Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWe explain how Google’s owner Alphabet makes its money

Google has become a major part of everyday life thanks to its range of sought-after products and services.

To ‘Google’ has become an English verb to describe searching the internet, while many readers will own Android-powered smartphones or tune in to YouTube videos regularly – all part of the Google empire.

Yet there are probably a lot of things you don’t know about one of the biggest technology companies in the world.

FROM G TO A

Most investors still know it as Google, even though the internet search giant reorganised as holding company Alphabet in 2015. So if you want to buy shares in Google, you now have to look for the name Alphabet on your investment platform.

The corporate rejig was designed to separate all of Google’s internet properties, like Search, YouTube, Gmail, Maps, Apps, Drive and Chrome from Other Bets, the company’s nascent ventures in biotech, healthcare, artificial intelligence and much else.

Its self-driving technology developer Waymo, life sciences arm Verily and Wing, its drone delivery start-up, are some of the better-known activities that fall under the banner of Other Bets. Some sound quite madcap, like Loon, which is developing internet services being supplied using high-altitude balloons.

But there is no question that the revenue and profit powerhouse of Alphabet remains its internet search and advertising business.

DIGITAL DOMINANCE

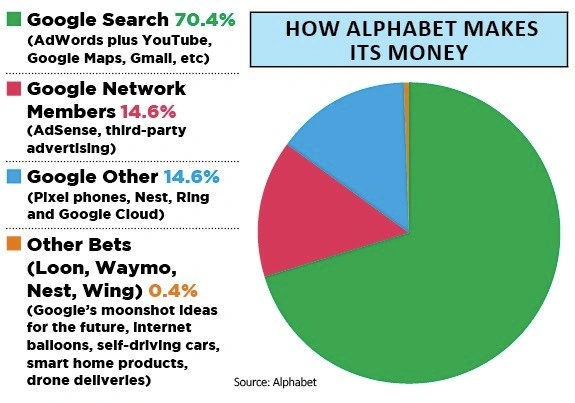

In 2018 Alphabet generated 70.4% of the $136.8bn overall revenue from its internet search and advertising, plus user activity on platforms like Gmail, Google Maps, Google Play and YouTube.

When you use Google to search for anything from financial information to local weather, you’re given a list of search results generated by Google’s top secret algorithm. The algorithm attempts to provide the most relevant results for your query, and, along with these results, you may find related page suggestions from an AdWords advertiser.

AdWords integration touches almost all of Google’s web properties so the recommended websites you see when logged into Gmail, YouTube, Google Maps, and other Google sites are generated through the AdWords platform.

To gain the top spot in Google advertisements, advertisers have to outbid each other in an auction. Higher bids move up the list while low bids may not even be displayed.

Advertisers pay Google each time a visitor clicks on an ad, anything from a few cents to more than $50 for highly competitive search terms such as insurance, personal injury, loans and other financial services.

Bolted on to this technology is AdSense which directs tailored ads to third-party websites for a fee. Other revenue streams include Pixel phones, Nest in-home connected products and Ring, the smart doorbell that lets you see who’s at the door from anywhere via your phone. There’s also Google Cloud, with a now $8bn annual revenue run-rate, although still well behind market leader Amazon Web Services’ $34bn.

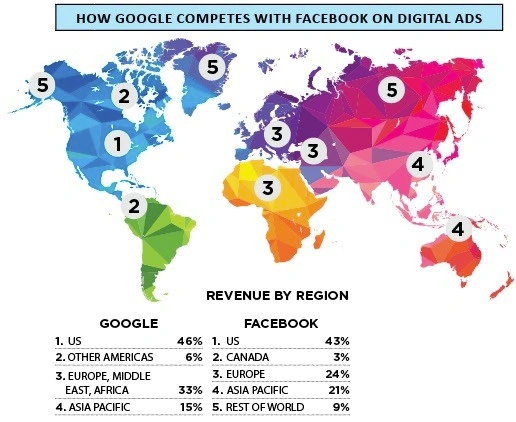

What this translates into is market dominance of the internet search and ads space. It’s now estimated that Google has about 2bn monthly users, which translates to approximately 3.5bn searches every day. As of 2019, Alphabet has approximately 90% of the search engine market share globally, plus capturing around a third of the world’s online advertising revenue, with Facebook a distant second at 20%, although Amazon looms as a new rival in digital ads.

QUESTIONS TO ANSWER

This has prompted some analysts to wonder if Alphabet’s income streams are diverse enough, ‘as it remains heavily dependent on advertising’, note analysts at Morningstar.

Others are more optimistic. ‘Its core Google business shows that the online advertising industry is still growing quickly,’ noted Christopher Rossbach, chief investment officer at investment company J Stern & Co, in response to second quarter results in July.

‘Those that had prophesised that Google’s glory days for search-related ad revenues were over clearly had to think again,’ says Richard Holway, the founder of TechMarketViews.

But the relative health of the online advertising market is not the only concern. Stiffer regulation is a worry for Alphabet as well as other internet companies that gather consumer data.

The US Department of Justice is exploring an antitrust investigation of Alphabet’s internet search and advertising business, and in March the company was handed a €1.49bn fine by the EU for breaching antitrust rules.

If the worst came to pass Alphabet could possibly restructure itself under regulatory pressure but it would likely fight tooth and nail and a legal battle could drag on for years.

THE KEY NUMBERS

What we can say with confidence is that Alphabet remains a financially strong business awash with cash. Net cash jumped $12bn in the first half of 2019 to $121bn, with second quarter earnings jumping from $11.75 to $14.21 per share year-on-year.

Alphabet's big numbers

3.5bn Google searches are made every day

60% of Google searches are done via mobile devices. Only five years ago, the figure was nearly half that at 34%

2bn monthly active YouTube users

Top 10 YouTube channels earned $180.5bn between June 2017 and June 2018

YouTube has 1.9bn monthly active users, second only to Facebook’s 2.27bn

That led the company to accelerate its share buyback plans to $25bn, and that’s on top of the rough $7bn shares bought back so far in 2019.

In Q2, the number of paid clicks jumped by 28% year-on-year although cost per click – the amount advertisers pay when someone clicks on their advert via Google – dropped by a worrying 11%.

‘Alphabet continues to strike a good balance between investing for long-term growth and operating margins,’ said J Stern’s Rossbach in July. Operating margins this year are forecast at around the 21% to 22% mark on high single-digit revenue growth to $162.5bn.

The shares trade on 22.2 times forecast earnings for the next 12 months. This is based on the $1,198.375 A shares, which carry one vote each. Non-voting C shares trade modestly cheaper at $1,197.43, but either way the power still sits with founder-owned B shares, which carry 10 votes each but are not traded on public markets.

It’s worth noting that Alphabet floated at $85 back in 2004, implying a hike of more than 1,300% to date.

‘Alphabet’s outlook remains very bright, with numerous growth options for the company that can provide significant upside to the current share price,’ is how Rossbach sees the stock.

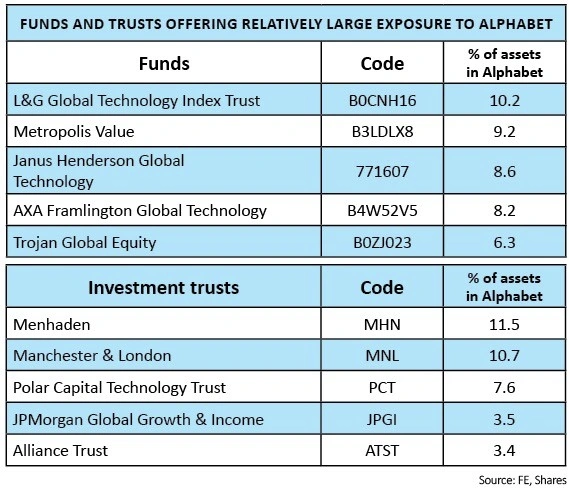

SHARES SAYS: With so many fingers in so many potential growth pies Alphabet remains a very solid holding for the long-term. We’ve published a table in this article showing the funds and investment trusts with the biggest holding in Alphabet as a proportion of their overall portfolio in case investors want an alternative way of getting exposure than buying the NASDAQ-listed shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.