Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLondon suffers a sharp decline in the number of IPOs

There has been a dearth of companies floating on the UK stock market this year, perhaps understandably given Brexit-induced volatility.

A mere 25 companies have floated in London so far in 2019, compared with 87 in 2018 and 106 in 2017 excluding listings classified as international offerings where stocks aren’t available to retail investors. The majority have chosen to list on the Main Market with only seven opting to join AIM.

Most notably there has been a scarcity of big names floating in the UK with only four IPOs (initial public offerings) worth more than £1bn.

It’s a different story in US markets with the New York Stock Exchange and Nasdaq attracting a large number of very big floats including Uber, Pinterest and Beyond Meat.

WHY HAVE COMPANIES SHUNNED THE UK?

Jake Robbins, fund manager at Premier Asset Management, suggests there are three reasons why the UK has lagged with IPOs this year.

First, he blames the low valuation of UK markets at the moment, both historically and relative to the rest of the world. ‘If companies are looking to raise capital, doing so in the UK seems like an unattractive place to do it given the low rating that domestic stocks are likely to receive.

‘Companies may be willing to wait until uncertainties such as Brexit, trade wars and economic slowdown have passed in the hope of achieving better valuations in the future.’

Second, Robbins believes that the US market has succeeded by grabbing big name IPOs because that’s where many of the high profile technology disruptors are based. The UK currently doesn’t have these sorts of businesses at the right stage in their development to attract big money from investors.

And third, Brexit uncertainty has prompted companies to delay big decisions which includes floating. Even when they regain confidence, the UK may not necessarily be the listing venue of choice.

‘Given that so many businesses are more global in nature these days, just because companies may have started life in the UK doesn’t necessarily mean they need to list in London. Listing in markets such as the US may offer deeper sources of capital at more attractive terms than the UK so some may be choosing that option instead,’ adds the fund manager.

MORE ISSUES TO CONSIDER

Other reasons may include companies preferring to stay private for longer as well as private equity companies being flush with cash and acquiring businesses off-market that might have been considering an IPO.

The poor performance from some of last year’s IPOs, notably Aston Martin (AML) and Funding Circle (FCH), will have put many people off new market listings.

Oliver Brown, fund manager at RC Brown, says investment banks may also be to blame as they may be advising companies not to list when markets are volatile. ‘Some overseas investors simply see the UK market as uninvestable until there is greater clarity in terms of the UK’s future trading relationship with the EU,’ he adds.

WHAT ABOUT THE IPOS THAT DID HAPPEN?

The average gain from all new market listings this year is 22% but retail investors would have only made a 4.8% average gain if you add up the figures based on the first chance they could buy the shares, namely the market opening price on day one.

Institutional investors tend to be the winners as they are able to take part in an IPO offer and buy at the issue price, yet retail investors typically have to wait until the stock begins trading before they can buy. They often miss out on an immediate bump in the share price.

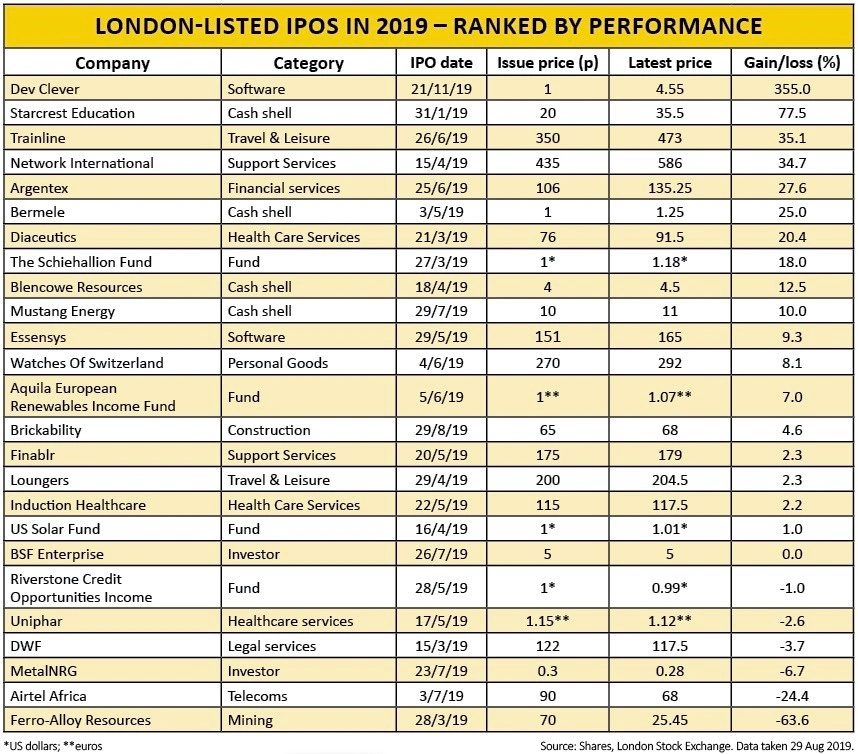

Latest London-listed IPOs

The most recent batch of London-listed IPOs includes Brickability (BRCK:AIM) which floated on 29 August. The AIM-quoted company is a construction materials distributor in the UK and is heavily leveraged to the housebuilding sector. It supplies more than 300m bricks a year as well as products linked to roofing, heating, flooring, doors and windows.

Coming later in September is investment trust JPMorgan Global Core Real Assets (JARA) which has a plan to provide retail investors with access to real asset sectors normally restricted to institutional investors.

It is targeting 4% to 6% dividend yield and a 7% to 9% total return each year. Research group Kepler says its aim is to provide investors with a defensive income stream from high quality real assets with low correlation to major equity markets.

STAR PERFORMERS

The best performing London-listed IPO so far this year is software group Dev Clever (DEV) with a 355% gain.

You could have made significantly more money on this stock if you timed it right and sold in March. At their peak shares in Dev Clever had surged 1,381% from their 1p issue price.

Dev Clever actually started trading at 2.25p versus its 1p IPO offer price, a difference of 125%. Another micro-cap jumping at the market open on the first day of trading was Bermele (BERM), a cash shell hoping to buy a pharmaceutical business, which traded 50% higher on its market debut.

It is quite common to see investors bid up shares in cash shells to far beyond the value of their assets in the hope that such vehicles will find earnings-enhancing acquisitions. This is the best explanation as to why shares in Starcrest Education (OBOR) have shot up by 77.5% since floating in January. It wants to capitalise on China’s ‘Belt and Road’ initiative to economically connect 71 countries and intends to buy companies involved in education services.

Among the larger floats, Trainline (TRN) has done the best with a 35.1% gain since joining the market in June. Close behind is payments group Network International (NETW), up 34.7% in four months.

The highest profile disappointment is Airtel Africa (AAF), the continent’s second-largest mobile operator which has seen its shares slump by nearly 25% since joining the London market in June. First quarter results in July were in line with market expectations so it is hard to know precisely what investors are worried about.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.