Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineOutstanding dividend payers in the FTSE 350

Investors looking for income from their portfolio should be mindful of the drag effect that inflation can have on their dividends as well their sustainability. Inflation reduces the purchasing power of each pound spent and over time can seriously reduce the ‘real purchasing’ value.

For example over the last 10 years the consumer price index (CPI) has averaged 2.1%, which doesn’t sound much, but that is equivalent to a 21% reduction in purchasing power over that period.

Investors should therefore look for companies which grow their dividends at least in line with the underlying trend rate of inflation.

But if you were wondering about how to go about finding the best companies offering inflation-busting income, Shares is here to help.

GOOD VERSUS BAD DIVIDENDS

It might be tempting to look for the highest yields, especially with interest rates at such low levels, but we would caution against following this approach. Dividend yields above 6% should be viewed with suspicion as a high level may indicate that the market thinks they are unsustainable.

Investors in Vodafone (VOD) and Centrica (CNA) know this story only too well given recent cuts in their dividends following a period of very high yields.

Also, it doesn’t really matter what the size of the yield is if the dividend doesn’t grow at least as fast as inflation over time.

OUR SEARCH PROCESS

We’ve taken a look at the constituents of the FTSE 350 and have crunched the numbers from SharePad to identify shares that income investors might consider including in their portfolios.

Of the 350 companies in the index we excluded investment trusts and those companies which didn’t have 10 years of data available. That whittled the universe down to 168 companies, which we analysed further to find those companies which consistently raised or maintained their dividends, rather than picking the fastest growers.

One caveat we should point out is that the limitations of the available data from SharePad restricted the time period to the last 10 years which roughly coincided with the end of the financial crisis and the start of the latest economic expansion.

Therefore we suspect that the growth rates shown probably overstate the natural long-term growth rate because the start date represents an abnormally low point in the cycle.

That said, the results are still interesting and informative as well as surprising. For example, not many people would have guessed that silver and gold miner Fresnillo (FRES) would top the dividend growth table, with a 10-year average growth rate of 72.7%. However, the average masks very high volatility.

The dividend was cut on four occasions over the last 10 years and some of the cuts were pretty brutal. In the three years from 2012, the dividend was cut by 41%, 92% and 36% respectively, not a pleasant result for investors relying on the company to provide them with a steady income.

In addition the cover ratio (the amount of times the dividend is covered by earnings) fell steadily from around five-times to under two-times, a level we consider a minimum to give confidence in the reliability of the dividend actually being paid.

WE WANT SUSTAINABLE GROWTH

As we saw with the likes of Fresnillo, focusing on growth rates alone is not necessarily the best approach to finding inflation-busting companies. What’s more relevant is the sustainability of the dividend and its future growth rate, which should be above the inflation rate of 2.1%.

There are so few companies that always increase their dividends which suggests that it doesn’t happen by chance, but is the result of strong and stable fundamentals. It also probably means that management run operations smoothly.

There is something called the Lindy effect, coined in 1964 by Albert Goldman. In the present context, this means that a company’s track record of growing dividends is a good indicator of its future growth rate. However, we should point out that, like many things in life, nothing is guaranteed to continue forever.

THE NEXT STEPS IN OUR SEARCH

In our screening exercise we excluded companies that had reduced or suspended their dividend as well as those unable to grow the dividend faster than the rate of inflation. This reduced the universe from 168 to just 37 companies.

Our next step was to filter the list by removing those companies whose dividends were less than twice covered by earnings.

We would be particularly sceptical of any company that borrowed money in order to pay its dividend, as they are just storing up trouble for the future.

Filtering for at least two-times dividend coverage reduced our universe to 20 companies. To guide us towards the best five companies we applied another measure of financial robustness which also has the added benefit of steering us away from the most expensive shares.

FREE CASH FLOW YIELD

Free cash flow yield is measured by taking the cash generated by the business, deducting capital expenditure, then dividing this figure by the total value of the company, or enterprise value. The free cash flow yield can be used as a measure of cheapness where the higher the number, the better value on offer.

Essentially, this measure is less susceptible to manipulation, because it is a cash number rather than an accounting number, which are generally non-cash based.

Free cash flow can be used by the company in a variety of ways. Management can use it to service debts, invest in the business for growth or pay dividends to income investors.

GETTING TO THE FINAL FIVE

It would be tempting to buy those companies with the highest historical growth rates, giving us inflation-busting success, if only future growth rates matched those of the past.

But if you look at the companies on the list, we just don’t know whether, for example, equipment rental company Ashtead (AHT) will be able to replicate the 10-fold increase in dividends that it has delivered since 2009.

As a cyclical company mainly exposed to the US, it has clearly benefited from the upswing in US GDP growth, but it would be susceptible to any future downturn, although its strong dividend cover may give investors some comfort.

Even during the depths of the financial crisis the company continued to increase its dividends, demonstrating the robustness of its business.

Rather than rely on historical growth rates as a guide, we also incorporated the free cash flow yield to help pick out the best five companies.

To recap, each company on the list has increased its dividend more than inflation every year for the last 10 years, and current dividends are covered at least two times by earnings per share.

5 OUTSTANDING DIVIDEND PAYERS

Paragon Banking (PAG) 440p

Paragon has grown its dividend six-fold over the last 10 years, an average rate of 22% per year. In addition the company has been actively buying back shares, on average around 2.2% a year, while it currently offers a 5.3% yield which is 2.4 times covered by earnings.

The company has consistently earned a return on equity of around 13%, while the shares trade in-line with book value, which seems stingy given the impressive track record. The core tier-one ratio, a key measure of financial strength, sits at an impressive 14.6%, way above the 10.5% minimum required by the regulator.

Paragon has been listed since 1985 and provides specialist banking services to the professional buy-to-let market which accounts for 62% of its loans with commercial lending making up the rest.

A quarterly update released on 30 June showed the company delivering on its goals, with lending volumes rising 20% year-on-year. The group remains on track to achieve its full year guidance of mortgage lending of £1.6bn and commercial lending of at least £0.9bn.

WH Smith (SMWH) £19.63

One of Shares’ running Great Ideas selections, WH Smith has successfully transformed from a staid high street books and stationery seller into a growth company focused on international travel outlets and hospitals.

The company has grown its dividends almost three-fold over the last 10 years, equivalent to 14.5% per year. It currently has a yield of 2.7%, covered twice by earnings.

Its travel arm continues to perform strongly as does the international business and with the acquisition of InMotion, the company now operates from 428 stores outside the UK.

Continued cost savings have been achieved in the UK high street stores helping to deliver margin improvements in line with the company’s plans.

Chief executive Stephen Clarke is stepping down on 31 October after 15 years with the company and overseeing 24% growth in pre-tax profit and a 177% rise in the share price.

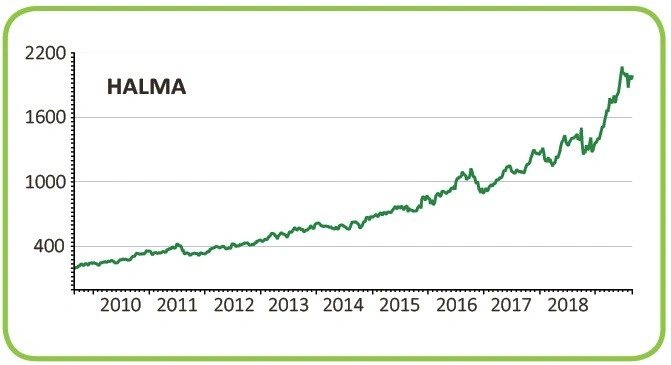

Halma (HLMA) £19.66

Electronics equipment maker Halma has increased its dividend consistently over the last 10 years, averaging 7.1% a year, which means they have roughly doubled over the period. In fact, the company has increased its dividend every year for the last 40 years. The shares currently yield 0.8% while the dividend cover is a healthy 3.8-times.

You may think it is odd that we are saying to buy Halma as an income stock when the yield is so low, yet we would remind investors that the income stream has been growing a very attractive rate and we hope this will continue in the future.

The firm’s focus on health, safety and environmental markets continues to drive long-term growth and thanks to its disciplined cost control, full year pre-tax profit rose by 15% marking a record 20.3% margin.

Halma achieves impressive returns on invested capital, averaging around 16% over the last six years, and the company highlights some reasons why that might be sustainable.

These include a focus on niche markets which have growth characteristics; a clear strategy to grow organically and selectively through acquisitions; and a simple financial model focusing on high levels of cash generation, allowing the company to reinvest in future growth and finance a progressive dividends to shareholders.

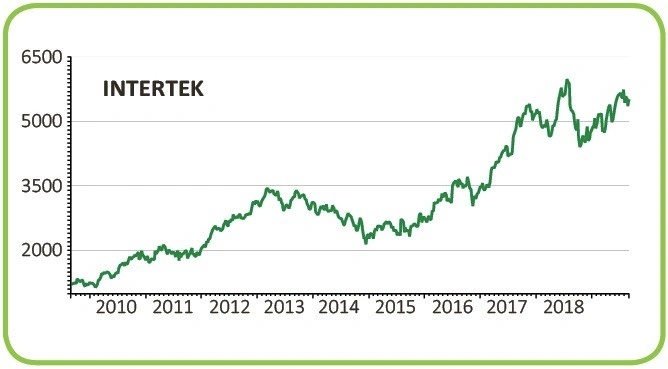

Intertek (ITRK) £54.50

Testing and certification company Intertek has grown its dividends almost four-fold over the last 10 years, giving an average annual growth rate of 17.6%. The 1.8% dividend yield is covered two times by earnings.

The company is the largest tester of consumer products in the world and has over 1,000 laboratories, operating in 100 countries across the global. Intertek works for governments and customs offices to improve compliance of imports with safety standards.

The recent half year results saw revenue growing 7% and operating profit up 8% while operating cash flow was up an impressive 12% to £219m. Operating margins improved for the fifth year in a row with progression seen across all three divisions.

In line with a dividend policy that targets a payout ratio of circa 50%, and underpinned by high margins and a cash generative earnings model, the company announced a half year dividend of 34.2p per share, an increase of 7.2%.

Diploma (DPLM) £15.83

A distributor of specialised technical products, Diploma has increased its dividends two and a half-fold over the last 10 years, giving an annual growth rate of 13.6%, handsomely beating inflation. It currently offers a 1.6% dividend yield, which is 3.3 times covered by earnings.

One of the big advantages of Diploma’s business is how resilient it is in downturns when other suppliers tend to struggle, helped by having a large interest in the supply of products to the healthcare sector which operates regardless of good or bad economic conditions.

In the case of seals and gaskets, customers like construction and mining firms are always replacing worn-out parts to keep what are typically fairly expensive pieces of machinery working.

In an update released on 28 August Diploma said that trading remained in line with expectations and revenue is expected to grow by circa 13%, comprising of 5% underlying revenue growth and 6% being contributed from acquisitions, net of disposals. Currency tailwinds should also boost revenue by 2%.

The operating margin is expected to be modestly ahead of last year, benefiting from tight control of costs and operating leverage from growth in revenue.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.