Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineChanging a fund manager can benefit investors

In the same manner a football team’s fortunes can turn upwards when a new manager enters the dressing room, performance can also improve when a new portfolio manager takes over or assumes sole responsibility for an investment trust.

A long-standing manager can benefit a trust if they have experience of how to navigate both good and bad markets. However, by bringing a fresh pair of eyes, a new broom is at liberty to shake up the portfolio in ways such as altering the investment strategy, allocating capital differently or perhaps pruning a long tail of underperforming stocks.

Within the diverse investment trusts sector, recent exemplars include Baillie Gifford UK Growth Fund (BGUK). In June last year, the board of what was then Schroder UK Growth awarded the mandate to Baillie Gifford, alarmed by a period of poor performance.

Over the year to 31 July 2019, it is now the third best performing investment trust out of the Association of Investment Companies’ (AIC) 13-strong UK All Companies sector.

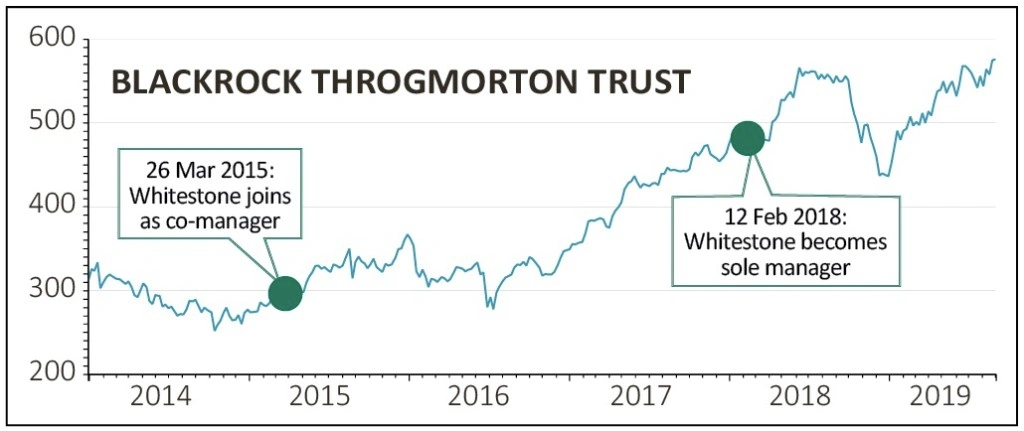

Strictly-speaking, Dan Whitestone isn’t a new broom at BlackRock. He’d co-managed BlackRock Throgmorton Trust (THRG) with the veteran investor Mike Prentis since 2015. Yet the trust has performed strongly since Whitestone took over as sole manager in February 2018, being the AIC UK Smaller Companies sector’s third best performer out of 23 over the year to July.

CHANGES AT MARTIN CURRIE TRUST

A former under-19’s Academy player at French football giant PSG who went on to become head of European research at BlackRock, Zehrid Osmani was appointed joint portfolio manager of Martin Currie Global Portfolio Trust (MNP) in June 2018 alongside industry veteran Tom Walker.

He took over as lead manager on 1 October 2018 following Walker’s retirement and the self-styled ‘long-term unconstrained investor’ has subsequently exhibited his deft stock picking skills, having turbo-charged returns.

Martin Currie Global Portfolio Trust is the top performing investment trust on a share price total return basis within the Global sector in the first seven months of 2019.

Improved performance means the discount to net asset value has narrowed, even swinging back to a premium, enabling the company to issue shares at a premium for the first time since 2016 to sate investor demand.

We also note the quarterly dividend payer has increased or maintained the dividend every year since launch in 1999 and offers shareholders inflation-beating dividend growth.

OSMANI’S HIGH QUALITY BIAS

Martin Currie Global Portfolio has a high quality bias, offering exposure to names including Visa, Microsoft, Adidas and Ferrari.

Under Osmani, the portfolio has become more concentrated around the new man’s highest-conviction ideas. The portfolio’s quality exposure, as defined by return on equity, has increased. And as 31 July, the book contained 33 holdings across 15 countries.

Active share, a measure of how different a fund’s holdings are from its benchmark, amounted to 93.6%. If a fund had no holdings at all in common with its benchmark, it would have an active share of 100%, and if all its holdings were the same as the benchmark, its active share would be 0%. High active share is considered roughly 80% or more.

‘We are persistently quality growth, which should be reassuring to our investors,’ Osmani informs Shares.

He defines quality growth as companies that have got sustainably high returns. His philosophy is that companies with a high and sustainable return on invested capital generate above-average total returns over the long term.

‘How we find these stocks is through fundamental research, which we do systematically’, he continues. Part of the in-depth fundamental research process involves focusing on three long-term megatrends: the future of technology, demographic change and resource scarcity.

Given an uncertain global macroeconomic backdrop, Osmani stresses the importance of focusing on companies that have an element of pricing power and can deliver in economic weathers fair and foul.

In addition to Ferraria, a unique franchise with a high degree of pricing power, the portfolio includes Italian luxury apparel brand Moncler, the puffer jackets-to-sweaters designer generating very high returns and significant revenue from Asia and with potential to increase its global presence.

Osmani also manages a stake in Sweden’s Assa Abloy, the world’s biggest lock maker, behind the Chubb brand and offering a play on the transition from mechanical to digital locks.

He explains that Assa Abloy is number one in a fragmented industry and has a major size advantage. ‘Assa Abloy can spend more on research and development and is also a play on the connected home. Its digital locks are compatible with both Amazon and Apple.’

If any money manager understands the competitive strengths of Assa Abloy it should be Osmani, whose father actually used to be a locksmith.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.