Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat Ferguson’s demerger means for UK investors

FTSE 100 plumbing and heating supplies firm Ferguson (FERG) plans to demerge its UK business, which trades under the old Wolseley banner, and make it an independently-listed company.

The UK business made up just 12% of turnover and less than 5% of trading profits in the year to 31 July 2018, with the vast majority of sales and earnings coming from the much bigger US market.

Although there were no details of how or when the demerger is expected to take place, Ferguson shares responded well, adding 3% to £63.23.

The company says that its decision ‘marks the conclusion of a detailed review of the group’s assets over several years’, but we suspect that the arrival of US activist investor Trian in June may have sped up the process.

Trian took a 6% stake in Ferguson, becoming its second-biggest shareholder in one fell swoop, because the firm had ‘market-leading brands and products, organic growth and margin runway, competitive advantage in its scale of distribution and a strong balance sheet’.

Reportedly the activist also wanted management to spin off the UK arm and list the core business in New York instead of London as a way to ‘create long-term shareholder value’, or get the price up.

Ferguson already reports its earnings in dollars and its US operations are much more profitable than the UK, with a trading profit margin on sales of 8.4% compared with just 2.8%.

Yet the company’s shares have tended to trade at a significant valuation discount to US rivals Home Depot and Lowe’s. For the financial year ending in July, Ferguson shares trade on 15 times earnings compared with 22.5-times for Home Depot and 20-times for Lowe’s.

Listing the shares in New York would instantly raise the firm’s profile among US investors and could be a way to narrow the discount.

Appointing a US chief executive, which the firm confirmed alongside the demerger proposal, is another way to help raise its profile with US investors.

For UK investors there is the prospect of being left with the demerged business which is low-margin and suffering from a weak UK construction market. The latest figures show the market experienced its sharpest fall in new orders in more than a decade thanks to poor industrial confidence and the threat of a no-deal Brexit.

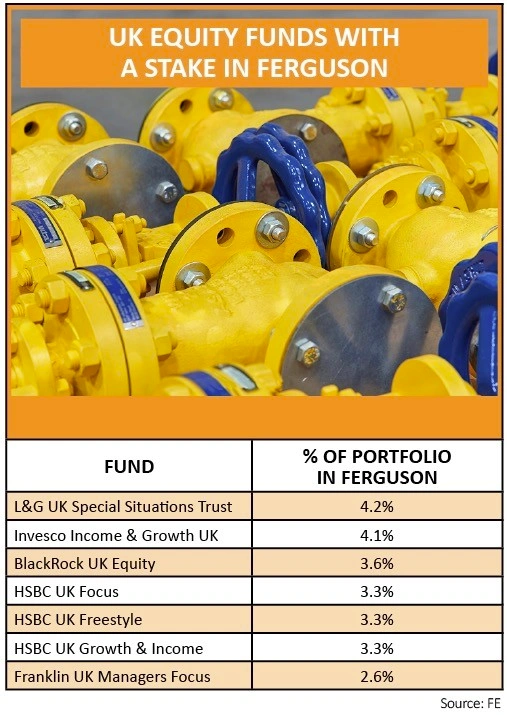

As well as an army of retail investors, quite a few UK funds and investment trusts own sizeable positions in Ferguson so there will be keen interest in the precise detail and nature of the demerger.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.