been proved right around Umicore’s technological prowess with regards to the nascent hybrid and electric vehicle industry and enjoying great performance from the shares, we failed to properly appreciate how much the market had extrapolated the growth.’

CHARLES LUKE

Fund manager of ASI UK Income Equity (B0XWNB4)

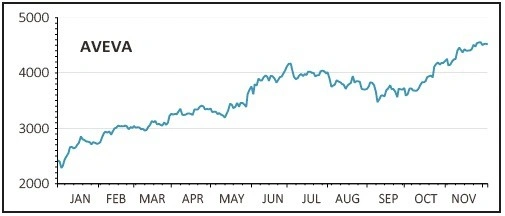

AVEVA – GOOD CALL

‘The merger of industrial software company Aveva (AVV) with Schneider’s software business provided the enlarged company with a larger product set, broader industrial vertical targets and wider geographic exposure.

‘Given the strong revenue and cost synergies, together with a supportive end-market backdrop, Aveva’s trading updates were generally accompanied by earnings upgrades together with a re-rating which resulted in a strong share price performance over the year.’

SAGA – BAD CALL

‘We owned a small holding in Saga (SAGA) given its attractive dividend yield, strong brand and the potential to replace its capital intensive underwriting earnings with earnings from broking and its cruise operations.

‘Unfortunately, we were wrong about the strength of the company’s brand and its resonance with its customer base and the impact of the highly competitive and commoditised UK home and car insurance market.

‘Given a stretched balance sheet, a dividend cut and a very significant change to the original investment case, we sold the holding immediately after it issued a profit warning in April.’

SIMON GERGEL

Portfolio manager of Merchants Trust (MRCH)

GREENE KING – GOOD CALL

‘Greene King is one of the UK’s largest pub companies with nearly 3,000 pubs. Like many UK consumer-related companies, the shares were attractively valued at the start of the year, as investors were concerned about the economic risks to the UK from the Brexit uncertainty.

‘There were also some concerns about a more competitive trading environment in the food and beverages industry.

‘We were particularly attracted to Greene King’s strong asset base, with brands such as Chef & Brewer and Hungry Horse, and beer brands like Green King IPA and Old Speckled Hen. The company also has a strong management team and a solid long term record of growth.

‘The low valuation of the shares prompted a takeover offer from the private company of one of Hong Kong’s richest men. This led to the shares rising sharply.’

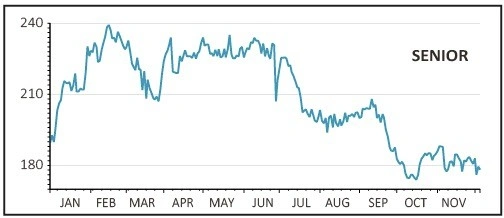

SENIOR – BAD CALL

‘Senior (SNR) is a manufacturer of aerospace and industrial equipment with a high exposure to the large civil aerospace manufacturers. The company has a long order book with greater sales per plane on most of the new and growing Boeing and Airbus programmes.

‘The company has been hit by a number of different issues this year. Most notable has been the grounding of Boeing’s 737 Max aircraft after two tragic accidents. But there has also been an impact from a slowdown in certain industrial markets and a non-renewal of some historic contracts.

‘In combination, these factors have had a significant impact on the company’s profit expectations, and this has led to the shares being one of the weakest performers in our portfolio this year.’

JASON PIDCOCK

Fund manager of Jupiter Asian Income (BZ2YMT7)

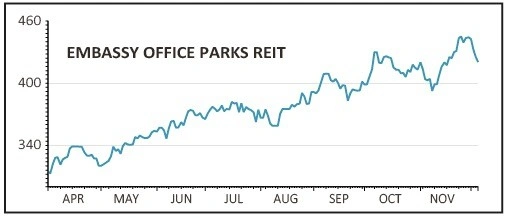

EMBASSY OFFICE PARKS REIT – GOOD CALL

‘We bought into office landlord Embassy Office Parks REIT earlier this year – the first REIT to list in India (and the only one to date). We liked the opportunity so much we became anchor investors and bought in the aftermarket until we’d established a significant (for us) position.

‘It floated in April at 300 rupees and the shares now trade at 442 rupees. We’ve also had two dividend payments. Embassy has so far outperformed the Indian market by 45%.’

HONG KONG STOCK EXCHANGE – BAD CALL

‘We considered buying shares in Hong Kong Stock Exchange at the end of September after it had made an indicative bid for London Stock Exchange (LSE).

‘We met the management and were impressed but thought they might raise their bid and waited to see if we could get a better entry price. It didn’t happen.

‘HKEX abandoned its bid for LSE and the shares have rallied from HK$222.60 on 25 September to HK$247.60.’

MIKE KERLEY

Fund manager of Henderson Far East Income (HFEL)

ANTA SPORTS – GOOD CALL

‘China branded sportswear Anta Sports – which has the rights to the Fila brand in parts of Asia – is a stock we owned through 2019 on the basis of three key themes – government support for leisure, exercise and heathier lifestyles; aspirational purchases as incomes rise; and finally, that local brands would take market share from foreign brands as quality improves and pricing remains competitive.

‘Anta has the third largest market share in sports apparel and has taken market share from the leaders, Nike and Adidas.’

LEND LEASE – BAD CALL

‘We invested in Australian property development and engineering contractor Lend Lease for its urban regeneration projects in Australia, Europe and the UK and for its exposure to increased infrastructure spending, primarily in Australia but also worldwide.

‘Unfortunately, some ill-conceived legacy engineering projects in Australia led to a series of provisions which were unexpected and badly communicated to the market which saw the stock underperform.’

LAURA FOLL

Co-fund manager of Lowland (LWI)

XP POWER – GOOD CALL

‘We invested in XP Power (XPP) at the beginning of this year for around £20 a share; they now trade around the £29 level. XP makes power converters for a range of industries – healthcare, semi-conductors as well as more general industrial applications.

‘It has always generated good operating margins and in our view the management team are excellent, but it had de-rated hugely towards the end of 2018 because of concerns about the semi-conductor cycle and the possible earnings downgrades that would result.

‘In our view the long-term quality of the business was such that this looked like an interesting entry point and we built a position.’

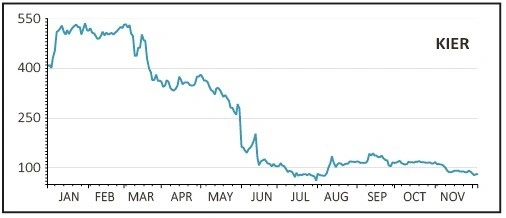

KIER – BAD CALL

‘Our worst new position in 2019 was a small stake in Kier (KIE) at the start of the year, following the rights issue.

‘We felt that the balance sheet issues were being addressed, and under a new CEO who wanted to simplify the business and take costs out that Kier could be well positioned for a recovery from a low valuation.

‘What I underappreciated was the scale of working capital outflow for this type of business when customers and suppliers lose trust. What that meant was the rights issue proceeds were quickly offset by the working capital outflow that occurred, leaving ongoing balance sheet stretch.’

TREVOR GREEN

Head of UK equities and a senior portfolio manager at Aviva Investors

AVEVA – GOOD CALL

‘Aveva is a global leader in engineering and industrial sector software which merged with Schneider Electric Software in 2018. In this case bigger seems to be better, with the firm delivering very strong earnings this year, assisted by the ongoing move by its customers to embrace digitalisation.

‘Recurring revenue has increased for the business and investors have rewarded the company in 2019 with a higher rating.’

IOMART – BAD CALL

‘web hosting cloud computing company Iomart (IOM:AIM) has strong end market growth drivers as the ever-increasing demand for more computer power, storage and connectivity gives it an ever larger market to play for.

‘Despite this situation, the share price has struggled since I invested in late January, with earnings forecasts drifting in 2019 as the business has made increased investment towards targeting larger and more complex contracts.

‘This year will go down as one of consolidation and investment, with investors looking to next year and beyond for this investment to pay off.’

LUCY MACDONALD

Portfolio manager of Brunner Investment Trust (BUT)

TAIWAN SEMICONDUCTOR MANUFACTURING – GOOD CALL

‘The growth prospects for Taiwan Semiconductor Manufacturing are driven by increasing demand for smaller, faster processors across a widening range of industries, in particular 5G smartphones and artificial intelligence computing.

‘It has a leading market position in advanced-node fabrication driving high sustainable returns and a broadening customer base, supplemented by an increase in outsourcing, from Intel in particular.

‘The competitive landscape has improved for TSM with the announcement from Globalfoundries of its suspension of 7-nanometer development.

‘This competitive strength is reflected in gross profit margins around 40%, with a target of 50%. Long term growth forecasts are being revised upwards.

‘At the beginning of 2019, the stock was attractively valued due to short term cyclical factors and offered a yield close to 4%. Over the year the earnings have recovered, surprising on the upside against overly conservative estimates and the stock has seen a re-rating, resulting in a 39% return.’

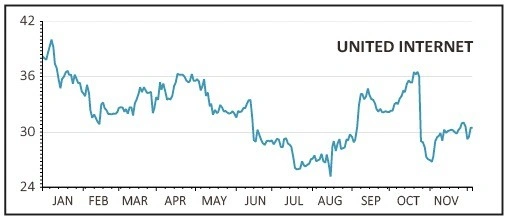

UNITED INTERNET – BAD CALL

‘United Internet provides internet access services to homes and small and medium-sized companies in Germany.

‘The original investment case was based on low capital intensity growth in a relatively concentrated market, with a regulatory background supportive to new entrants. The company demonstrated market share gains and high returns.

‘There was also attraction in the potential stock market flotation of the Business Applications segment of the business, which was seeing strong growth.

‘This core thesis, which worked for a year or two, was broken with the decision of the company to pursue 5G licences at scale, raising concerns about a shifting business model and a lower return on investment.

‘The change in strategy raised questions about the corporate governance and our engagement with the company on the issues were unsatisfactory. We therefore made the decision to sell after collecting a dividend payment. The dividend has subsequently been reduced.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.